Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

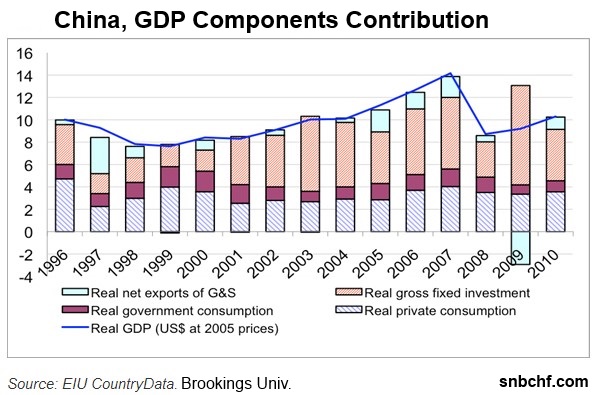

Currency update – the Chinese renminbi

Currency update – the Chinese renminbi9 Aug 2019

Real Estate Perfectly Sums Up The Rate Cuts

Real Estate Perfectly Sums Up The Rate Cuts28 Jul 2019

What Does It Mean That Real Estate, Not Equities, Is Driving Monetary Policy?

What Does It Mean That Real Estate, Not Equities, Is Driving Monetary Policy?25 Jul 2019

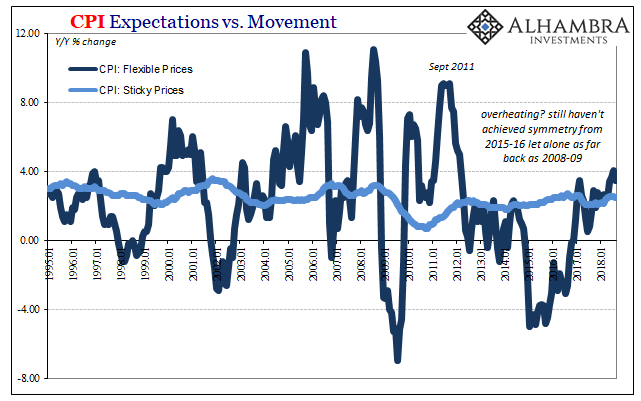

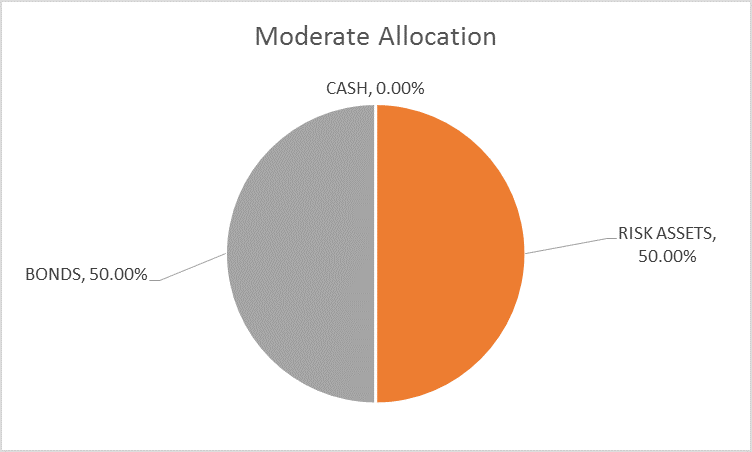

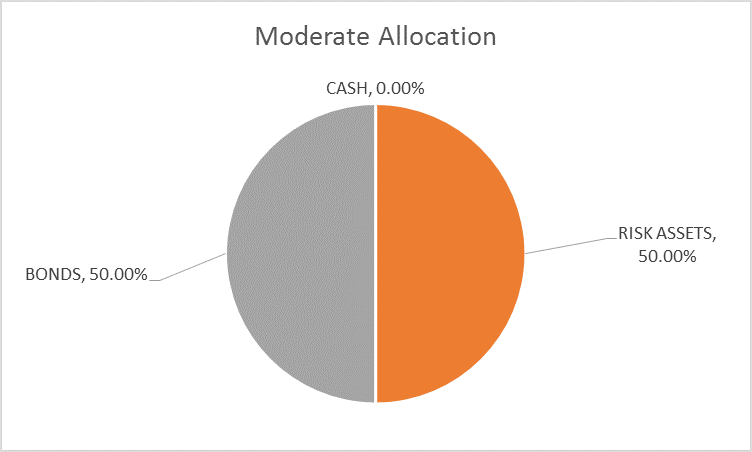

