Read More »

On Swiss National Bank Main SNB Background Info

On Swiss National Bank Main SNB Background Info

Financial Savvy Ways To Thrive In The Auto Market

Financial Savvy Ways To Thrive In The Auto Market8 May 2023

Rückläufige US-Erdölvorräte lassen Ölpreise steigen

Rückläufige US-Erdölvorräte lassen Ölpreise steigen27 Jan 2022

United States: The ISM Conundrum

United States: The ISM Conundrum5 Sep 2019

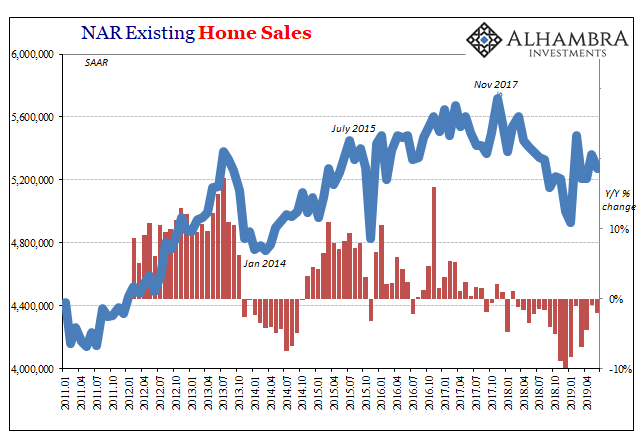

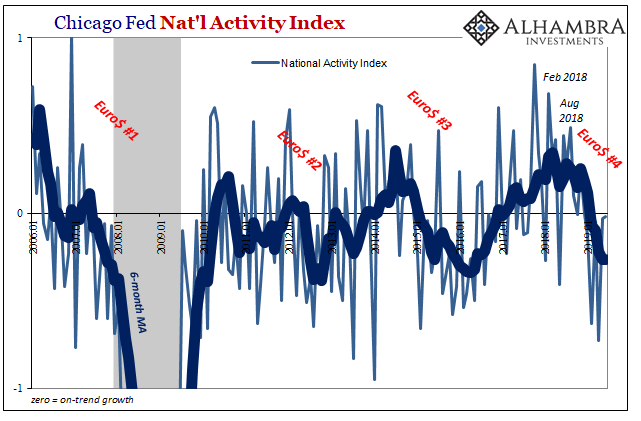

Latest Thoughts on the US Economic Outlook

Latest Thoughts on the US Economic Outlook4 Sep 2019

Real Estate Perfectly Sums Up The Rate Cuts

Real Estate Perfectly Sums Up The Rate Cuts28 Jul 2019

US Economic Crosscurrents Reach the 50 Mark

US Economic Crosscurrents Reach the 50 Mark27 Jul 2019

It’s Not Just the News That’s Fake–Everything’s Fake

It’s Not Just the News That’s Fake–Everything’s Fake26 Jul 2019

What Does It Mean That Real Estate, Not Equities, Is Driving Monetary Policy?

What Does It Mean That Real Estate, Not Equities, Is Driving Monetary Policy?25 Jul 2019

Our Ruling Elites Have No Idea How Much We Want to See Them All in Prison Jumpsuits

Our Ruling Elites Have No Idea How Much We Want to See Them All in Prison Jumpsuits22 Jul 2019

Monthly Macro Monitor: We’re Not There Yet

Monthly Macro Monitor: We’re Not There Yet21 Jul 2019

Globally Synchronized, After All

Globally Synchronized, After All20 Jul 2019

US FX intervention still someway off

US FX intervention still someway off19 Jul 2019

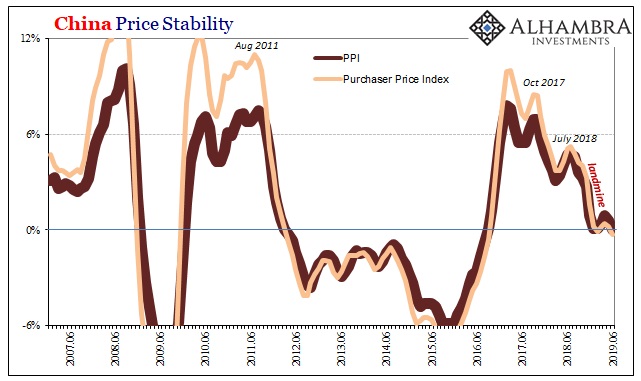

As Chinese Factory Deflation Sets In, A ‘Dovish’ Powell Leans on ‘Uncertainty’

As Chinese Factory Deflation Sets In, A ‘Dovish’ Powell Leans on ‘Uncertainty’14 Jul 2019

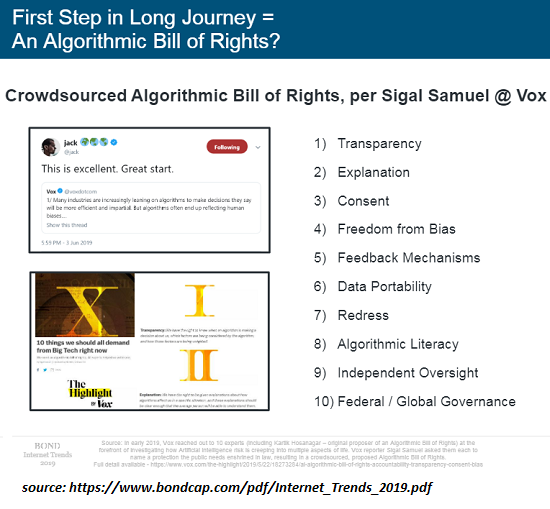

“Alexa, How Do We Subvert Big Tech’s Orwellian Internet-of-Things Surveillance?”

“Alexa, How Do We Subvert Big Tech’s Orwellian Internet-of-Things Surveillance?”12 Jul 2019

Predatory “Green Capitalism” Is Monetizing the Air, and It’s Going to Cost You

Predatory “Green Capitalism” Is Monetizing the Air, and It’s Going to Cost You10 Jul 2019

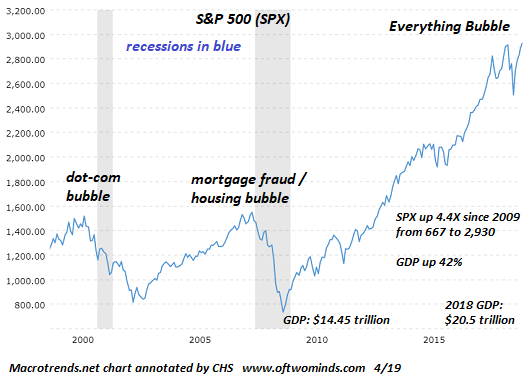

When Everything from Bat Guano to Quatloos Is Soaring, Speculative Euphoria Has Reached an Extreme

When Everything from Bat Guano to Quatloos Is Soaring, Speculative Euphoria Has Reached an Extreme8 Jul 2019

Vested Interests in Charge = Guaranteed Failure

Vested Interests in Charge = Guaranteed Failure6 Jul 2019

What’s Left to Monetize?

What’s Left to Monetize?5 Jul 2019

America’s Concealed Crisis: Fifty Years of Economic Decline, 1969 to 2019

America’s Concealed Crisis: Fifty Years of Economic Decline, 1969 to 20192 Jul 2019

Following in Rome’s Footsteps: Moral Decay, Rising Inequality

Following in Rome’s Footsteps: Moral Decay, Rising Inequality1 Jul 2019