Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Macro: GDP Q3 — Inflationary BOOM!

Macro: GDP Q3 — Inflationary BOOM!22 Dec 2023

Weekly Market Pulse: Look Up In The Sky! It’s A UFO! Or Not!13 Feb 2023

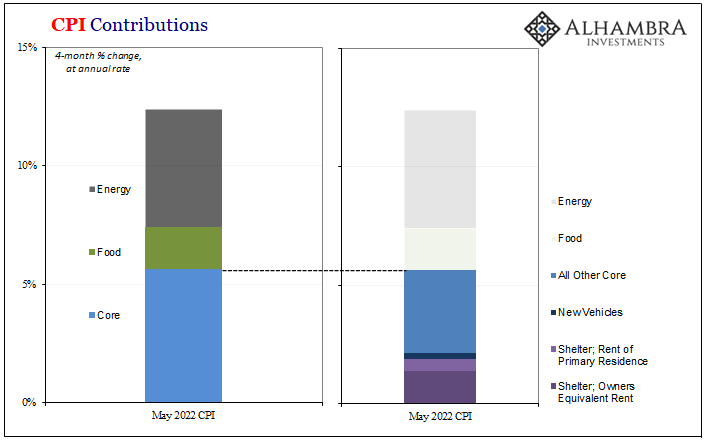

Curve Inversion 101: US CPI Politics Up Front, China PPI Down(ing) The Back16 Jun 2022

