Alhambra CEO Joe Calhoun responds to questions about a slowing economy, long-term economic impacts of COVID, stock prices and the business cycle.

Read More »

Category Archive: 5) Global Macro

The Banality of (Financial) Evil

Read More »

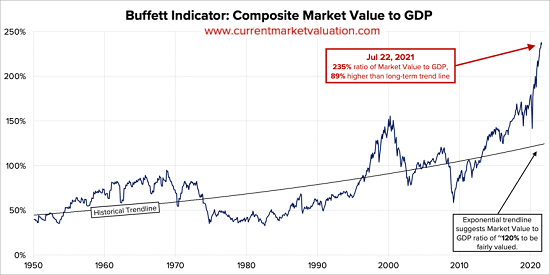

Please Don’t Pop Our Precious Bubble!

Read More »

Weekly Market Pulse (VIDEO)

Read More »

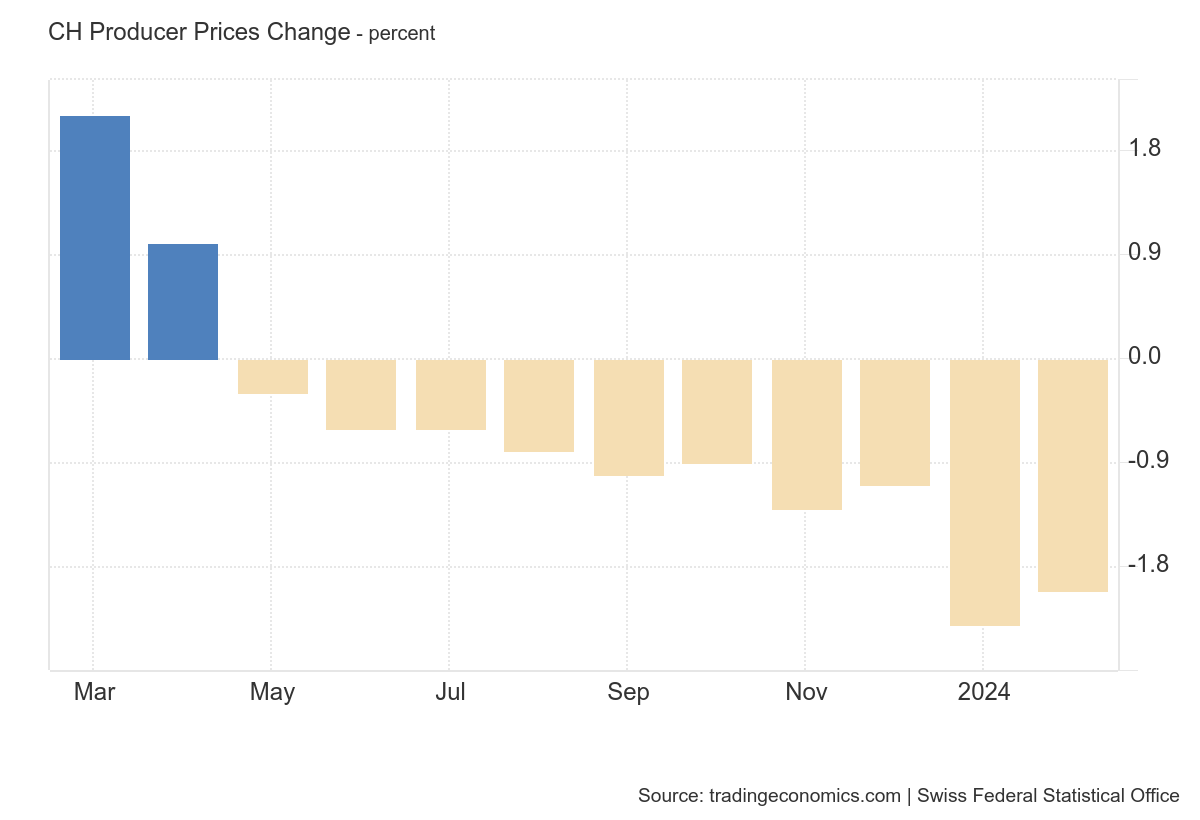

What’s Real Behind Commodities

Read More »

The Upside of a Stock Market Crash

Read More »

The Smart Money Has Already Sold

Read More »

Taper *Without* Tantrum

Read More »

Why the Global Economy Is Unraveling

Read More »

Weekly Market Pulse: Happy Anniversary!

Read More »

CPI’s At Fives Yet Treasury Auctions

Read More »

Dear Fed: Are You Insane?

Read More »

A Real Example Of Price Imbalance

Read More »

The Two Big Anniversaries of August: The Lost Decade (plus) Of The ‘Fiat’ Half Century

Read More »

The End of Global Tourism?

Read More »

Weekly Market Pulse: What Is Today’s New Normal?

