Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

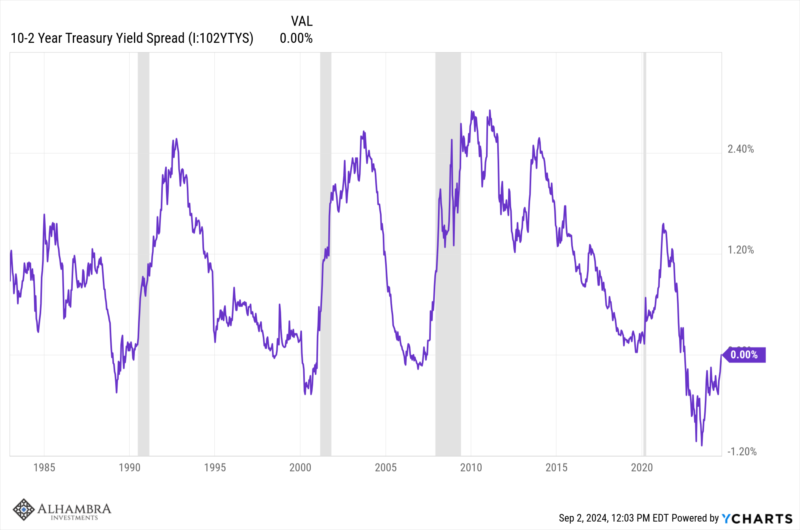

Weekly Market Pulse: It’s An Uncertain World

Weekly Market Pulse: It’s An Uncertain World3 Sep 2024

Pressure Returns to Bank Shares and seems to Help Propel Gold Higher5 Apr 2023

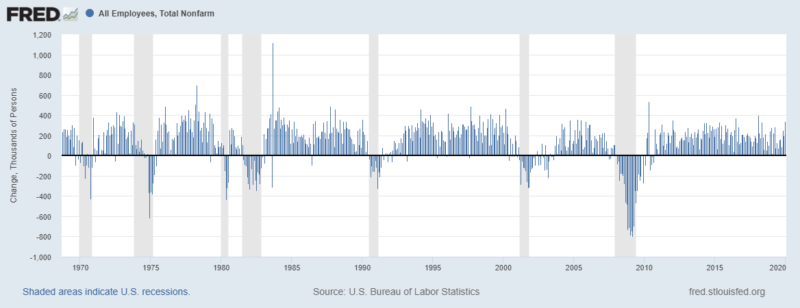

Weekly Market Pulse: Good News, Bad News

Weekly Market Pulse: Good News, Bad News14 Nov 2022

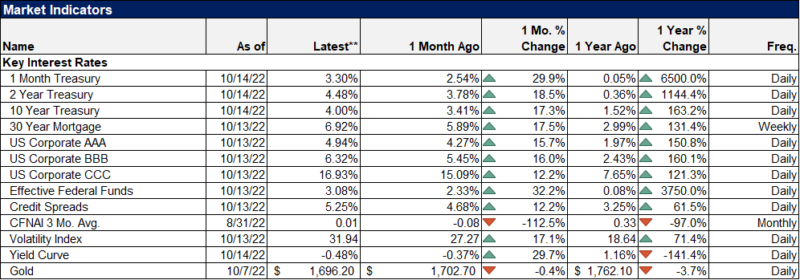

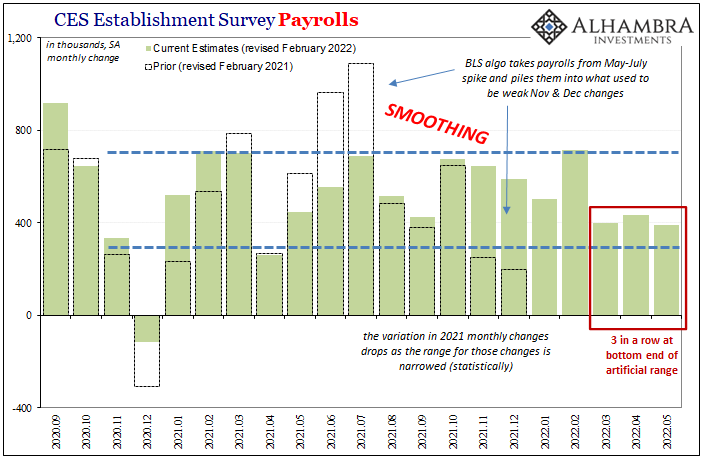

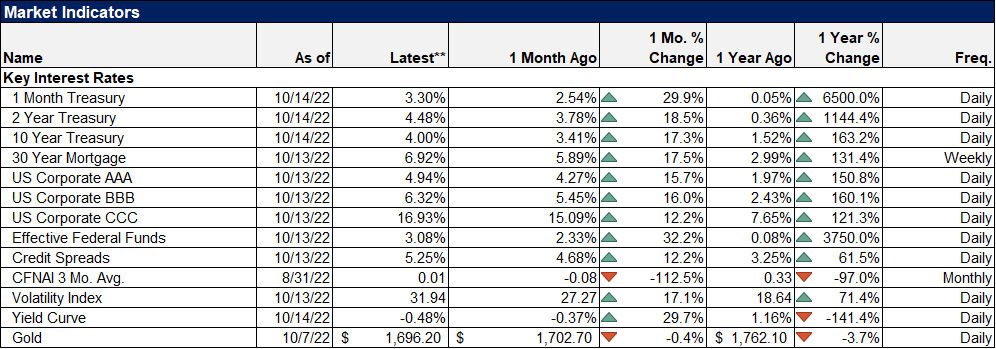

Weekly Market Pulse: Just A Little Volatility

