Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Prospects for the Swiss Economy Remain Favourable

The KOF Economic Barometer has only changed little and reached a value of 102.7 in July. In June, and therefore before the referendum in the United Kingdom about its membership in the EU, the KOF Economic Barometer stood at a value of 102.6 (revised from 102.4). Thus the Barometer has been standing above the historical average since February this year. Despite the outcome of the vote in the United Kingdom and various other geopolitical risks, the outlook for the Swiss economy remains stable. |

KOF Economic Barometer Click to enlarge.

|

Japan

Bank of Japan Governor Kuroda appears to be the central banker that the markets have the most difficulty in reading. The activist Governor provide the barest of tweaks to what is by nearly any reckoning among the most aggressive monetary policies by a high income economy. Moreover, much of the important data reported during the BOJ’s meeting, including inflation and consumption were weaker than expected.

The BOJ increased its ETF purchases from JPY3.3 trillion a year to JPY6 trillion. This was the lowest hanging fruit for the central bank, and there was broad agreement that this step would be taken. The BOJ also doubled its dollar-lending facility. And that was it. No, cut in the negative deposit rate. No additional JGB purchases. No pushing out the inflation target or increasing the JPY80 trillion monetary base growth.

The market’s response was clear and not surprising. The yen strengthened. The dollar spiked to JPY102.70 after having been squeezed to JPY105.50 in the NY afternoon yesterday. The JPY102.25 area corresponds to a (61.8%) retracement of the greenback’s rally from the Brexit low of JPY99 to last week’s high near JPY107.50. Moving beyond that retracement objective may embolden participants to look for another test on JPY100. On the topside, the dollar has been unable to retake the JPY104-handle since the BOJ announcement.

Kuroda’s pledge of a comprehensive review of the monetary policy framework at the September 20-September 21 meeting is not the main focus now. However, it promises to inject fresh volatility in the market after the summer. Draghi also flagged the September ECB meeting as important.

Japanese government bonds sold off hard, with the benchmark 10-year JGB yield rising eight bp, which leaves it is minus 20 bp. Japanese stocks overcame initial weakness to close higher, with the Topix up 1.2% and the Nikkei gaining almost 0.6%. On the week both indices lost about a third of a percent. Nearly all of the other markets in the region fell, and Tokyo was sufficient to lift the MSCI Asia-Pacific Index 0.5%, the fifth consecutive advance 13 of the past 15 sessions.

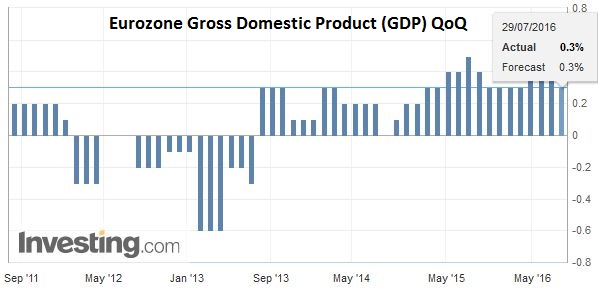

EurozoneIn Europe, there are two main developments. First, the economic data. The preliminary July CPI estimate came in at 0.2% after 0.1% pace in June. The market had expected a 0.2% increase, but after the firmer than expected German data yesterday, the risk was on the upside. The core rate was steady at 0.9%. The median guesstimate was for slippage to 0.8%. June unemployment was steady at 10.1%. |

Click to enlarge. Source Investing.com |

| The initial estimate of GDP showed a 0.3% expansion, which was in line with forecasts, and it follows a 0.6% expansion in Q1. The year-over-year pace held in at 1.6% after 1.7% in Q1, which is seen as a bit better than a trend. Details will be available in a couple of weeks. |

Click to enlarge. Source Investing.com |

| We do know that the French growth disappointed by not there not being any. A 0.2% expansion was expected. However Q1 GDP was revised up to 0.7% from 0.6% Spain’s 0.7% expansion may be the envy of most in Europe, but it matches the country’s slowest pace since Q3 14. Separately, Spain reported an easing of deflationary forces. CPI fell 0.6% from a year ago after a 0.8% fall in June. Lastly, German retail sales disappointed by falling 0.1% (median forecast was for a 0.1% gain) and the May gain was shaved to 0.7% from 0.9%. |