Monthly Macro Monitor: We’re Not There Yet

Monthly Macro Monitor: We’re Not There Yet21 Jul 2019

Globally Synchronized, After All

Globally Synchronized, After All20 Jul 2019

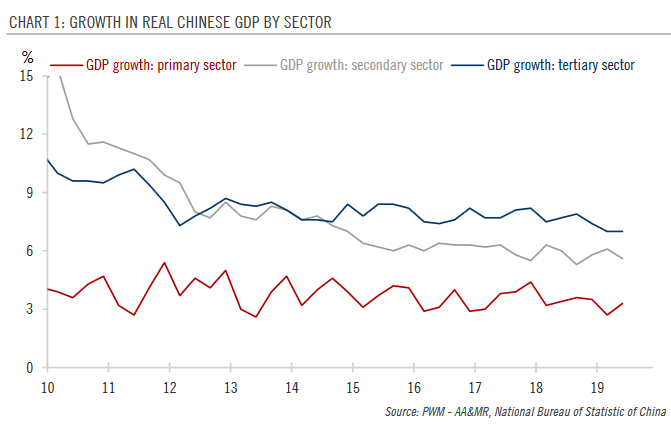

China: Q2 growth lowest in decades

China: Q2 growth lowest in decades17 Jul 2019

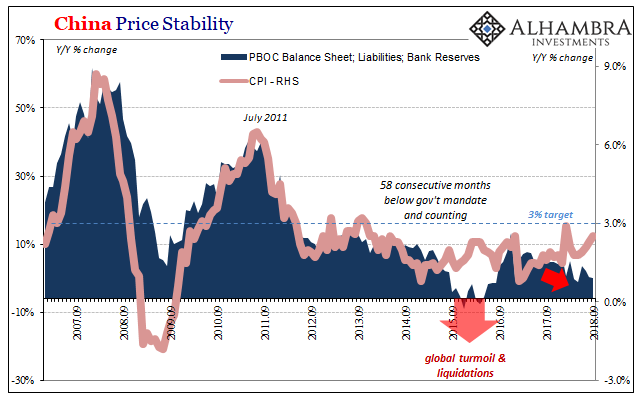

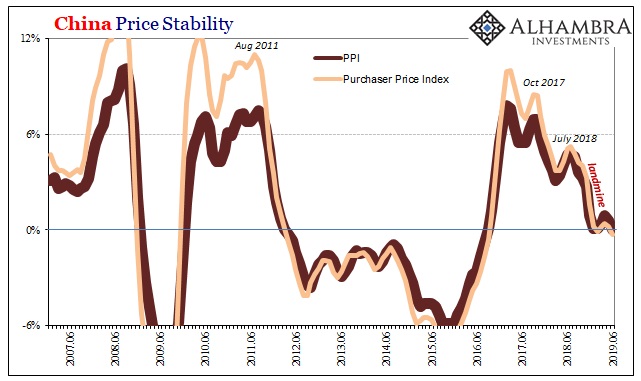

As Chinese Factory Deflation Sets In, A ‘Dovish’ Powell Leans on ‘Uncertainty’

As Chinese Factory Deflation Sets In, A ‘Dovish’ Powell Leans on ‘Uncertainty’14 Jul 2019