“Inflation” Not Inflation, Through The Eyes of Inventory11 Jun 2022

T-bills Targeted Target

T-bills Targeted Target20 May 2022

Industrial Synchronized Demand11 May 2022

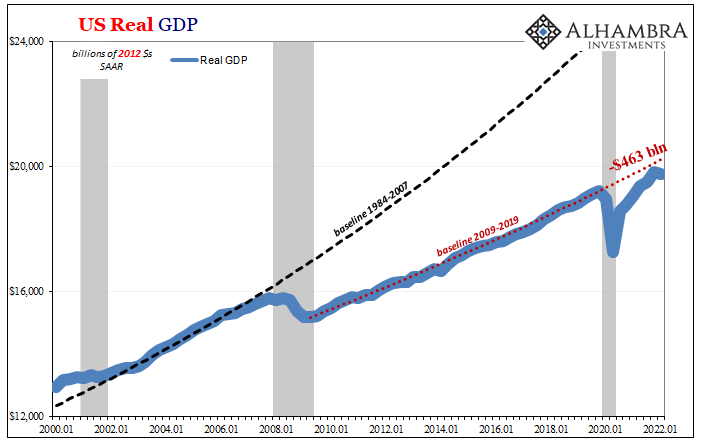

Is It Recession?30 Apr 2022

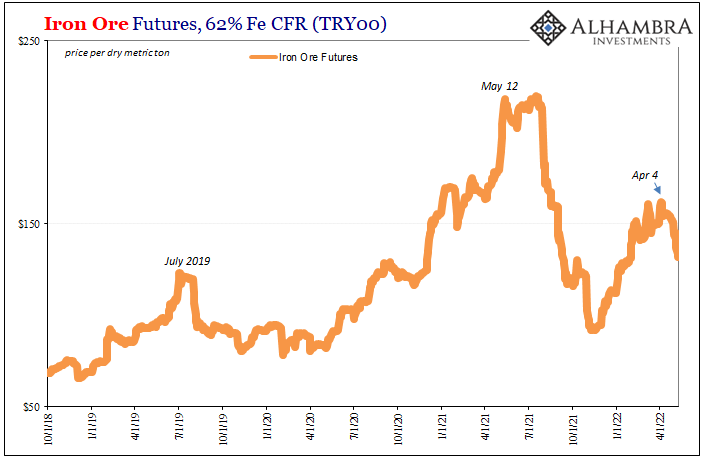

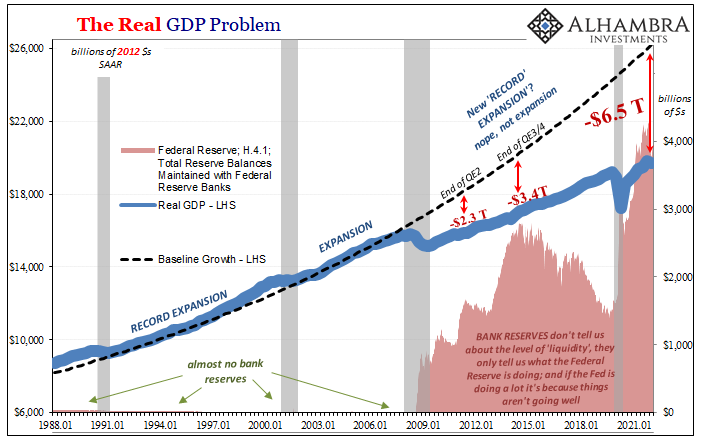

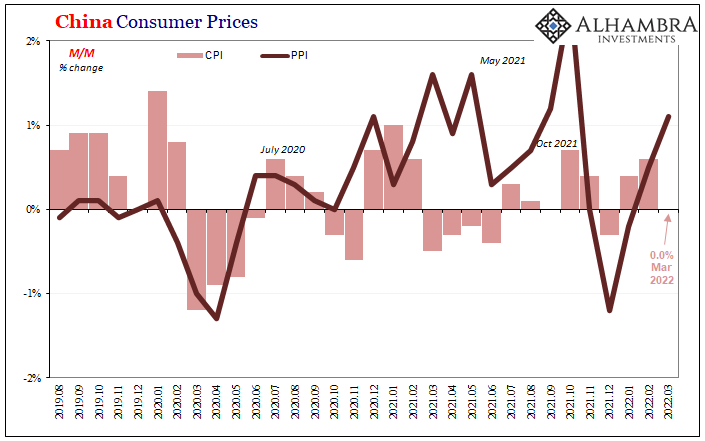

China More and More Beyond ‘Inflation’17 Apr 2022

Briefing Even More Inventory1 Mar 2022

The Enormously Important Reasons To Revisit The Revisions Already Several Times Revisited29 Oct 2021

