Jeffrey P. Snider

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

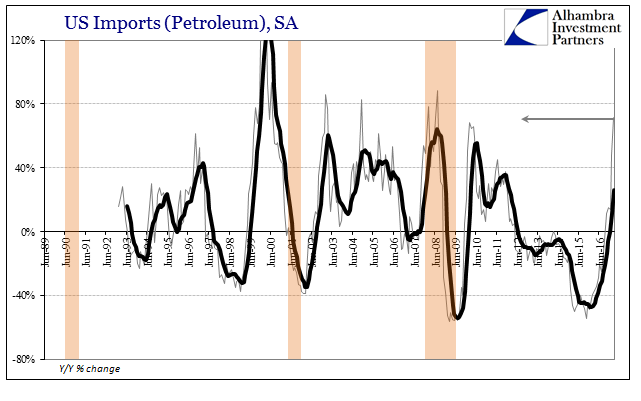

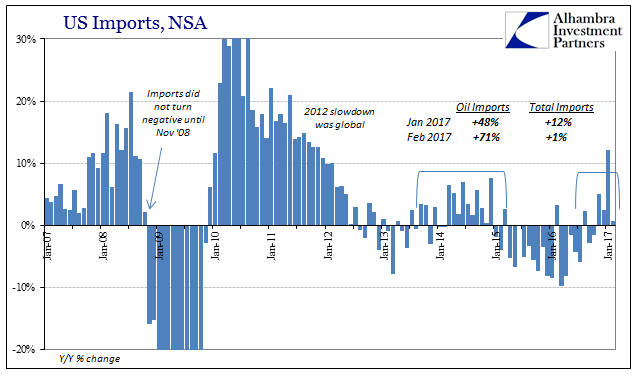

| The oversized base effects of oil prices could not in February 2017 push up overall US imports. The United States purchased, according to the Census Bureau, 71% more crude oil from global markets this February than in February 2016. In raw dollar terms, it was an increase of $7.3 billion year-over-year. Total imports, however, only gained $8.4 billion, meaning that nearly all the improvement was due to nothing more than the price of global oil. |

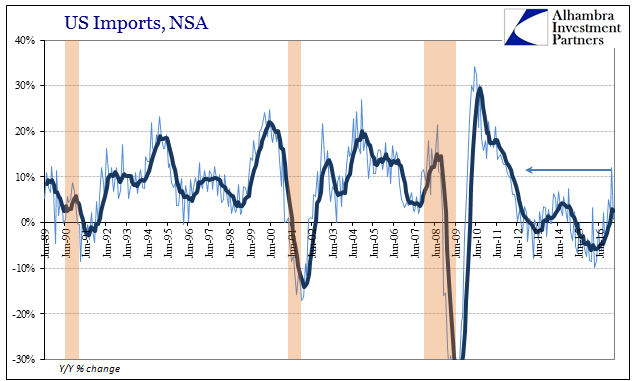

US Imports, Jun 1989 - 2016 - Click to enlarge |

| Total imports which had jumped by 12% in January were flat in February. There are still calendar effects to consider, including the comparison to last February and its extra leap year day, as well as the winding down of China’s New Year holiday. Despite those, the seasonally-adjusted estimate was down sharply in the latest month from January, suggesting that February trade on the inbound side was considerably weaker than was expected. |