Weekly Market Pulse: Just A Little Volatility17 Oct 2022

Weekly Market Pulse: The Real Reason The Fed Should Pause11 Oct 2022

Weekly Market Pulse: A Most Unusual Economy

Weekly Market Pulse: A Most Unusual Economy11 Jul 2022

Weekly Market Pulse: Things That Need To Happen5 Jul 2022

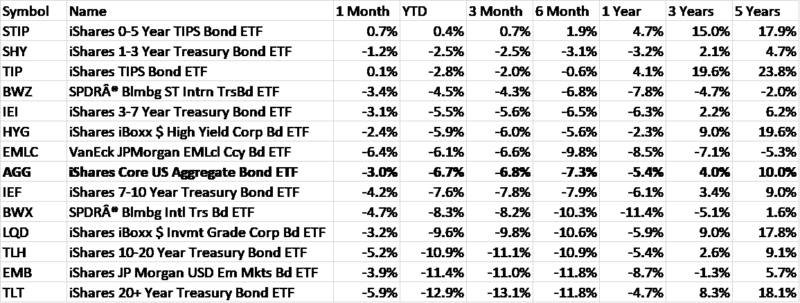

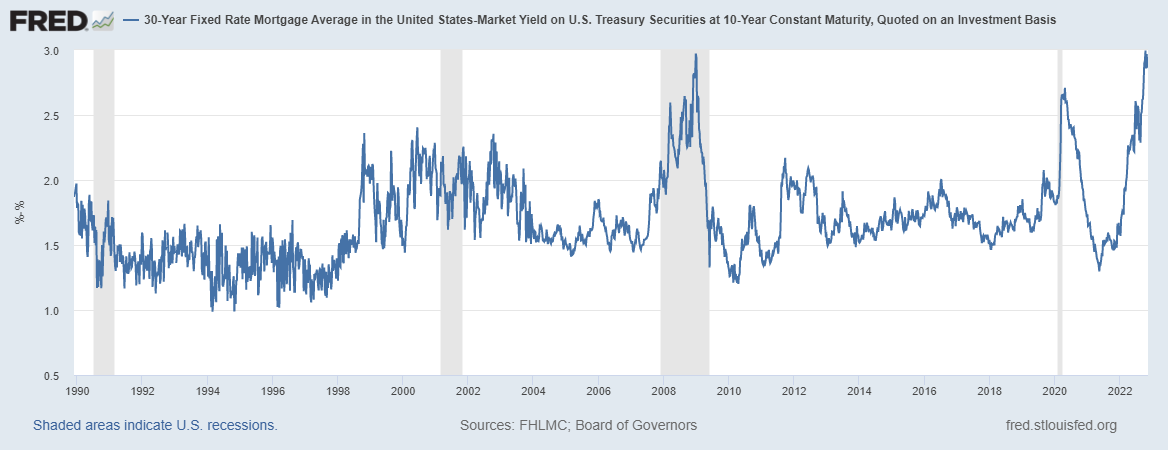

Update The Conflict of Interest Rate(s)13 Jun 2022

Simple Economics and Money Math12 Jun 2022

UST 2s & Euro$ Futures *Whites* Both Ask, Landmine At Last?25 May 2022

Peak Inflation (not what you think)