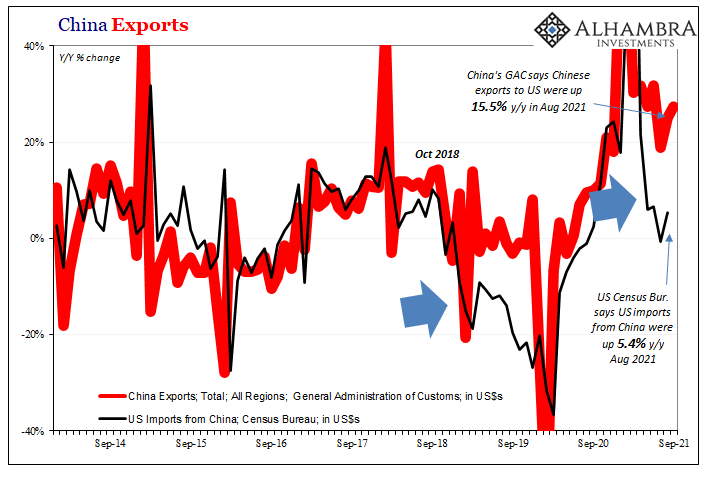

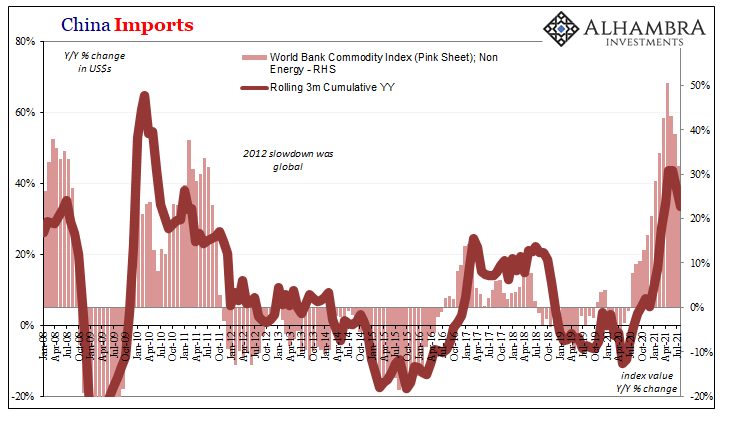

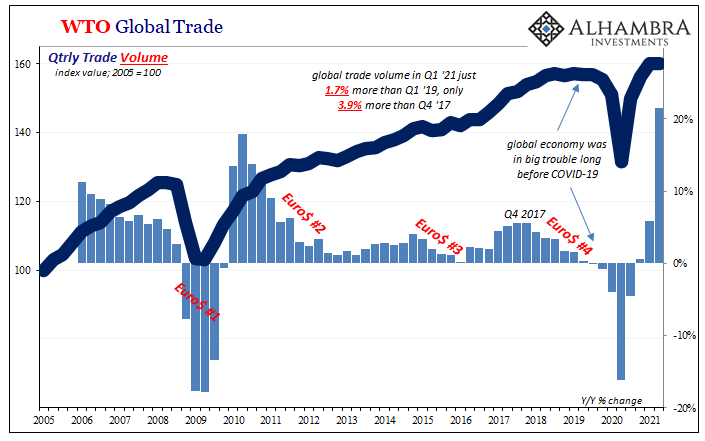

Inflating Chinese Trade15 Oct 2021

What’s Real Behind Commodities8 Sep 2021

A Real Example Of Price Imbalance11 Aug 2021

Real Dollar ‘Privilege’ On Display (again)8 Apr 2021

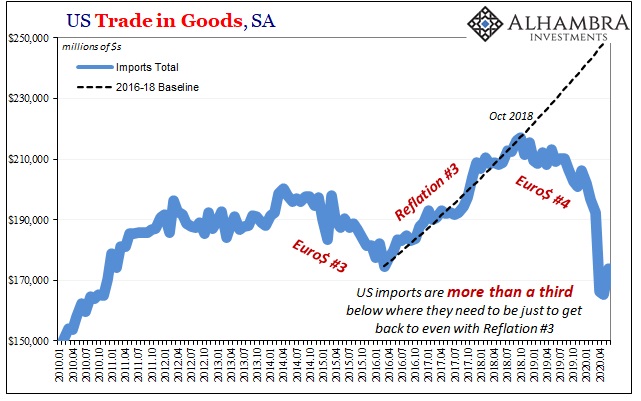

Shoe V arning8 Aug 2020

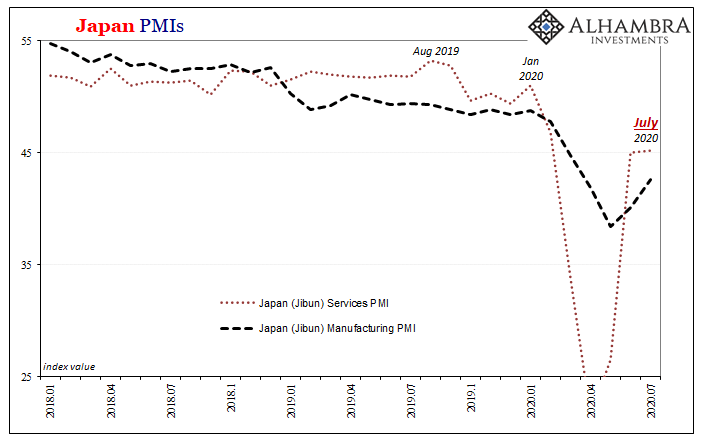