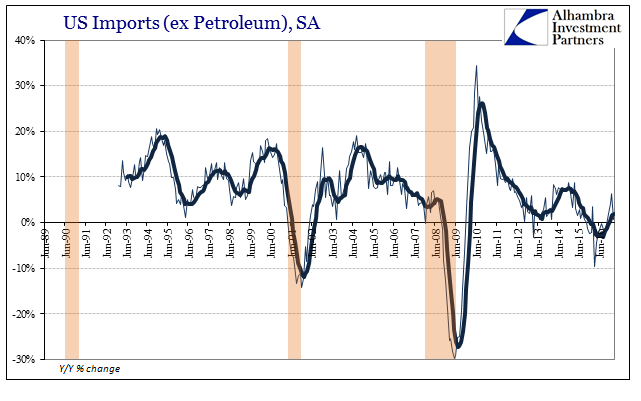

US Imports ex Petroleum, Jun 1989 - 2016 - Click to enlarge |

US Imports Petroleum, Jun 1989 - 2016 - Click to enlarge |

|

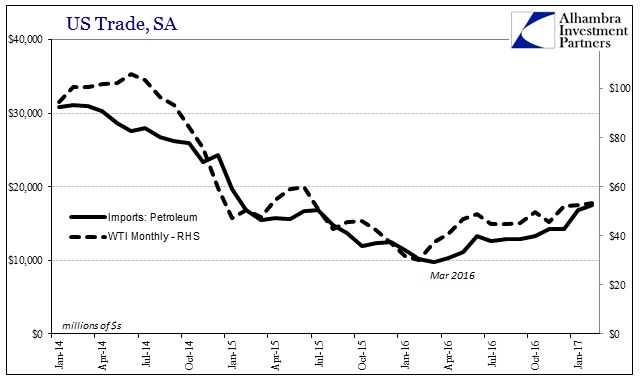

US Trade Balance, Jan 2014 - 2017(see more posts on U.S. Trade Balance, ) - Click to enlarge |

|

US Imports, Jan 2007 - 2017 - Click to enlarge |

|

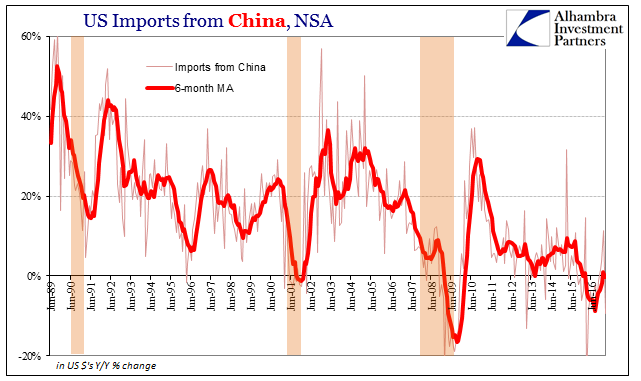

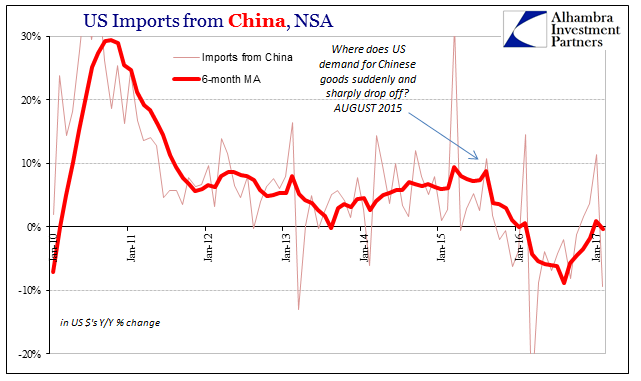

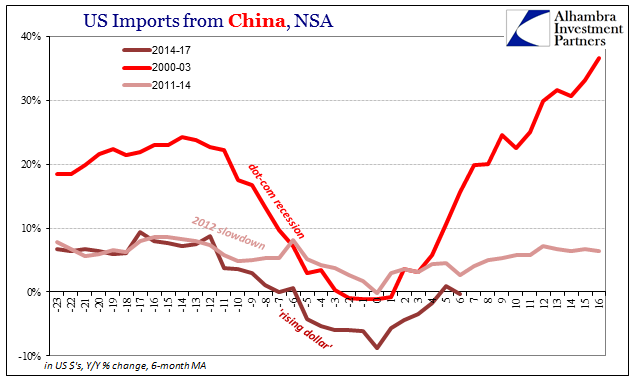

| That starts, as always, with China. US imports from China had increased 11.4% in January due to the earlier Lunar New Year over there, and then declined 9.4% in February. For both months combined, the United States purchased from the Chinese only 1% more in the first two months of 2017 than during the first two months of 2016. It is considerably less than a recovery, and quite some significant distance from even a rebound. |