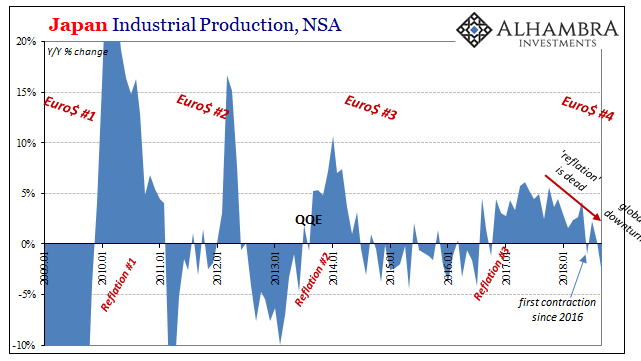

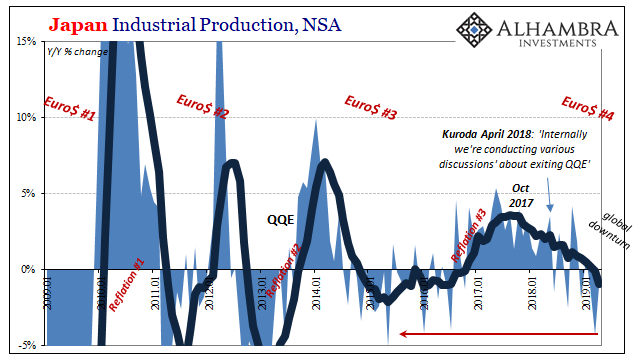

Japan’s Bellwether On Nasty #4

Japan’s Bellwether On Nasty #425 Jun 2019

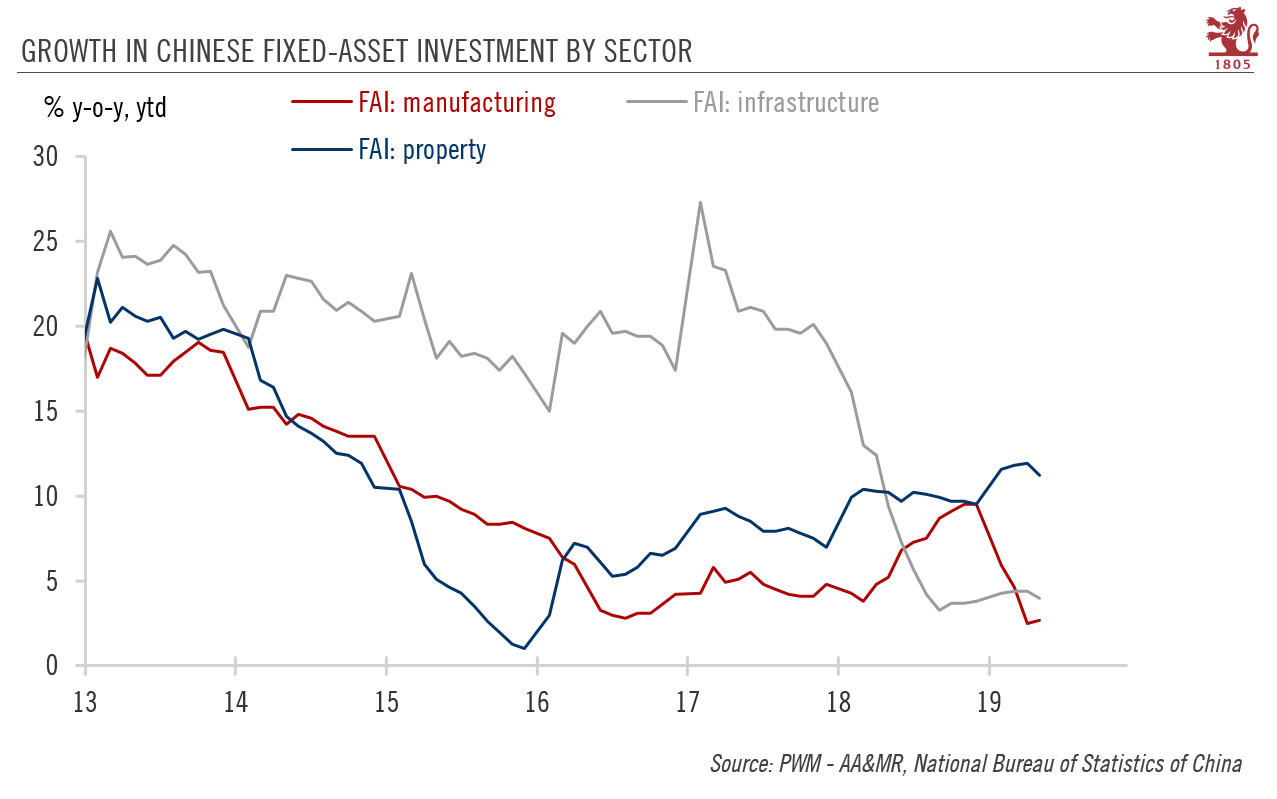

China looks to new policies to boost infrastructure spending

China looks to new policies to boost infrastructure spending19 Jun 2019

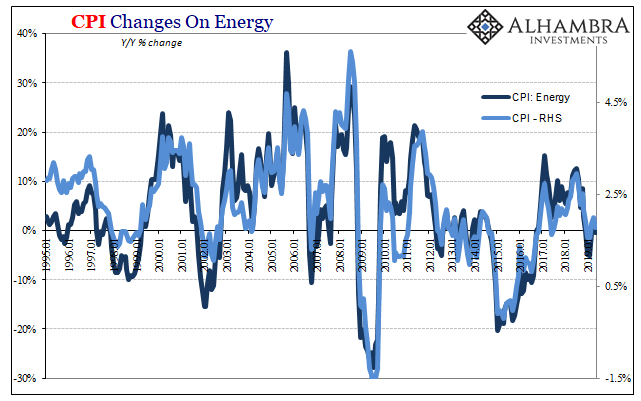

When Verizons Multiply, Macro In Inflation

When Verizons Multiply, Macro In Inflation16 Jun 2019

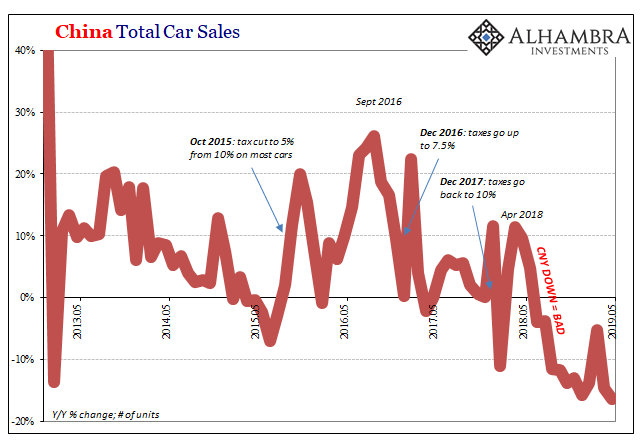

Dimmed Hopes In China Cars, Too

Dimmed Hopes In China Cars, Too15 Jun 2019

Commodities And The Future Of China’s Stall

Commodities And The Future Of China’s Stall13 Jun 2019

