Jeffrey P. Snider

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

| It was for a time a somewhat curious dilemma. When it rains it pours, they always say, and for China toward the end of 2015 it was a real cloudburst. The Chinese economy was slowing, dangerous deflation developing around an economy captured by an unseen anchor intent on causing havoc and destruction. At the same time, consumer prices were jumping where they could do the most harm.

The Chinese had a pork problem in 2015, an outgrowth of central state-injected imbalance. To put it simply, there had been before 2014 too many producers causing pork prices to fall, exposing many especially small firms to the backlash of oversupply, which then put China in no position to respond flexibly to an outbreak of disease. Pork prices toward the end of 2015 skyrocketed just as the economy could least afford the disturbance. |

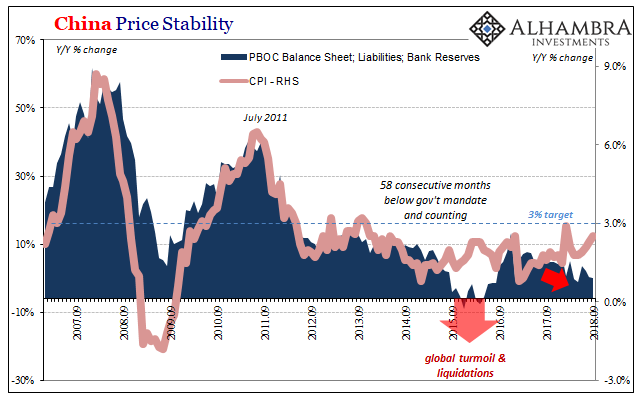

China Price Stability 2007-2018 - Click to enlarge |

| The result was, again, a somewhat curious divergence (shown above) between money and inflation. The PBOC caught in a eurodollar vise was in contraction mode while consumers faced the pig shortage as best they could. It wasn’t an easy time for anyone which is one major reason why by early 2016 Communist officials panicked into repeating textbook Economic measures they had largely sworn off not long before.

Three years later, nothing much has changed. It’s not pigs this time, however, it’s other foodstuffs (pork prices were down 2.4% year-over-year last month). The price of fresh vegetables, according to China’s National Bureau of Statistics, has risen by nearly 15% year-over-year in the country’s CPI basket, most of that over the last two months. For fruits, the increase is a little more than 10%. Those two categories alone contributed 0.52 points to the headline CPI’s 2.5% advance in September 2018. |

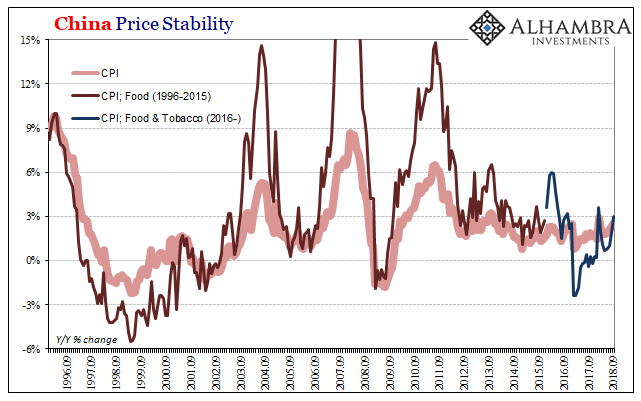

China Price Stability 1996-2018 - Click to enlarge |

| The government has continuously blamed poor weather for restricting marginal supplies, therefore forming this bottleneck adding to the margins of the CPI via foods. The press release mentioned specifically “typhoons, heavy precipitation and winds in some areas.” It seems consistent with CPI data that shows food prices rising at just a 1% annual rate in July, and then 1.9% in August followed by 3% in September.

