Read More »

On Swiss National Bank Main SNB Background Info

On Swiss National Bank Main SNB Background Info

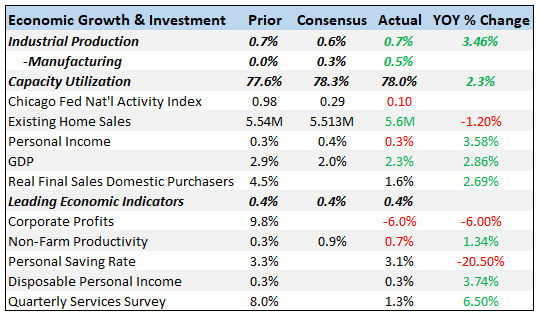

Weekly Market Pulse: Peak America?

Weekly Market Pulse: Peak America?21 Apr 2025

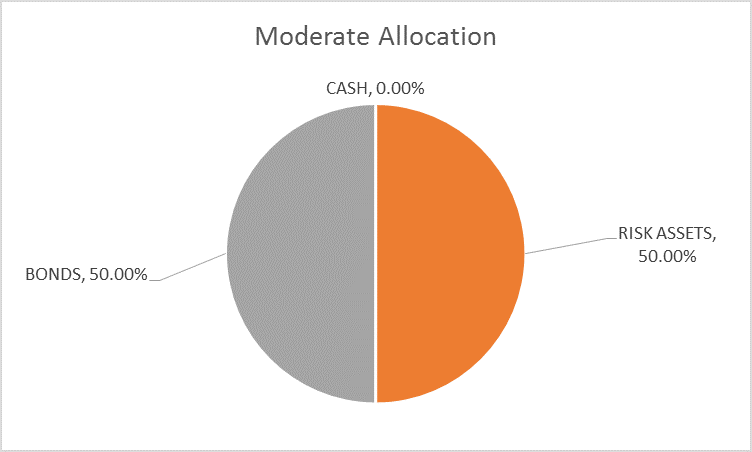

Weekly Market Pulse: Happy Days Are Here Again!

Weekly Market Pulse: Happy Days Are Here Again!7 Feb 2023

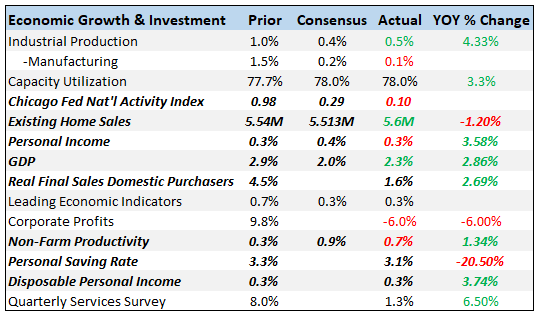

Weekly Market Pulse: The Real Reason The Fed Should Pause

Weekly Market Pulse: The Real Reason The Fed Should Pause11 Oct 2022

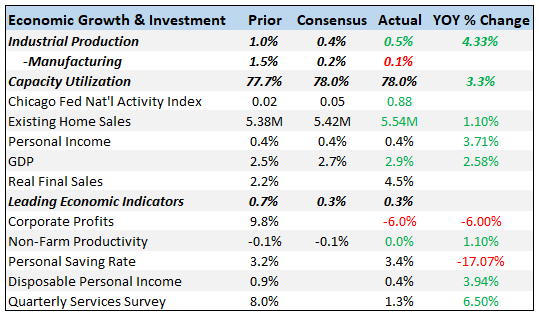

Weekly Market Pulse: No News Is…

Weekly Market Pulse: No News Is…12 Sep 2022

Weekly Market Pulse: Opposite George

Weekly Market Pulse: Opposite George1 Aug 2022

Weekly Market Pulse: There Is No Certainty In Investing

Weekly Market Pulse: There Is No Certainty In Investing18 Jul 2022

Weekly Market Pulse: A Most Unusual Economy

Weekly Market Pulse: A Most Unusual Economy11 Jul 2022

Weekly Market Pulse: Things That Need To Happen

Weekly Market Pulse: Things That Need To Happen5 Jul 2022

Market Pulse: Mid-Year Update

Market Pulse: Mid-Year Update24 Jun 2022

Weekly Market Pulse: Is The Bear Market Over?