All Of US Trade, Both Ways, And Much, Much More Than The Past Few Months

All Of US Trade, Both Ways, And Much, Much More Than The Past Few Months10 Jun 2019

Janus Powell

Janus Powell9 Jun 2019

Monthly Macro Monitor – June 2019 (VIDEO)

Monthly Macro Monitor – June 2019 (VIDEO)8 Jun 2019

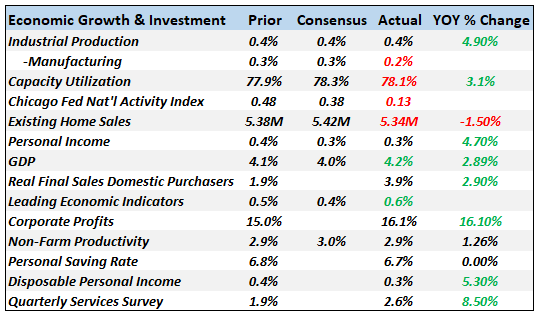

Monthly Macro Monitor: Economic Reports

Monthly Macro Monitor: Economic Reports4 Jun 2019

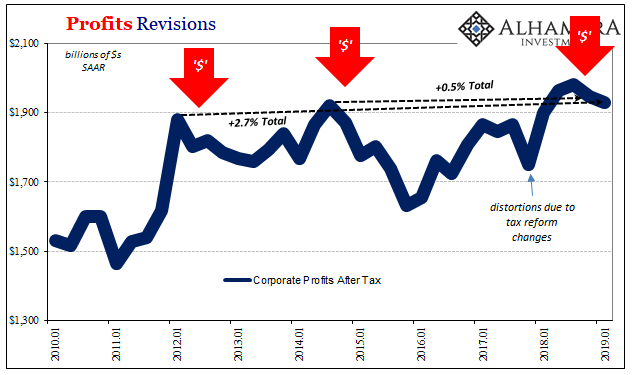

More What’s Behind Yield Curve: Now Two Straight Negative Quarters For Corporate Profit

More What’s Behind Yield Curve: Now Two Straight Negative Quarters For Corporate Profit1 Jun 2019