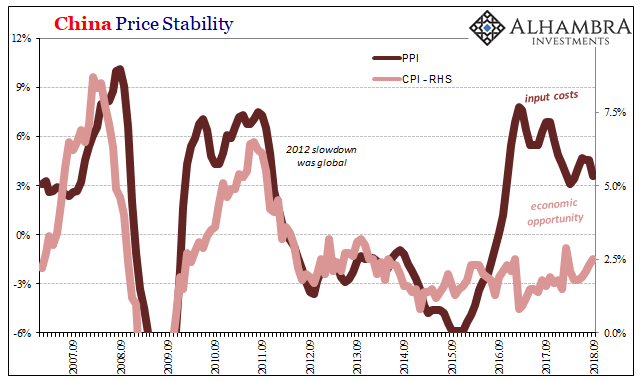

While food prices are accelerating, if only temporarily, producer prices are slowing. Both factory prices as well as China’s PPI decelerated last month. The latter was estimated to have increased by 3.6% in September, the lowest rate since April. |

China Price Stability 2007-2018 - Click to enlarge |

| The possible convergence between the CPI and PPI is again the story of China’s inability to obtain its prior economic footing. Mistaken impressions and expectations formed during that “stimulus” panic in 2016 pushed commodities in particular way ahead of actual economic circumstances on the ground. Investors were anticipating that China’s economy like the global economy would at some point catch up to them. |

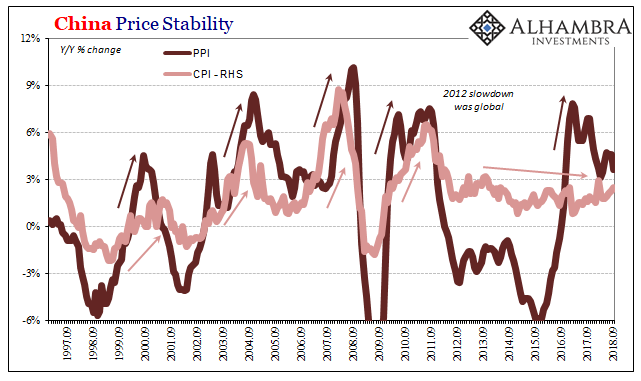

China Price Stability 1997-2018 - Click to enlarge |

| Except China’s CPI has consistently (since the 2012 slowdown, meaning 2011 eurodollar crisis) demonstrated that there isn’t much space for that to ever happen. So long as China’s internal monetary situation is constrained by its external eurodollar requirements there isn’t any way for companies to pass along input costs to inhibited Chinese consumers.

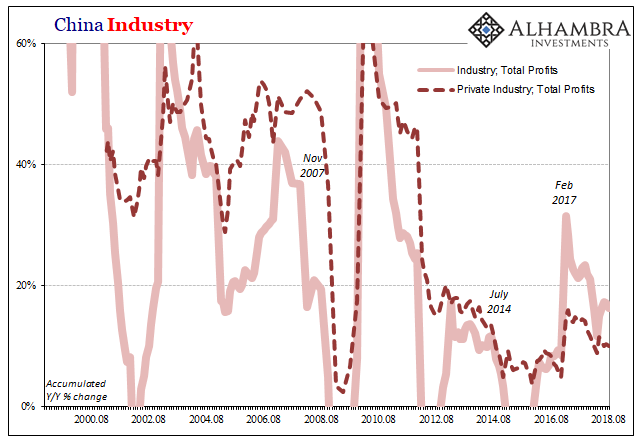

The PPI therefore is reflective of monetary misunderstanding while the CPI is the basis for convergence, including, ironically, the spike in food prices that can only further crowd out any reflexive tendencies toward equalizing the corporate bottom line with topline growth. In other words, if China’s economy had actually been performing as commodity investors have been expecting, corporate profits would’ve rebounded significantly. Instead, profits fell sharply around 2012 and like the CPI have never come back. |

China Industry 2000-2018 - Click to enlarge |

| As inflation, it is indicative again of monetary constraints. Over time, without economic growth in fact as opposed to narrative only, conjunction can be the only result – prices (PPI) before economy (imports).

In this way, China’s imbalanced condition is transmitted to the rest of the global economy (economic contagion) which if serious enough even sky-high global sentiment can no longer resist. It’s not really about pigs and typhoon plagued vegetables as it is the lack of economic opportunity under monetary restrictions. The rise of food prices, call it random bad luck, has again contributed even more pressure at the worst possible moment. Small wonder the PBOC’s replaying of RRR; what other choice is there? |

China Imports 2008-2018(see more posts on China Imports, ) - Click to enlarge |

Tags: bank reserves,China,China Imports,Consumer Prices,CPI,currencies,economy,EuroDollar,eurodollar standard,Federal Reserve/Monetary Policy,food prices,Markets,Money Supply,newsletter,PBOC,PPI,RMB