Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

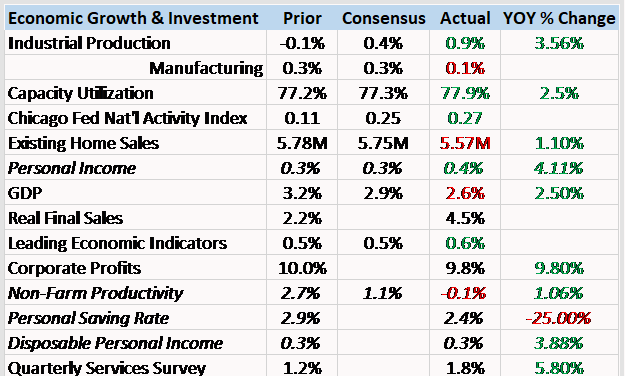

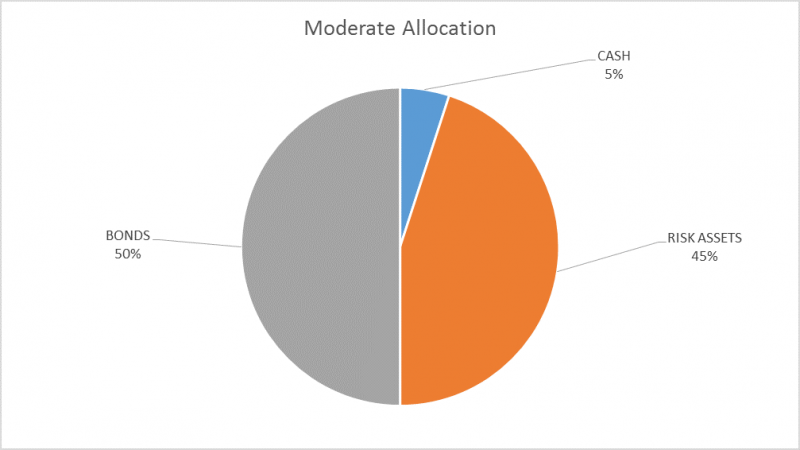

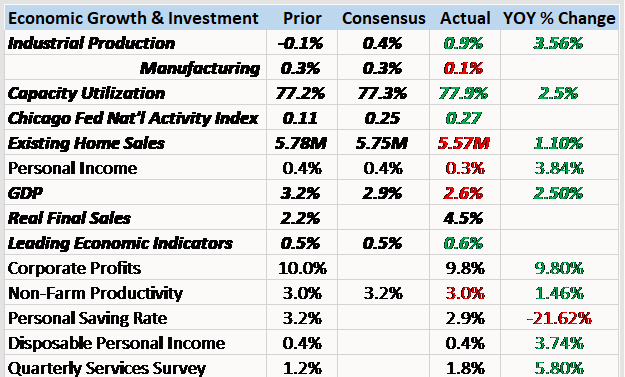

Weekly Market Pulse: It’s An Uncertain World

Weekly Market Pulse: It’s An Uncertain World3 Sep 2024

Pressure Returns to Bank Shares and seems to Help Propel Gold Higher

Pressure Returns to Bank Shares and seems to Help Propel Gold Higher5 Apr 2023

Weekly Market Pulse: Good News, Bad News

Weekly Market Pulse: Good News, Bad News14 Nov 2022

Weekly Market Pulse: Just A Little Volatility

Weekly Market Pulse: Just A Little Volatility17 Oct 2022

Weekly Market Pulse: The Real Reason The Fed Should Pause

Weekly Market Pulse: The Real Reason The Fed Should Pause11 Oct 2022

Weekly Market Pulse: A Most Unusual Economy

Weekly Market Pulse: A Most Unusual Economy11 Jul 2022

Weekly Market Pulse: Things That Need To Happen

Weekly Market Pulse: Things That Need To Happen5 Jul 2022

Update The Conflict of Interest Rate(s)

Update The Conflict of Interest Rate(s)13 Jun 2022

Simple Economics and Money Math

Simple Economics and Money Math12 Jun 2022

UST 2s & Euro$ Futures *Whites* Both Ask, Landmine At Last?

UST 2s & Euro$ Futures *Whites* Both Ask, Landmine At Last?25 May 2022

Peak Inflation (not what you think)

Peak Inflation (not what you think)15 May 2022

China Then Europe Then…

China Then Europe Then…8 May 2022

Weekly Market Pulse: Welcome Back To The Old Normal

Weekly Market Pulse: Welcome Back To The Old Normal3 May 2022

Yield Curve Inversion Was/Is Absolutely All About Collateral

Yield Curve Inversion Was/Is Absolutely All About Collateral18 Apr 2022

You Know What They Say About The Light At The End Of The Tunnel

You Know What They Say About The Light At The End Of The Tunnel14 Apr 2022

Concocting Inventory

Concocting Inventory11 Apr 2022

Weekly Market Pulse: What Now?

Weekly Market Pulse: What Now?5 Apr 2022

The Short, Sweet Income Case For Ugly Inversion(s), Too

The Short, Sweet Income Case For Ugly Inversion(s), Too4 Apr 2022

Weekly Market Pulse: The Cure For High Prices

Weekly Market Pulse: The Cure For High Prices31 Mar 2022

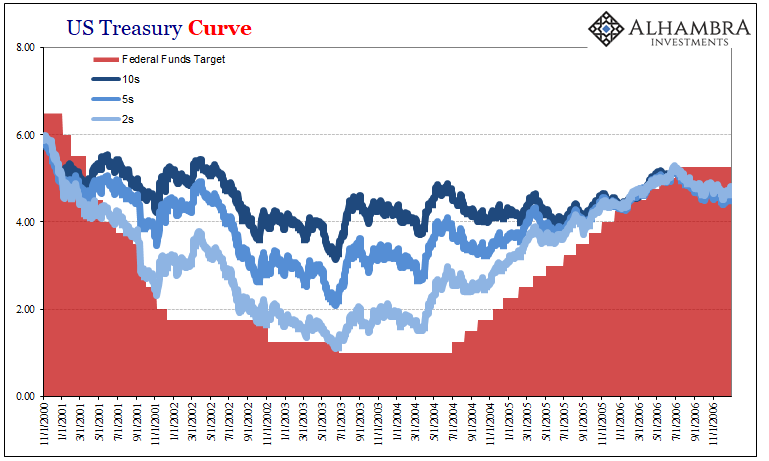

BOJ Steps-Up its Efforts, US 2-10 Curve steepens, and the Dollar Softens

BOJ Steps-Up its Efforts, US 2-10 Curve steepens, and the Dollar Softens30 Mar 2022