Weekly Market Pulse: Is The Bear Market Over?31 May 2022

Weekly Market Pulse: TANSTAAFL

Weekly Market Pulse: TANSTAAFL16 May 2022

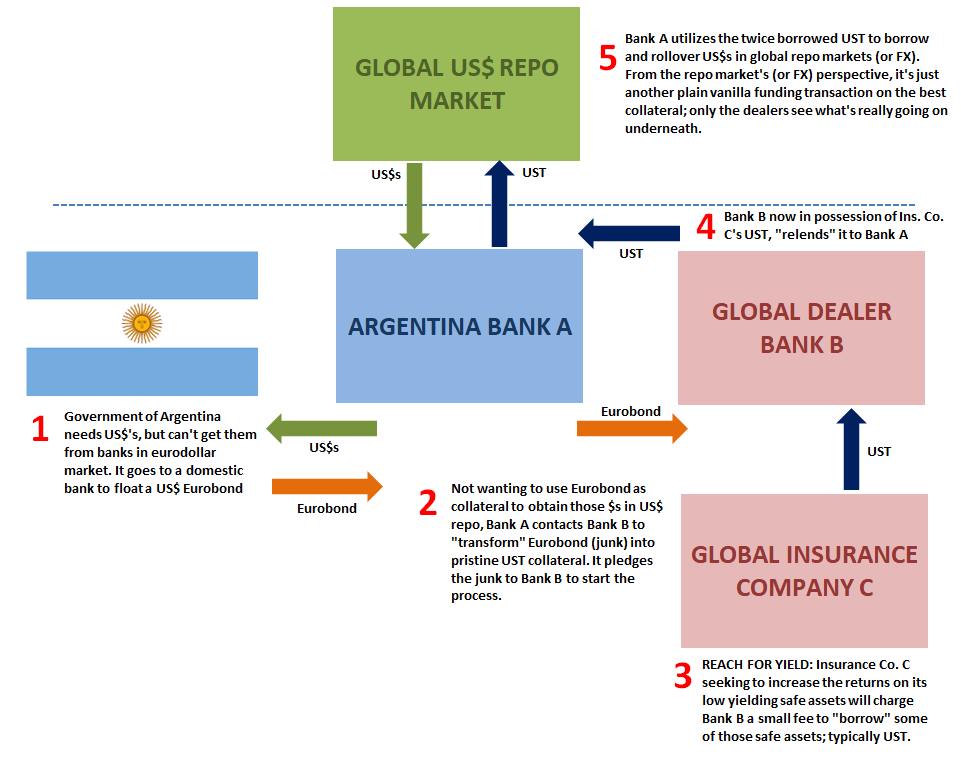

Eurobonds Behind Euro$ #5’s Collateral Case

Eurobonds Behind Euro$ #5’s Collateral Case12 May 2022

Weekly Market Pulse: Welcome Back To The Old Normal

Weekly Market Pulse: Welcome Back To The Old Normal3 May 2022

Weekly Market Pulse: What Now?

Weekly Market Pulse: What Now?5 Apr 2022

Weekly Market Pulse: The Cure For High Prices

Weekly Market Pulse: The Cure For High Prices31 Mar 2022

Weekly Market Pulse: Is This A Bear Market?

Weekly Market Pulse: Is This A Bear Market?16 Mar 2022

Weekly Market Pulse: Oil Shock

Weekly Market Pulse: Oil Shock8 Mar 2022

Weekly Market Pulse: Are We There Yet?

Weekly Market Pulse: Are We There Yet?31 Jan 2022

Weekly Market Pulse: Is It Time To Panic Yet?

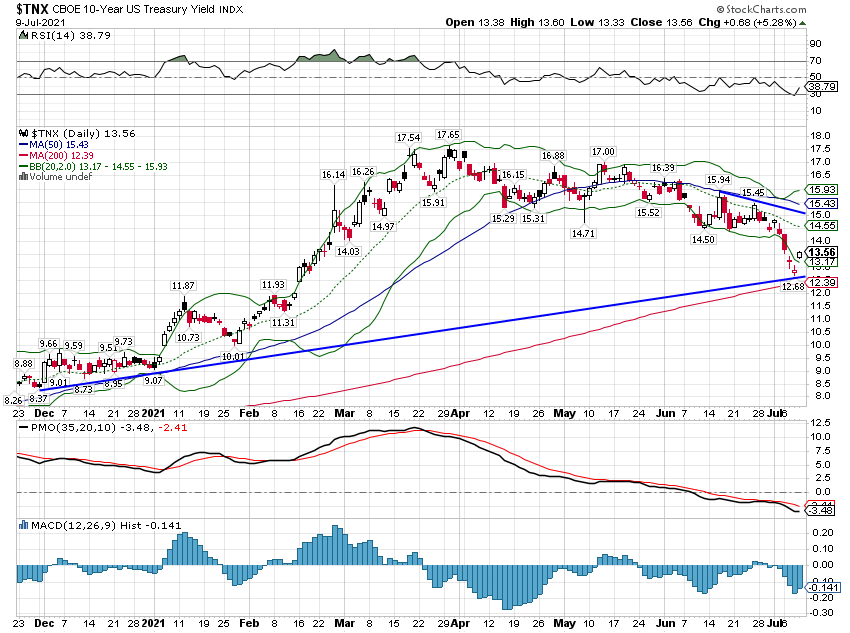

Weekly Market Pulse: Is It Time To Panic Yet?12 Jul 2021

Politics Get Weird, Markets Don’t Care

Politics Get Weird, Markets Don’t Care19 Jan 2021