The U.S. economy regularly improves between October and March. This year the improvement was a bit earlier thanks to QE3. By March the economy already weakened according to the latest ISM PMIs.

Read More »

Category Archive: 5) Global Macro

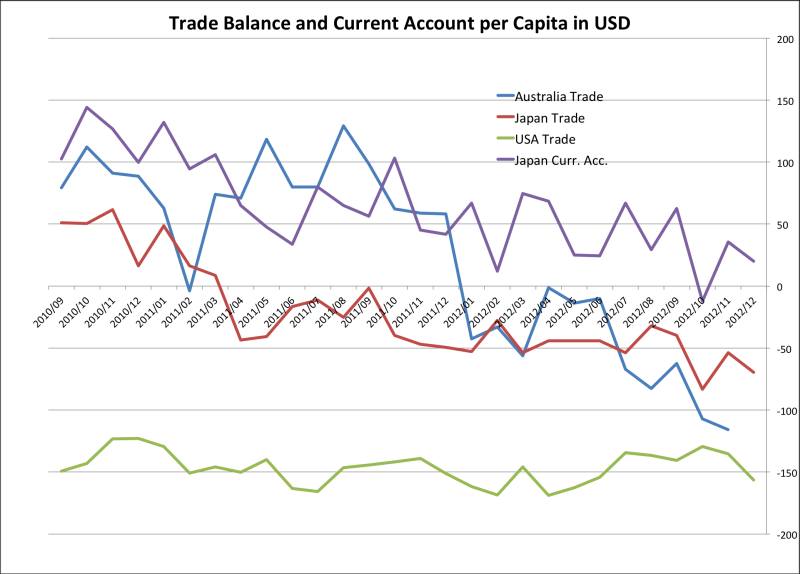

Japanese Currency Debasement, Part 1: Current Account and Japanese Bond Bears

Read More »

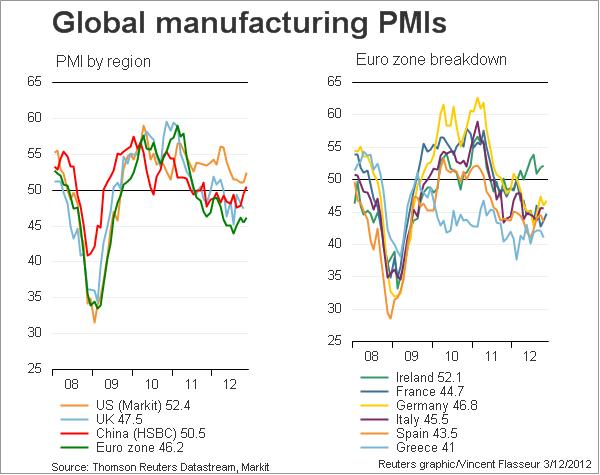

Global Purchasing Manager Indices, Update January 25

Read More »

Roubini and Deutsche Bank’s Sanjeev Sanyal: Still Waiting for the Chinese Consumer

Read More »

Epic Shift in Monetary Policy: Japan goes SNB, Nuclear Option

Read More »

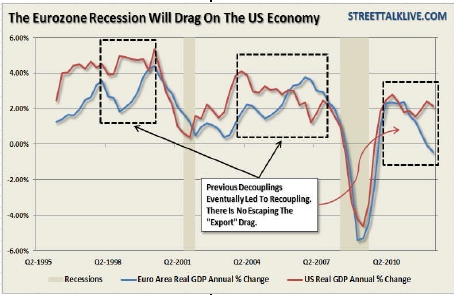

Same Procedure as Every Year: Analysts Shouting “The Great Recession is Over!” But It Is Not!

Read More »

2012 Posts on Global Macro

Debt, the Financial Cycle Determinant between 2011 and 2017

Read More »

Quantitative Easing, Gold and the Swiss Franc

Read More »

The Biggest Bubble of the Century is Ending: Government Bond Yields

Read More »

Global Purchasing Manager Indices, Update December 17

Read More »

Main US Economic Indicators

Read More »

Global Purchasing Manager Indices, Update December 10

Read More »

Die Wiederwahl Obamas bedeutet nichts Gutes für die Schweiz

Read More »

Who Has Got the Problem? Europe or Japan?

