Read More »

Category Archive: 1) SNB and CHF

Death of an FX punter

Read More »

The liquidity monster and FXCM

As we have already pointed out about Thursday’s unprecedented Swiss franc move following the SNB’s announcement about removing its 1.20 euro level floor and introducing a -0.75 per cent interest rate regime, the real story to pay attention to is what...

Read More »

Read More »

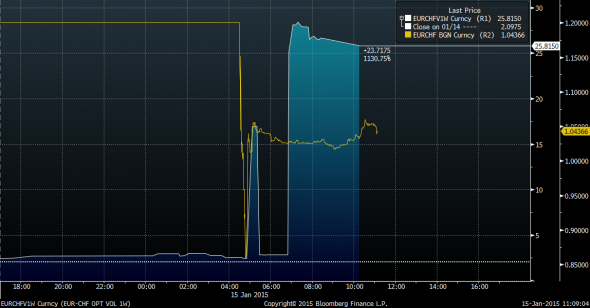

What did the SNB do to EURCHF options markets?

Read More »

Central Europe and the Swiss franc: Currency risk

Read More »

The SNB and the Russia/oil connection

A quick post to collate a few side theories on the reasons, justifications and consequences of the SNB move. Simon Derrick at BNY Mellon is first to point out that the euro floor/chf celing was leaving an open door to safe haven flows from Russia by ...

Read More »

Read More »

Currencies: Going cuckoo for the Swiss

Read More »

2014 Results: SNB expects profit of CHF 38 billion

Read More »

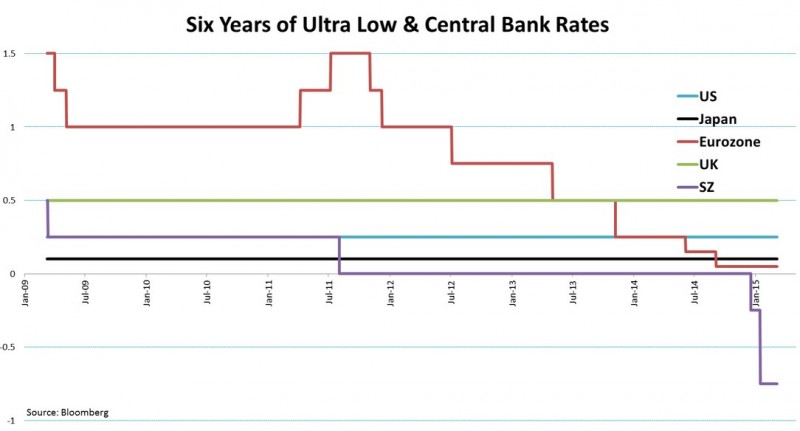

December 2014: SNB Introduces Negative Rates, a Toothless Measure?

Read More »

Setting monetary policy by popular vote: Full of holes

Read More »

Keith Weiner: SNB Must Keep Euro over 1.20 To Avoid Losses of Swiss Banks

Read More »