China Exports to US, Jun 1989 - 2016(see more posts on China Exports, ) - Click to enlarge |

China Exports to US, Jan 2010 - 2017(see more posts on China Exports, ) - Click to enlarge |

|

| It is also asymmetric compared to prior historical experience, where in the past any downturn especially from the Chinese perspective is followed closely by an equally sharp (or better) upturn. Though statistics here as well as on that side of the Pacific are relatively better this year, they don’t show the kind of momentum that should accompany a truly meaningful improvement. Just as inflation rates outside of oil have meandered only slightly upward in the US as well as Europe, what is being classified as economic improvement only qualifies in the most minimal sense possible. |

China Exports to US(see more posts on China Exports, ) - Click to enlarge |

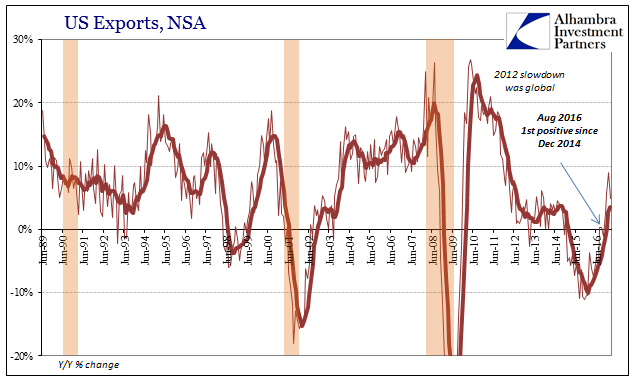

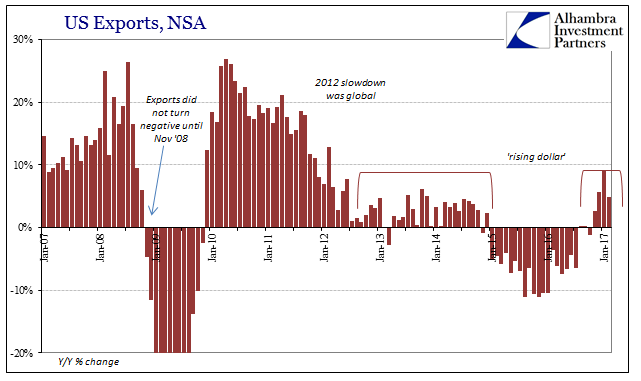

| Exports in February were somewhat better than imports, rising 4.8% year-over-year after growing by 9% in January. In context, however, these growth rates are still far below what might be called “normal.” From January 2004 until August 2008, US export growth averaged better than 13%. |

US Exports, Jun 1989 - 2016 - Click to enlarge |

| The economic problem isn’t strictly growth rates, though they are compelling enough even the wider context of time. That is the most serious issue here, the one where the lack of momentum indicates the underlying differences that truly matter. Though February’s exports were almost 5% more than in February the year before, they are 4% less than in February 2012. After five years, the US is still exporting a smaller amount than it did just after the events of 2011. The global economy simply fell off after that point and has never been restored – what recovery there might have been up to that point was rudely terminated.

Therefore the back and forth above and below zero across all of the five years since doesn’t truly indicate much beyond whether the global economy with the US still as its center is actively getting weaker or has entered these temporary interspersed periods of calm that we find in between monetary events. The lack of momentum clearly indicates nothing more than a transition to the the latter; the post-2011 economy frustratingly remains with us and in effect. For now, this is only a partial review and evidence to that prospect. The update for March 2017 will allow us to finally move past all the calendar effects in order to clarify just how much improvement there might be this year to last, to further and more robustly conclude that the US economy remains monetarily constrained. |

US Exports, Jan 2007 - 2017 - Click to enlarge |

Tags: China,China Exports,consumer spending,Crude Oil,currencies,demand,depression,dollar,economy,EuroDollar,exports,Federal Reserve/Monetary Policy,global trade,imports,Markets,newslettersent,oil prices,petroleum,U.S. Trade Balance,WTI