Read More »

Again Flawed Data for Jobs

Read More »

IMF World Economic Outlook

Read More »

Conspiracy? Why the Jobs Report Was not Cooked, but simply Flawed

Read More »

The “Beautiful” De-Leveraging

Read More »

It’s not simply QE3

Read More »

On Swiss National Bank

On Swiss National Bank

-

USD/CHF stays above 0.9100 nearing the highs since October

-

SNB Sight Deposits: increased by 17.0 billion francs compared to the previous week

-

Pound Sterling falls back as upbeat US Retail Sales strengthen US Dollar

-

Canadian Dollar remains vulnerable after strong US Retail Sales

-

2024-04-09 – Martin Schlegel: Interest rates and foreign exchange interventions: Achieving price stability in challenging times

Main SNB Background Info

Featured and recent

-

Supergau für Jens Spahn wegen RKI Files!

Supergau für Jens Spahn wegen RKI Files! -

Kentucky Becomes 45th State to End Sales Taxes on Gold and Silver

-

STARKES Umfeld, STARKE Renditen: Ein (Börsen-)Jahr voller Erfolg

STARKES Umfeld, STARKE Renditen: Ein (Börsen-)Jahr voller Erfolg -

Javier Milei vs. the Status Quo

-

The Problem with Microlibertarianism

-

Habeck Files: Die Grüne Kernschmelze!

Habeck Files: Die Grüne Kernschmelze! -

The Danger of the West’s Neglect of Individual Rights

-

Bodemann flippt aus: “Wir brauchen mehr Kontrolle”

Bodemann flippt aus: “Wir brauchen mehr Kontrolle” -

The Evil of War

-

Deutscher General: “Wir arbeiten an Operationsplan Deutschland”

Deutscher General: “Wir arbeiten an Operationsplan Deutschland”

More from this category

Supergau für Jens Spahn wegen RKI Files!

Supergau für Jens Spahn wegen RKI Files!25 Apr 2024

STARKES Umfeld, STARKE Renditen: Ein (Börsen-)Jahr voller Erfolg

STARKES Umfeld, STARKE Renditen: Ein (Börsen-)Jahr voller Erfolg25 Apr 2024

Habeck Files: Die Grüne Kernschmelze!

Habeck Files: Die Grüne Kernschmelze!25 Apr 2024

Bodemann flippt aus: “Wir brauchen mehr Kontrolle”

Bodemann flippt aus: “Wir brauchen mehr Kontrolle”25 Apr 2024

Deutscher General: “Wir arbeiten an Operationsplan Deutschland”

Deutscher General: “Wir arbeiten an Operationsplan Deutschland”25 Apr 2024

Wichtige Morning News mit Oliver Klemm #288

Wichtige Morning News mit Oliver Klemm #28825 Apr 2024

Wichtige Morning News mit Oliver Klemm #289

Wichtige Morning News mit Oliver Klemm #28925 Apr 2024

Understanding Elliott Wave Theory and Investment Strategies – Andy Tanner and Bob Prechter

Understanding Elliott Wave Theory and Investment Strategies – Andy Tanner and Bob Prechter24 Apr 2024

4-20-24 Candid Coffee – Open Season Episode

4-20-24 Candid Coffee – Open Season Episode24 Apr 2024

Habecks Geheimakten enthüllt!

Habecks Geheimakten enthüllt!24 Apr 2024

Diese Aktien sind extrem günstig!

Diese Aktien sind extrem günstig!24 Apr 2024

Bitcoin Price Prediction and the Future of Crypto – Robert Kiyosaki, Mark Moss

Bitcoin Price Prediction and the Future of Crypto – Robert Kiyosaki, Mark Moss24 Apr 2024

Gold Price Just Dropped! What Happened? (2024 Update)

Gold Price Just Dropped! What Happened? (2024 Update)24 Apr 2024

The DNA of Success: Habits of Millionaires Unveiled

The DNA of Success: Habits of Millionaires Unveiled24 Apr 2024

Who’s to Blame for Inflation?

Who’s to Blame for Inflation?24 Apr 2024

Will gold prices keep rising in 2024? #gold #inflation #goldprice #preciousmetals

Will gold prices keep rising in 2024? #gold #inflation #goldprice #preciousmetals24 Apr 2024

4-24-24 What Does Realistic Retirement Look Like?

4-24-24 What Does Realistic Retirement Look Like?24 Apr 2024

Eklat: Grünen Politiker wirft genervt hin!

Eklat: Grünen Politiker wirft genervt hin!24 Apr 2024

Die größten Tagesgewinne an der Börse! #highlife

Die größten Tagesgewinne an der Börse! #highlife24 Apr 2024

Marktausblick Mit Stefan Breintner und Markus Koch April 2024

Marktausblick Mit Stefan Breintner und Markus Koch April 202424 Apr 2024