Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Swiss Franc |

EUR/CHF - Euro Swiss Franc, November 28(see more posts on EUR/CHF, ) . - Click to enlarge |

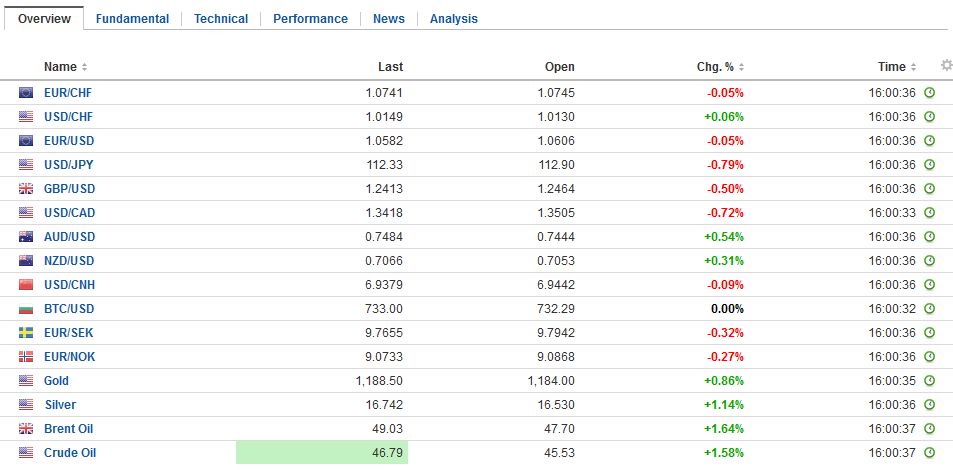

FX RatesAs soon as markets opened in Asia, the greenback was sold, and corrective forces that had been nipping below the surface took hold. The euro, which had finished last week below $1.0590, rallied nearly a cent. Before the weekend, the greenback had pushed to almost JPY114, an eight-month high, before closed near JPY113.20. It was sold to almost JPY111.35 in early Asia. Sterling extended last week’s gains and briefly poked through $1.2530, to reach its highest level since November 14. There were no fundamental developments that sparked the move. However, as we had noted, the dollar’s technical condition was stretched. The key macro considerations remain intact. Barring a surprisingly poor jobs report at the end of the week, the Federal Reserve is on track to hike rates in a few weeks, and the prospect is for fiscal stimulus next year, even if the precise details are not known. Meanwhile, the combination of European politics (Austrian election for President and Italy’s referendum this weekend) and the prospects for the ECB to extend its asset purchases program, with possible tweaks to the rules to address the scarcity of some securities (including securities lending rules) undermines weighs on the European complex. |

FX Performance, November 28 2016 Movers and Shakers . Source: Dukascopy - Click to enlarge |

| The buying enthusiasm for the euro faded, and in the European morning, the euro had given back nearly half of the day’s gains. A move below $1.0620, and especially $1.0580, may signal the end of the correction. The euro did close higher in the last two sessions. We’ve seen the widening interest rate differentials to be a key force, and note that even today, the two-year and 10-year US premium is slightly wider.The dollar began to recover against the Japanese yen in the Asian session and continued through the European morning. It was more than a yen off its lows by late-European morning turnover to approach JPY112.50, the area that offered support before the weekend. The US two-year premium is slightly wider, but the 10-year advantage is a touch smaller. Boost by utilities and financials, the Topix added 0.35% to extend its advancing streak for a 12th consecutive session. Although it recovered from earlier losses, the Nikkei was not as fortunate. Its minor loss snapped a seven-day advance. |