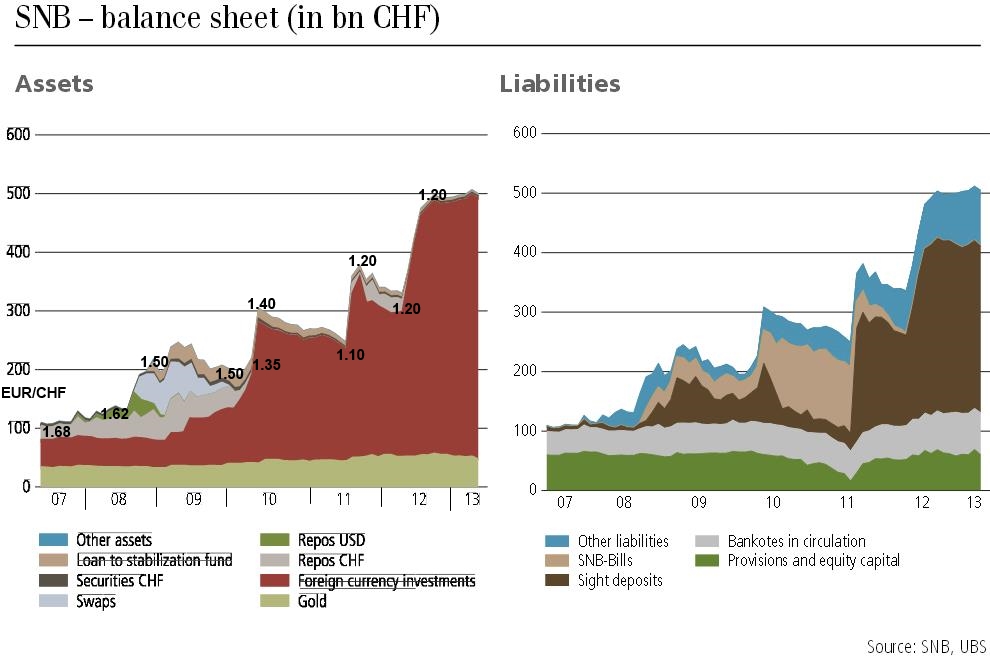

History of SNB Interventions

Read More »

Things That Make You Go Hmmm: This Little Piggy Bent The Market

Read More »

Sept 2014, George Dorgan at the CFA Society: Predicted End of EUR/CHF Peg

Read More »

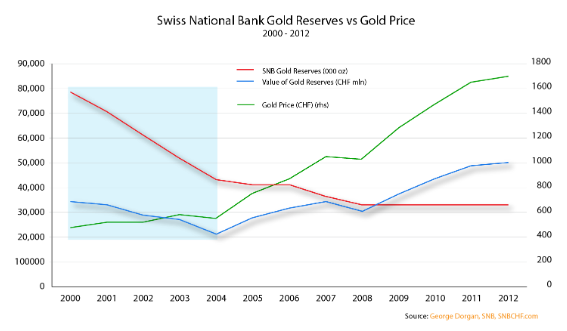

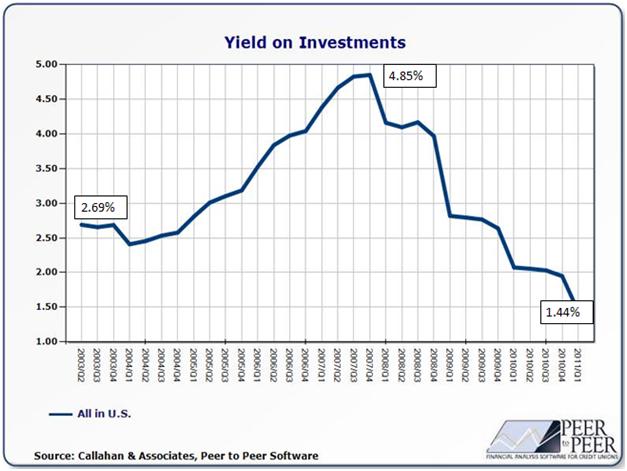

Will SNB FX Investments Yield Enough Until U.S. Inflation Starts?

Read More »

When FX wars become negative interest wars

Read More »

Swiss Franc and Swiss Economy: The Overview Questions

Read More »

On Swiss National Bank

-

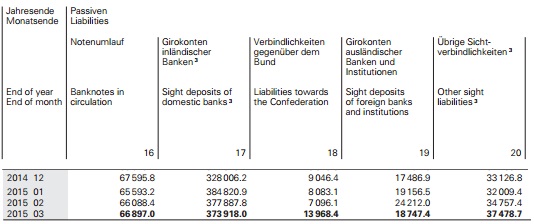

SNB Sight Deposits: decreased by 2.5 billion francs compared to the previous week

-

USD/CHF stays above 0.9100 nearing the highs since October

-

Pound Sterling falls back as upbeat US Retail Sales strengthen US Dollar

-

Canadian Dollar remains vulnerable after strong US Retail Sales

-

2024-04-09 – Martin Schlegel: Interest rates and foreign exchange interventions: Achieving price stability in challenging times

Main SNB Background Info

Featured and recent

-

Ampel schlittert in die Katastrophe!