A Japanese Stall?24 Jul 2020

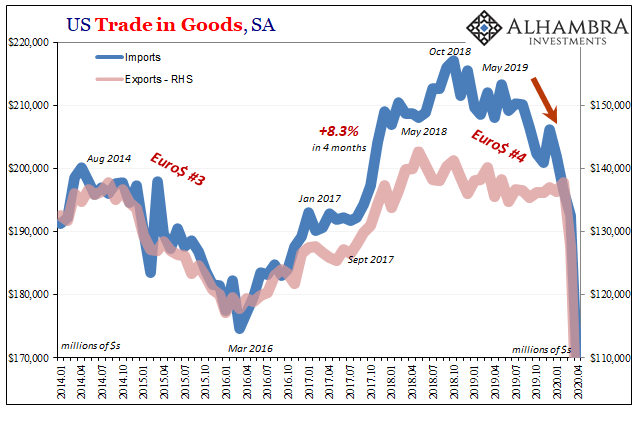

Second Wave Global Trade10 Jul 2020

Someone’s Giving Us The (Trade) Business9 Jun 2020

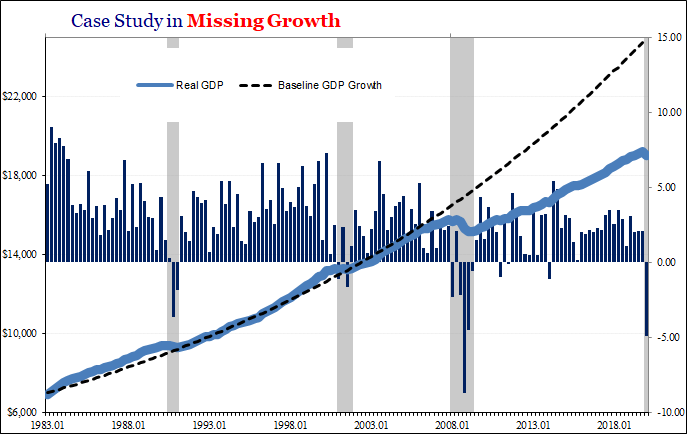

GDP + GFC = Fragile1 May 2020

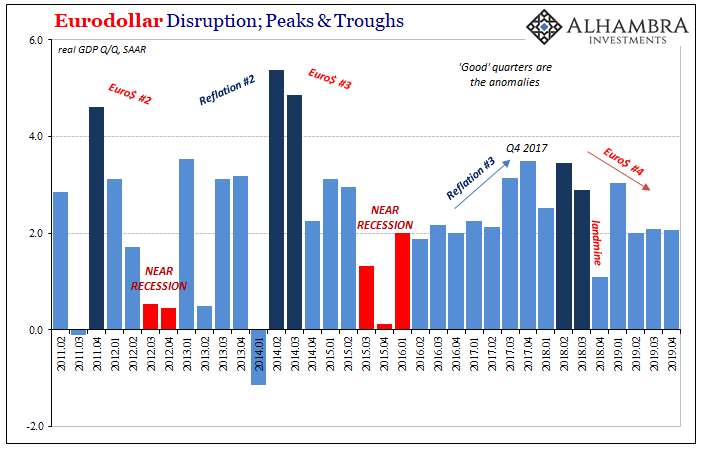

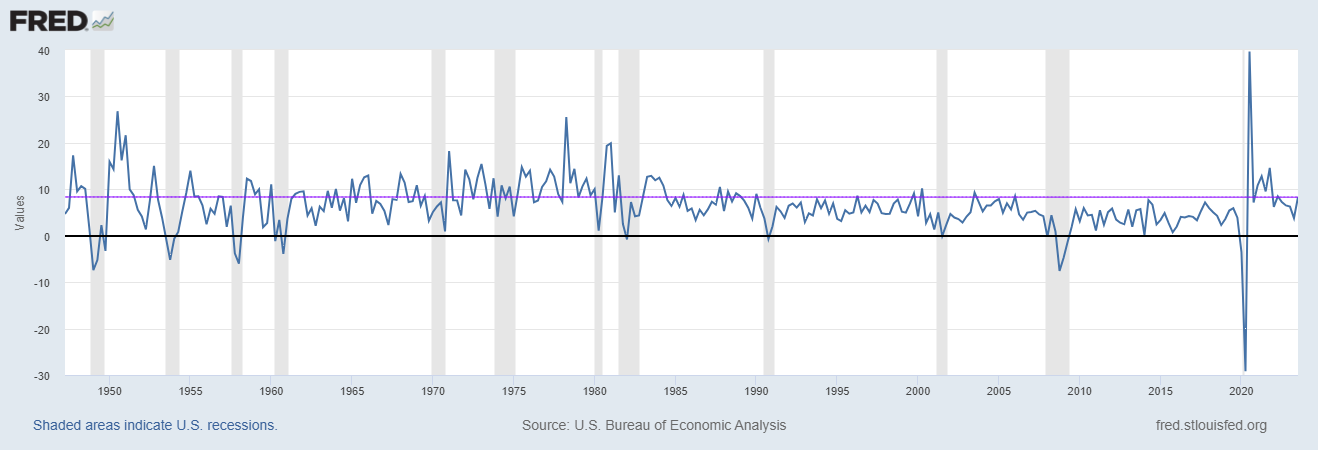

Three Straight Quarters of 2 percent, And Yet Each One Very Different2 Feb 2020