Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

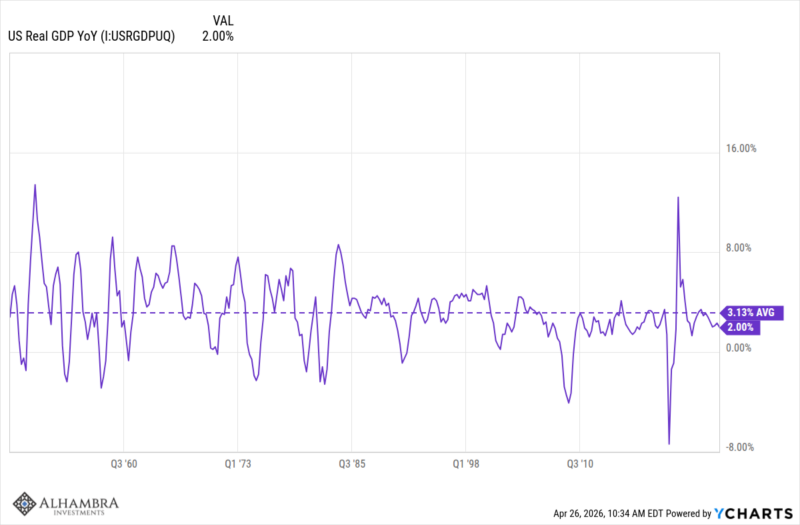

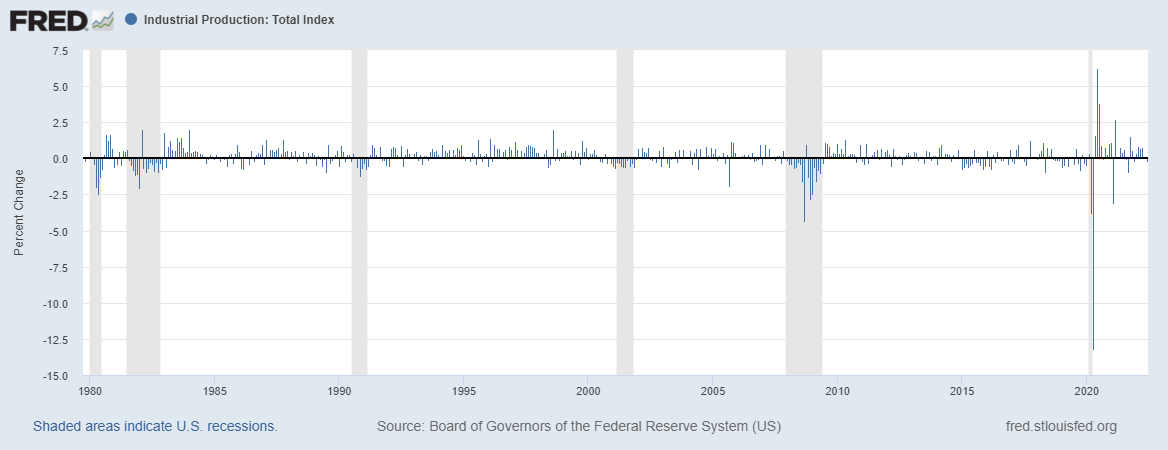

Monthly Macro Monitor: A Lot Of Noise, Little Effect

Monthly Macro Monitor: A Lot Of Noise, Little Effect27 Apr 2026

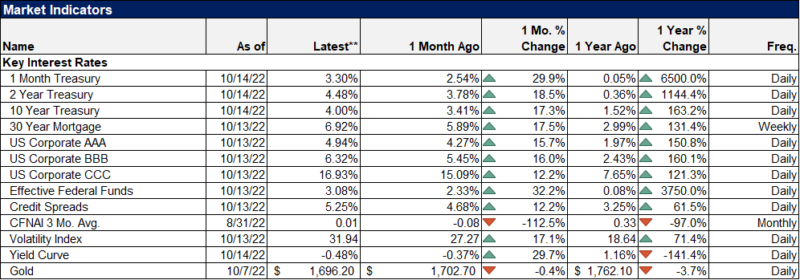

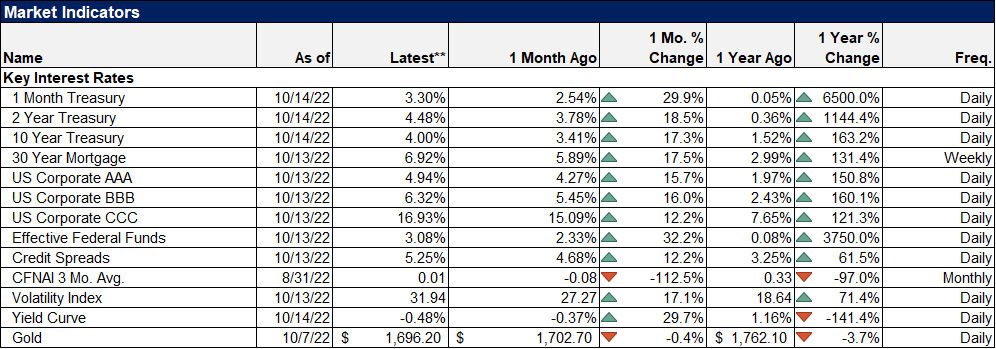

Weekly Market Pulse: Just A Little Volatility

Weekly Market Pulse: Just A Little Volatility17 Oct 2022

Weekly Market Pulse: No News Is…12 Sep 2022