-

Heftig: Aiwangers Ansage an Ricarda Lang!

-

Correctiv kassiert massive Klatsche vor Gericht!

-

Habeck scheitert an Prozentrechnung

Habeck scheitert an Prozentrechnung -

Neue Frist für Deine Steuererklärung #shorts

Neue Frist für Deine Steuererklärung #shorts -

Quick History of the Buffalo

Quick History of the Buffalo -

Be generous and expect generosity from others

Be generous and expect generosity from others -

New Taxes Proposed by White House as Inflation Rages

New Taxes Proposed by White House as Inflation Rages -

Völlige Eskalation in Grünheide!

Völlige Eskalation in Grünheide! -

#495 Eigenheim ohne reiche Oma – Das geleaste Zuhause #eigenheim

#495 Eigenheim ohne reiche Oma – Das geleaste Zuhause #eigenheim

More from this category

- USD/CHF stays above 0.9100 nearing the highs since October

16 Apr 2024

- Canadian Dollar remains vulnerable after strong US Retail Sales

15 Apr 2024

- Pound Sterling falls back as upbeat US Retail Sales strengthen US Dollar

15 Apr 2024

- 2024-04-09 – Martin Schlegel: Interest rates and foreign exchange interventions: Achieving price stability in challenging times

9 Apr 2024

- 2024-04-08 – Thomas Jordan: Towards the future monetary system

8 Apr 2024

Swiss Franc at risk as inflation diverges from SNB forecasts

Swiss Franc at risk as inflation diverges from SNB forecasts16 Mar 2024

EUR/CHF Price Analysis: Pullback possible amid mixed signals

EUR/CHF Price Analysis: Pullback possible amid mixed signals12 Mar 2024

- The Swiss National Bank vs. the Federal Reserve: The Fed’s Capital Losses in Perspective

12 Mar 2024

- US Dollar enters fourth day of consecutive losses ahead of Powell testimony

6 Mar 2024

-638453232816314704.png) Swiss Franc extends losses on Swiss interest rate outlook

Swiss Franc extends losses on Swiss interest rate outlook6 Mar 2024

Vorwort des Buches « L’Humanité vampirisée ». Philippe Bourcier de Carbon (version Allemande)

Vorwort des Buches « L’Humanité vampirisée ». Philippe Bourcier de Carbon (version Allemande)5 Mar 2024

USD/CHF Price Analysis: Trades back and forth around 0.8800

USD/CHF Price Analysis: Trades back and forth around 0.880027 Feb 2024

EUR/CHF hits ten-week highs above 0.9550 as Franc continues to soften

EUR/CHF hits ten-week highs above 0.9550 as Franc continues to soften26 Feb 2024

Sichtguthaben bei der SNB ziehen leicht an

Sichtguthaben bei der SNB ziehen leicht an26 Feb 2024

Parlamentskommission reicht in Credit-Suisse-Untersuchung Anzeige ein

Parlamentskommission reicht in Credit-Suisse-Untersuchung Anzeige ein23 Feb 2024

Forex Today: Pound Sterling weakens on soft UK inflation, US Dollar consolidates gains

Forex Today: Pound Sterling weakens on soft UK inflation, US Dollar consolidates gains14 Feb 2024

Gold price consolidates post-US CPI losses, seems vulnerable near two-month low

Gold price consolidates post-US CPI losses, seems vulnerable near two-month low14 Feb 2024

- USD/CHF retraces its recent gains on risk appetite, inches lower to near 0.8730

8 Feb 2024

USD/CHF heading for 0.8500 as Swiss Franc climbs into four-month high against Greenback

USD/CHF heading for 0.8500 as Swiss Franc climbs into four-month high against Greenback21 Dec 2023

- 2023-12-20 – 4/2023 – Business cycle signals: SNB regional network

20 Dec 2023