Peak Inflation (not what you think)15 May 2022

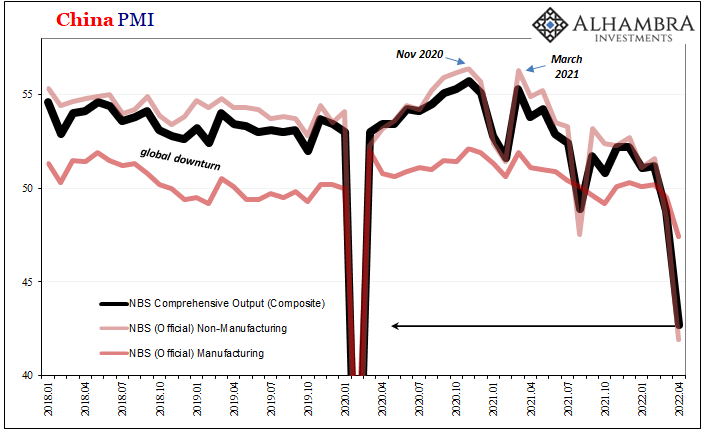

China Then Europe Then…8 May 2022

Weekly Market Pulse: Welcome Back To The Old Normal

Weekly Market Pulse: Welcome Back To The Old Normal3 May 2022

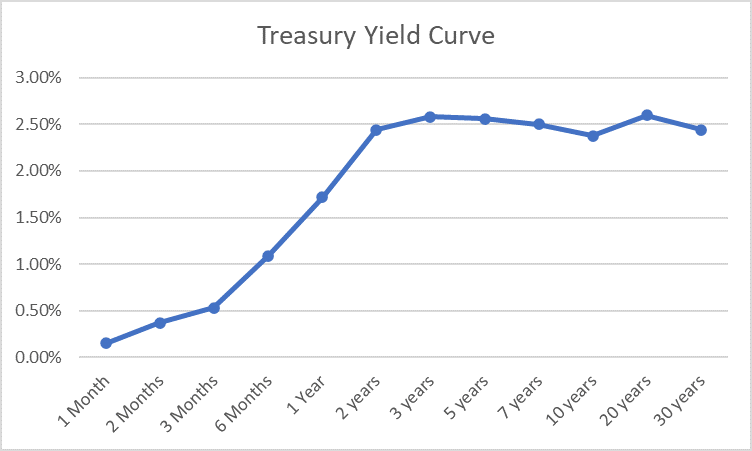

Yield Curve Inversion Was/Is Absolutely All About Collateral18 Apr 2022

You Know What They Say About The Light At The End Of The Tunnel14 Apr 2022

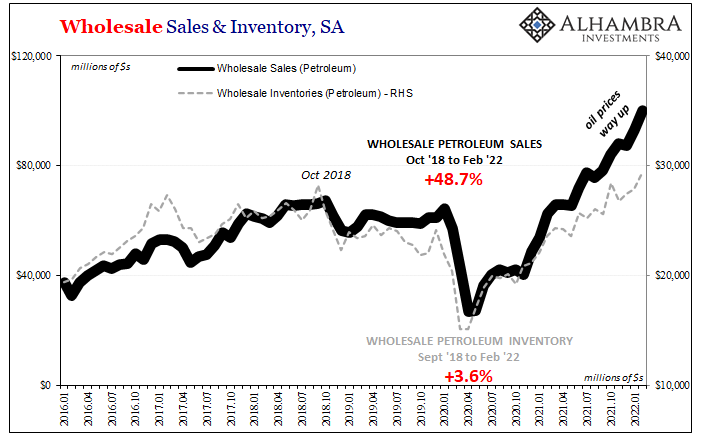

Concocting Inventory11 Apr 2022

Weekly Market Pulse: What Now?5 Apr 2022

The Short, Sweet Income Case For Ugly Inversion(s), Too4 Apr 2022

Weekly Market Pulse: The Cure For High Prices

Weekly Market Pulse: The Cure For High Prices31 Mar 2022

BOJ Steps-Up its Efforts, US 2-10 Curve steepens, and the Dollar Softens30 Mar 2022