Weekly Market Pulse: There Is No Certainty In Investing

Weekly Market Pulse: There Is No Certainty In Investing18 Jul 2022

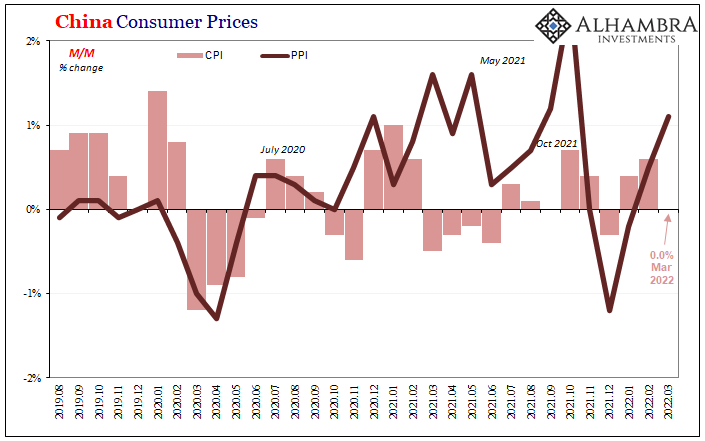

Curve Inversion 101: US CPI Politics Up Front, China PPI Down(ing) The Back16 Jun 2022

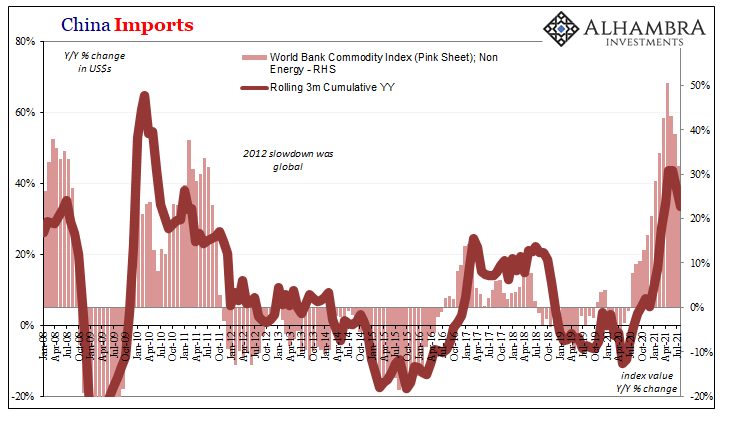

China More and More Beyond ‘Inflation’17 Apr 2022

US CPI Reaches Seven On US Goods Prices, With Disinflation Setting In Everywhere Else (incl. US Services)16 Jan 2022