Click to enlarge. Source Investing.com |

European Banks

The second development in Europe today is the last minute private sector attempt to buy Monte dei Paschi, Italy’s troubled bank. Reports indicate that a local businessman has proposed to team up with a Swiss bank, which is rivaling another offer from a US bank and an Italian bank combine. The market’s initial response is favorable. The Milan bank index is up nearly 4.5% near midday in Italy. The gain is enough to turn the week positive, and it is the fourth consecutive week Italian banks have recouped some of the year’s steep decline. The development in Italy is helping lift European banks. While the Dow Jones Stoxx 600 is up 0.25%, the financials are the strongest sector, up 1.8% at pixel time. Overall the index is up about 3.25% this month, which is its biggest advance since last October. The European bank stress test results will be reported at the close of the North American session today. The potential deal for Monte Paschi may reduce the anxiety over the results. Moreover, it is not as simple as a pass/fail grade, or specifying precisely how much capital particular institutions must raise. However, to be credible require in the mind of investors many of whom are not convinced European banking challenges have been addressed, there must be some actionable results. |

FX Rates Click to enlarge. |

United StatesAttention now turns to North America. US reports Q2 GDP and Canada reports May GDP. The wider trade deficit and weaker inventories that were reported yesterday prompted economists to slash their forecast for today’s US report. Many economists more or less matched the Atlanta Fed’s GDPNow tracker, which cut its estimate to 1.8% from 2.3%. One thing to watch out for today is whether the more severe inventory correction in Q2 will increase the prospect for Q3 GDP and this may be seen in the NY Fed’s GDP tracker that is published on Friday’s. |

Source investing.com |

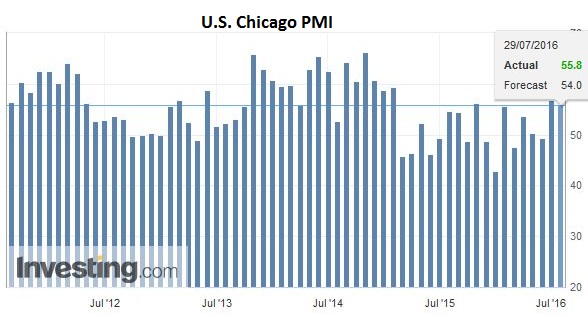

| Separately the US reports the Chicago PMI, which is notoriously volatile and the University of Michigan’s consumer sentiment report. |

Source investing.com |

| In addition to the headline, where consumer confidence remains elevated even if not accelerating higher, the inflation expectations will be watched, as the FOMC statement referred to survey-based measures as stable. The 2.6% pace expected for July matches the six- and 12-month averages. |

Source investing.com |

CanadaCanada’s May GDP is expected to have contracted by 0.5%. While Alberta’s fires and the related disruption did not help matters, the Canadian economy has faltered this year after a reasonably good Q4 15, which was the first quarter since Q2 14 that the economy expanded in each month. Canada began the year with good momentum, and in January, the economy grew 0..5%. And that’s been it. Small contractions were reported in February and March before the 0.1% growth in April. The Bank of Canada seems to be willing to write off the first half and anticipating (hoping?) for better traction in H2. Oil prices are closing the week on a soft note and is not particularly helpful for Canada. Oil prices are off 7.8% this week. It is the largest weekly fall since January. It brings the loss on the month to an eye-catching 15.7% on the continuation futures contract, the largest monthly drop since the end of 2014. |

Click to enlarge. Source Investing.com |

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?

Tags: #USD,Banca Monte dei Paschi,Bank of Canada,Bank of Japan,Canada Gross Domestic Product,Canadian Dollar,Dow Jones,EUR/USD,Eurozone Consumer Price Index,Eurozone Gross Domestic Product,Germany Retail Sales,Italian Bank,Japanese yen,newslettersent,Switzerland KOF Economic Barometer,U.S. Chicago PMI,U.S. Core PCE Price Index (PCE Deflator),U.S. Gross Domestic Product