Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

“Self-control and self-respect have become undervalued”

“Self-control and self-respect have become undervalued”17 Feb 2021

The Real Diseased Body

The Real Diseased Body12 Apr 2020

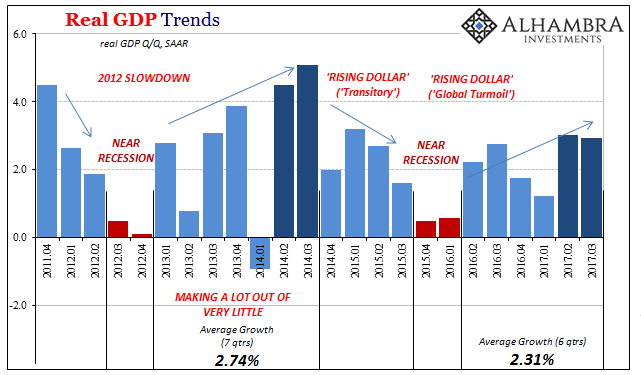

Strong Growth? Q3 GDP Only Shows How Weak 2017 Has Been

Strong Growth? Q3 GDP Only Shows How Weak 2017 Has Been3 Nov 2017

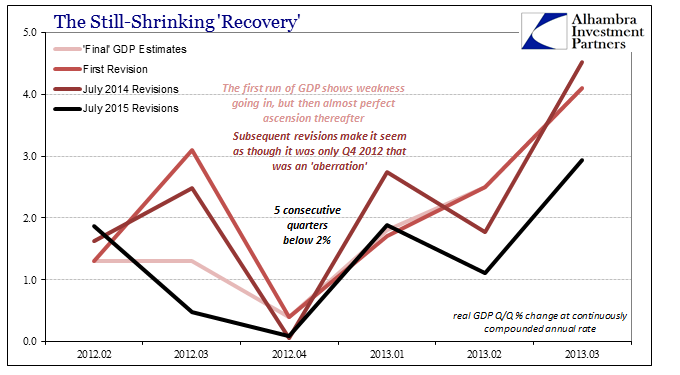

Real GDP: The Staggering Costs

Real GDP: The Staggering Costs12 Aug 2017

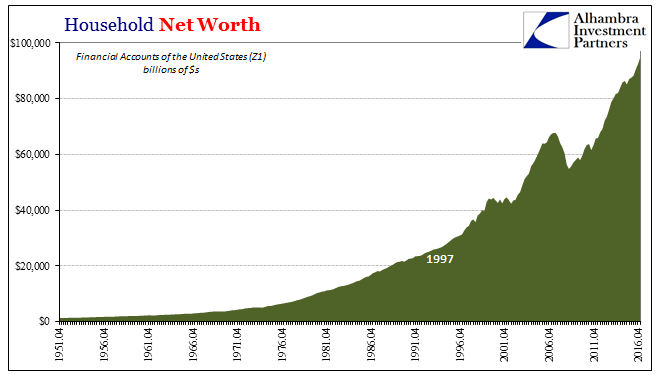

Wealth Paradox Not Effect

Wealth Paradox Not Effect18 Jun 2017

17 Jun 2017

16 Jun 2017

All About Inventory

All About Inventory14 Jun 2017

Forced Finally To A Binary Labor Interpretation

Forced Finally To A Binary Labor Interpretation13 Jun 2017

Signs of Something, Just Not Wage Acceleration

Signs of Something, Just Not Wage Acceleration11 Jun 2017

The Anti-Perfect Jobs Condition

The Anti-Perfect Jobs Condition10 Jun 2017

Dollars And Sent(iment)s

Dollars And Sent(iment)s9 Jun 2017

Pay No Attention To 50

Pay No Attention To 508 Jun 2017

Simple (economic) Math

Simple (economic) Math2 Jun 2017

Suddenly Impatient Sentiment

Suddenly Impatient Sentiment28 May 2017

Less Than Nothing

Less Than Nothing25 May 2017

Commodity and Oil Prices: Staying Suck

Commodity and Oil Prices: Staying Suck24 May 2017

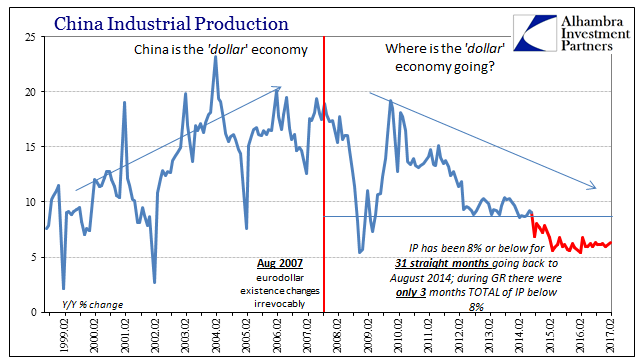

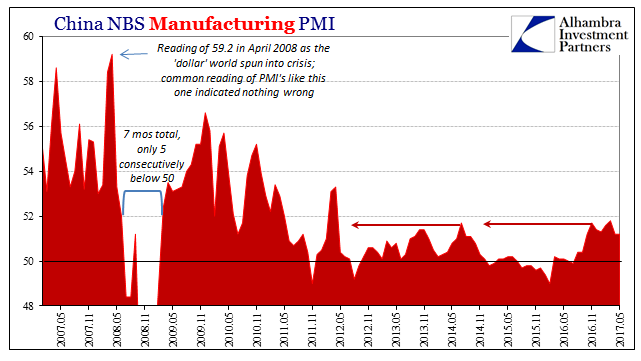

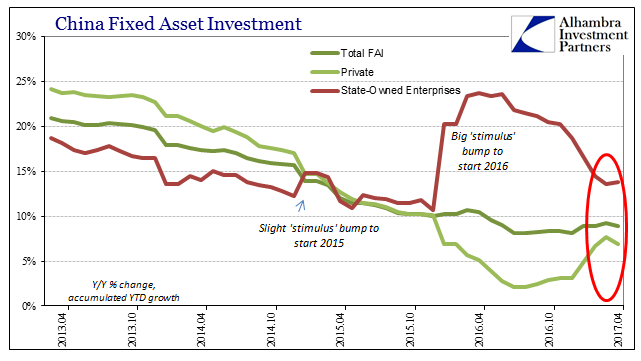

Trying To Reconcile Accounts; China

Trying To Reconcile Accounts; China21 May 2017

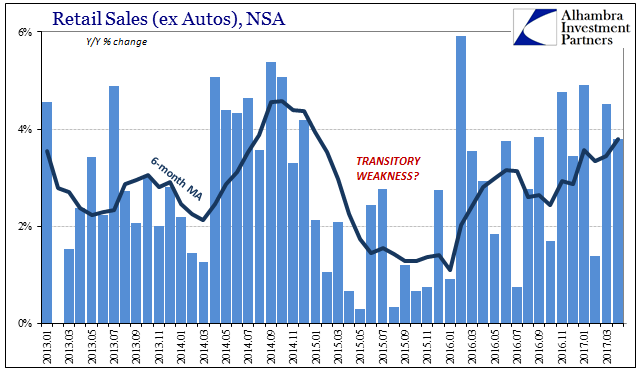

Reasonable Retail (Therefore Consumer) Expectations

Reasonable Retail (Therefore Consumer) Expectations20 May 2017

Hopefully Not Another Three Years

Hopefully Not Another Three Years19 May 2017