What’s Real Behind Commodities8 Sep 2021

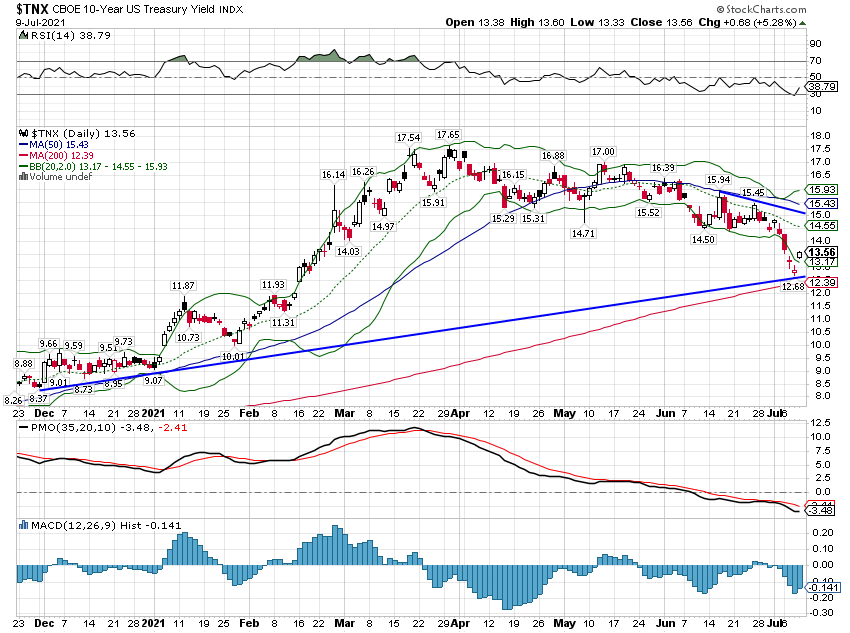

Weekly Market Pulse: As Clear As Mud19 Jul 2021

And Now Three Huge PPIs Which Still Don’t Matter One Bit In Bond Market15 Jul 2021

Weekly Market Pulse: Is It Time To Panic Yet?

Weekly Market Pulse: Is It Time To Panic Yet?12 Jul 2021

The Inflation Emotion(s)10 Jun 2021

Two Seemingly Opposite Ends Of The Inflation Debate Come Together19 Feb 2021

If the Fed’s Not In Consumer Prices, Then How About Producer Prices?16 Jan 2021

If Trade Wars Couldn’t, Might Pig Wars Change Xi’s Mind?12 Dec 2019

Consistent Trade War Inconsistency Hides The Consistent Trend5 Dec 2019

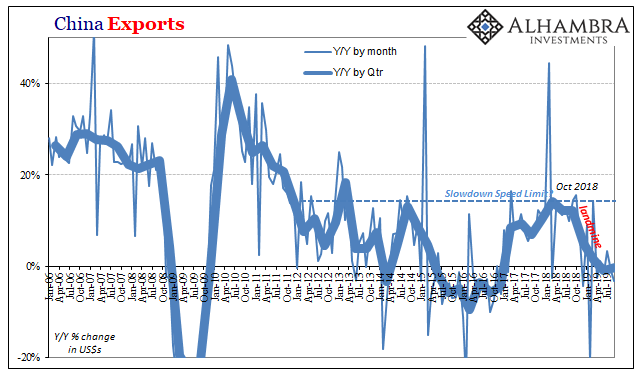

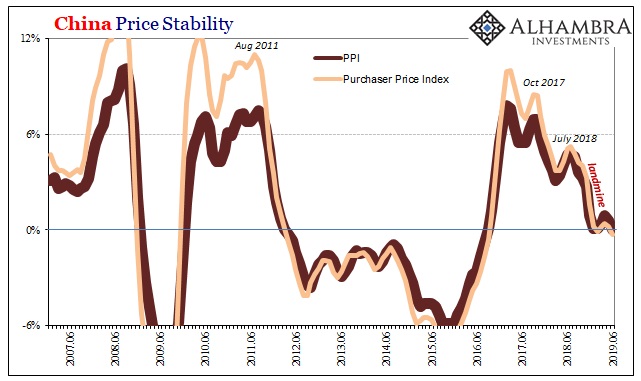

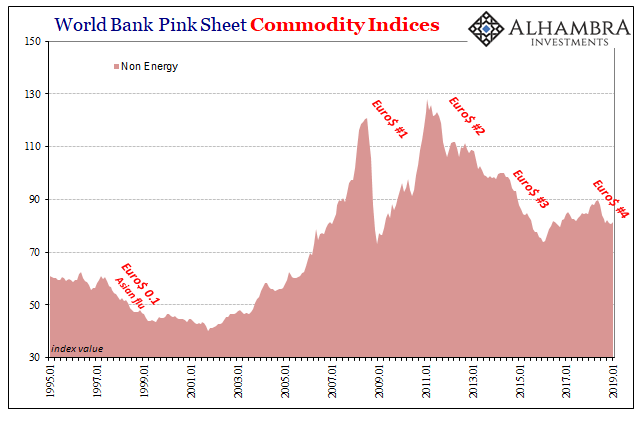

China’s Dollar Problem Puts the Sync In Globally Synchronized Downturn18 Oct 2019

As Chinese Factory Deflation Sets In, A ‘Dovish’ Powell Leans on ‘Uncertainty’14 Jul 2019

China’s Big Money Gamble19 Feb 2019

Rate of Change13 Jan 2019