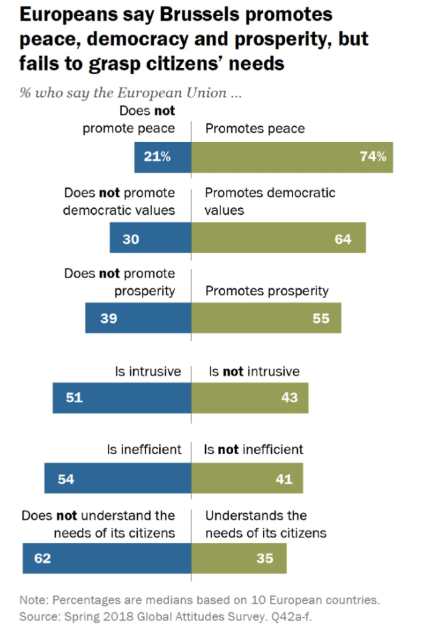

Europe Comes Apart, And That’s Before #4

Europe Comes Apart, And That’s Before #430 May 2019

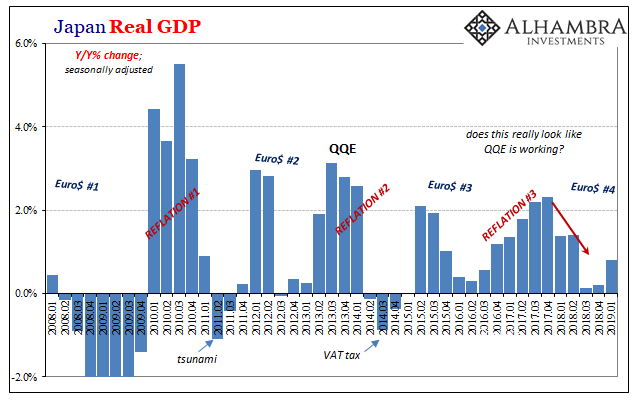

Japan’s Surprise Positive Is A Huge Minus

Japan’s Surprise Positive Is A Huge Minus21 May 2019

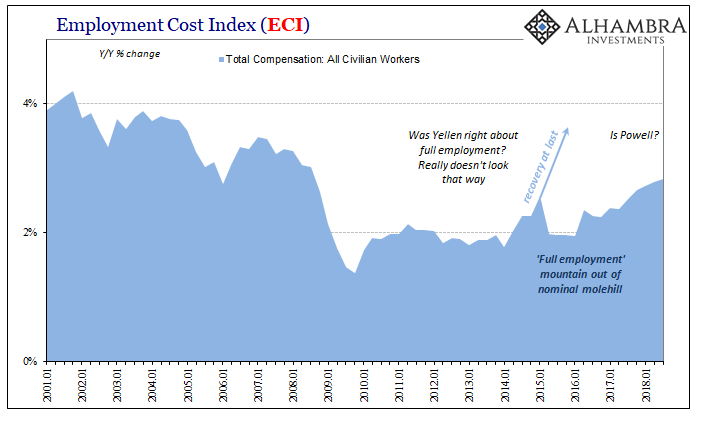

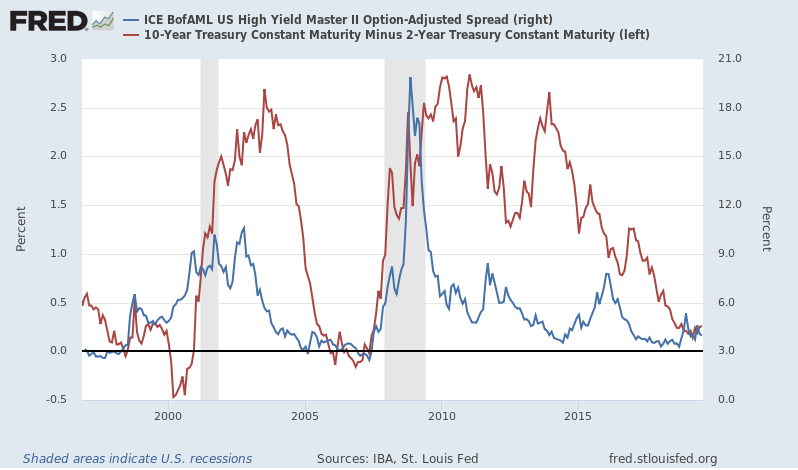

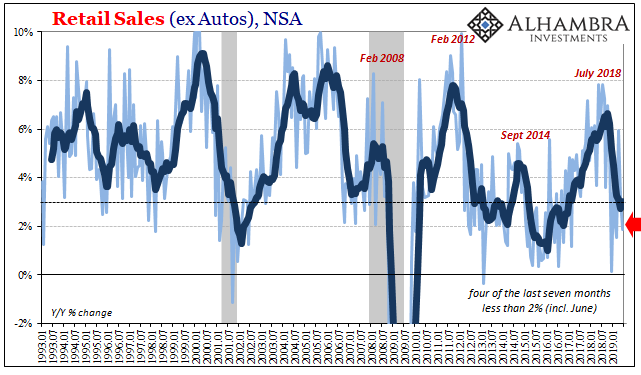

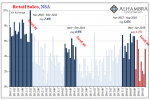

Global Doves Expire: Fed Pause Fizzles (US Retail Sales)

Global Doves Expire: Fed Pause Fizzles (US Retail Sales)18 May 2019