Read More »

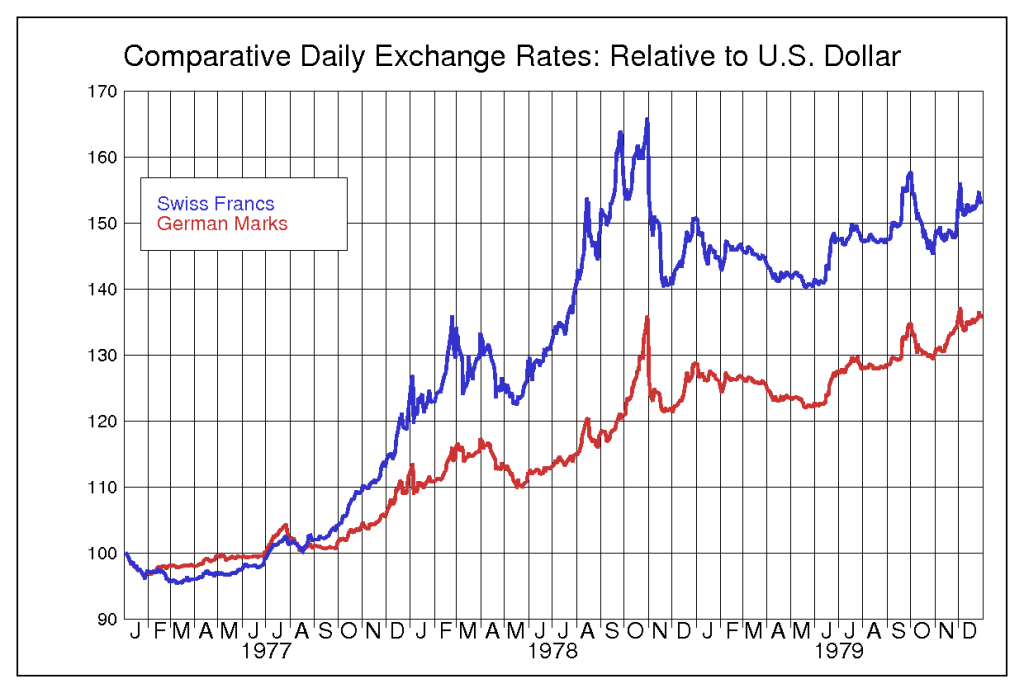

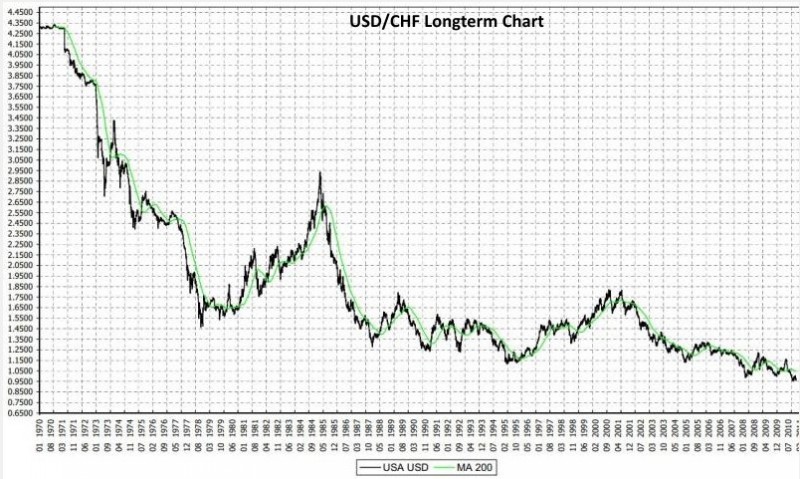

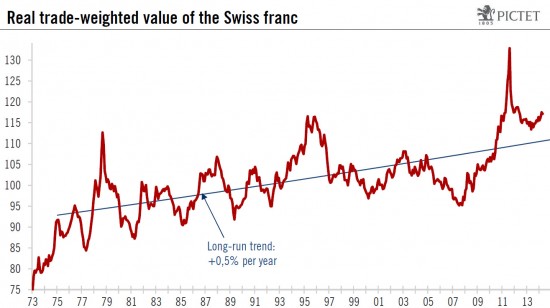

On Swiss National Bank Main SNB Background Info

On Swiss National Bank Main SNB Background Info

5-9-24 Finding The Next Apple Using Buffett’s Logic

5-9-24 Finding The Next Apple Using Buffett’s Logic9 May 2024

Skandal: AfD-Spitzenkandidat unter Spionageverdacht (aufgedeckt)

Skandal: AfD-Spitzenkandidat unter Spionageverdacht (aufgedeckt)9 May 2024

Wichtige Morning News mit Oliver Klemm #294

Wichtige Morning News mit Oliver Klemm #2949 May 2024

Stimmt! Wehrpflicht, Bürgergeld Studie, Migration – mit Schuler, Häusler, Zitelmann

Stimmt! Wehrpflicht, Bürgergeld Studie, Migration – mit Schuler, Häusler, Zitelmann8 May 2024

It’s a Power Shift!

It’s a Power Shift!8 May 2024

5 teure Mietwagen-Fehler

5 teure Mietwagen-Fehler8 May 2024

Perfekt abgesichert? So klappt’s | Geld ganz einfach

Perfekt abgesichert? So klappt’s | Geld ganz einfach8 May 2024

Top 15 teuerste Städte Deutschlands

Top 15 teuerste Städte Deutschlands8 May 2024

Hidden Costs of a Cashless Society: Rising Fees and Consumer Impact

Hidden Costs of a Cashless Society: Rising Fees and Consumer Impact8 May 2024

5-8-24 The Difference Between the Price You See vs the Price You Pay is Growing

5-8-24 The Difference Between the Price You See vs the Price You Pay is Growing8 May 2024

Rente: So viel bleibt übrig #rente

Rente: So viel bleibt übrig #rente8 May 2024

¿Quo Vadis, Presidente Sánchez?, con Juan Ramón Rallo

¿Quo Vadis, Presidente Sánchez?, con Juan Ramón Rallo8 May 2024

Deine MEGA-CHANCE am japanischen Aktienmarkt

Deine MEGA-CHANCE am japanischen Aktienmarkt8 May 2024

Wichtige Morning News mit Oliver Klemm #292

Wichtige Morning News mit Oliver Klemm #2928 May 2024

Wichtige Morning News mit Oliver Klemm #2938 May 2024

The secret to my success

The secret to my success7 May 2024

Love is the Most Important Soft Skill

Love is the Most Important Soft Skill7 May 2024

Trade Republic: Geschäftsmodell in Gefahr!

Trade Republic: Geschäftsmodell in Gefahr!7 May 2024

Quick Guide Selling Your Precious Metals to Money Metals Exchange

Quick Guide Selling Your Precious Metals to Money Metals Exchange7 May 2024

EURUSD trades to new lows for the day/week and approaches a key target support level

EURUSD trades to new lows for the day/week and approaches a key target support level7 May 2024