FX Daily Rates, November 28 (GMT 16:00) . - Click to enlarge |

|

Sterling cannot get out of its own way. It rose in four of last week’s five sessions but is giving back those gains today. From the high set in Asia to the low in the European morning, sterling shed nearly a cent and a quarter before finding support near the pre-weekend low. It has not traded below $1.24 since November 23. The dollar-bloc currencies are firmer. The Aussie’s upside correction began last week, and it gained against the greenback in four of the five sessions. It reached almost $0.7500 to meet the 38.2% retracement of the decline since the US election. Initial support is seen near $0.7460. The Canadian dollar has recouped most of the pre-weekend losses, helped perhaps by the steadying in oil prices. OPEC appears to be making a last-ditch effort to reach an agreement at Wednesday’s meeting. The same problem that has bedeviled the cartel continues to do so, namely not all OPEC members are prepared to cut output, which the Saudi Arabia has made a precondition to its cuts. Over the weekend, Saudi Arabia was playing down the need for an agreement, noting that demand is likely to absorb some of the increase next year. |

FX Performance, November 28 . - Click to enlarge |

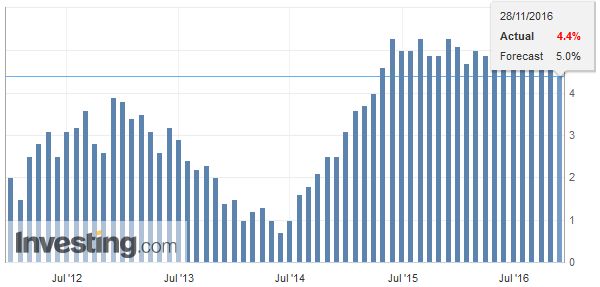

EurozoneThe main economic news today has been the ECB’s money supply and lending figures. For the record, money supply growth slumped to 4.4% from a revised 5.1% in September. It was the slowest since March 2015 and caught economist by surprise. It appears that the base effect was not fully appreciated, but more importantly, lending fared better than expected. Lastly, we note that while Italian bonds are outperforming their Spanish counterparts today, the stock market is heavy. The 1.25% loss lead the major bourses lower today. Italian bank stocks are extended their fall. The FTSE-Italia All-Shares Bank Index has been up one session since November 11. It is off 2.7% today to reach its lowest level since September 30. |

Eurozone M3 Money Supply YoY, October 2016(see more posts on Eurozone M3 Money Supply, ) . Source: Investing.com - Click to enlarge |

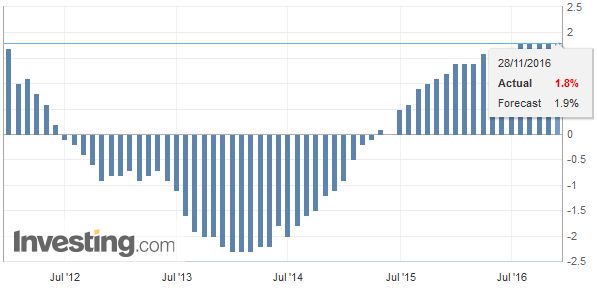

| Lending to non-financial business rose 2.1% in October. Initially, lending in September was estimated to have risen 1.9%, and was revised to 2.0%. Lending to households was steady at 1.8%. |

Eurozone Private Sector Loans YoY, October 2016(see more posts on Eurozone Private Sector Loans, ) . |

China

The Chinese yuan has been succumbing to the same forces that had dragged down other currencies against the dollar. The yuan participated in the broader dollar correction today and rose by the most in two months. The advance, less than 0.2% is the most since early September. Chinese officials point out that it is broadly steady against the basket of 13 currencies that it tracks. Even though the yuan is near eight-year lows against the dollar, it is near three-month highs against this basket.

Officials have announced that the Hong Kong-Shenzhen link will open on December 5. This will give Hong Kong-based accounts access to the small-cap market in Shenzhen. Although Shenzhen shares slipped lower today, the Hong Kong Enterprise Index which tracks mainland companies rose almost 0.9%, led by small-caps which were up nearly twice as much.

United States

The US and Canadian calendars are light to start the week. The US reports the Dallas Fed’s manufacturing index for November. The first positive reading since the end of 2014 is expected but is unlikely to have much impact.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CNY,$EUR,$JPY,EUR/CHF,Eurozone M3 Money Supply,Eurozone Private Sector Loans,FX Daily,newslettersent