Read More »

While the Herd Slumbers, Risk Is Rocketing Higher

Read More »

Sophistry Dressed (as) Reallocation

Read More »

The Moment Wall Street Has Been Waiting For: Retail Is All In

Read More »

Golden Collateral Checking

Read More »

On Swiss National Bank

On Swiss National Bank

-

SNB Sight Deposits: increased by 17.0 billion francs compared to the previous week

-

Swiss Franc at risk as inflation diverges from SNB forecasts

-

The Swiss National Bank vs. the Federal Reserve: The Fed’s Capital Losses in Perspective

-

EUR/CHF Price Analysis: Pullback possible amid mixed signals

-

-638453232816314704.png)

Swiss Franc extends losses on Swiss interest rate outlook

Main SNB Background Info

Featured and recent

-

SNB Sight Deposits: increased by 17.0 billion francs compared to the previous week

SNB Sight Deposits: increased by 17.0 billion francs compared to the previous week -

The Real Impact of Financial Policies on Your Wallet – John MacGregor

The Real Impact of Financial Policies on Your Wallet – John MacGregor -

Required Reading: 25th Anniversary Rothbard Graduate Seminar

-

Risk Management Tips for Investors – Andy Tanner

Risk Management Tips for Investors – Andy Tanner -

Bitcoin: Das darf JETZT NICHT passieren!

Bitcoin: Das darf JETZT NICHT passieren! -

Spektakulär FALSCH: Habecks desolates Video!

Spektakulär FALSCH: Habecks desolates Video! -

THe USDCHF traded to a new 2024 high, but failed.What would increase the bearish bias now?

THe USDCHF traded to a new 2024 high, but failed.What would increase the bearish bias now? -

Kickstart the FX trading day on April 15 with a technical look at EURUSD, USDJPY & GBPUSD

Kickstart the FX trading day on April 15 with a technical look at EURUSD, USDJPY & GBPUSD -

Human Action on Its 75th Anniversary Helps Us Understand How Statism Has Decimated Argentina

-

Japan: Massive Demos gegen WHO Pandemievertrag!

Japan: Massive Demos gegen WHO Pandemievertrag!

More from this category

The Real Impact of Financial Policies on Your Wallet – John MacGregor

The Real Impact of Financial Policies on Your Wallet – John MacGregor15 Apr 2024

Risk Management Tips for Investors – Andy Tanner

Risk Management Tips for Investors – Andy Tanner15 Apr 2024

Bitcoin: Das darf JETZT NICHT passieren!

Bitcoin: Das darf JETZT NICHT passieren!15 Apr 2024

Spektakulär FALSCH: Habecks desolates Video!

Spektakulär FALSCH: Habecks desolates Video!15 Apr 2024

THe USDCHF traded to a new 2024 high, but failed.What would increase the bearish bias now?

THe USDCHF traded to a new 2024 high, but failed.What would increase the bearish bias now?15 Apr 2024

Kickstart the FX trading day on April 15 with a technical look at EURUSD, USDJPY & GBPUSD

Kickstart the FX trading day on April 15 with a technical look at EURUSD, USDJPY & GBPUSD15 Apr 2024

Japan: Massive Demos gegen WHO Pandemievertrag!

Japan: Massive Demos gegen WHO Pandemievertrag!15 Apr 2024

Gold Technical Analysis – WATCH this key levels for the next direction

Gold Technical Analysis – WATCH this key levels for the next direction15 Apr 2024

Wichtige Morning News mit Oliver Klemm #282

Wichtige Morning News mit Oliver Klemm #28215 Apr 2024

LA IZQUIERDA NO QUIERE QUE SEPAS LO QUE PAGAS EN IMPUESTOS

LA IZQUIERDA NO QUIERE QUE SEPAS LO QUE PAGAS EN IMPUESTOS14 Apr 2024

Gerichtsurteil gegen Sparkasse! JETZT Gebühren zurückholen!

Gerichtsurteil gegen Sparkasse! JETZT Gebühren zurückholen!14 Apr 2024

El GRAN LOGRO de MILEI

El GRAN LOGRO de MILEI14 Apr 2024

Brandenburg tobt: “Uneidliche Falschaussagen im Corona-Ausschuss!”

Brandenburg tobt: “Uneidliche Falschaussagen im Corona-Ausschuss!”14 Apr 2024

Coca-Cola vs Pepsi 🥤#cola #pepsi

Coca-Cola vs Pepsi 🥤#cola #pepsi14 Apr 2024

Was ist der SANUSCOIN?

Was ist der SANUSCOIN?14 Apr 2024

Flexibel durch Deine 60er #shorts

Flexibel durch Deine 60er #shorts14 Apr 2024

Performt dein ETF WIRKLICH so gut wie sein Index?

Performt dein ETF WIRKLICH so gut wie sein Index?14 Apr 2024

Pkw Fahrverbote 2024: Lindner teilt massiv gegen Grüne aus!

Pkw Fahrverbote 2024: Lindner teilt massiv gegen Grüne aus!14 Apr 2024

Macht die neue FlexCo für mich als Unternehmer Sinn?

Macht die neue FlexCo für mich als Unternehmer Sinn?14 Apr 2024

Geldmaschine Volatrading? Infos zum Reverse Split im UVXY

Geldmaschine Volatrading? Infos zum Reverse Split im UVXY14 Apr 2024