Lance Roberts

My articles My offerMy siteAbout meMy videosMy books

Follow on:TwitterSeeking AlphaFacebookAmazon

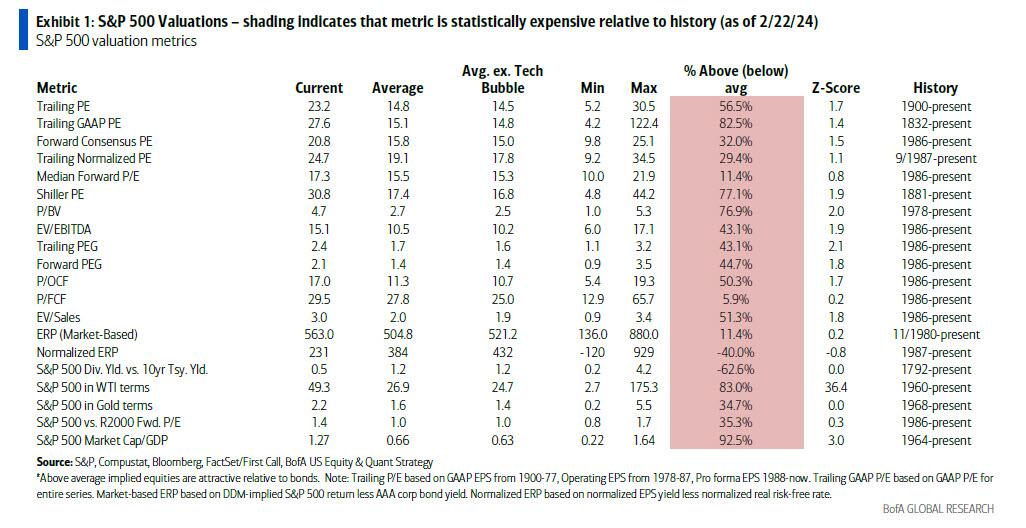

Valuation metrics have little to do with what the market will do over the next few days or months. However, they are essential to future outcomes and shouldn’t be dismissed during the surge in bullish sentiment. Just recently, Bank of America noted that the market is expensive based on 20 of the 25 valuation metrics they track. As BofA’s Chief Equity Strategist stated:

“The S&P 500 is egregiously expensive vs. history. It’s hard to be bullish based on valuation“

Since 2009, repeated monetary interventions and zero interest rate policies have led many investors to dismiss any measure of “valuation.” Therefore, investors reason the indicator is wrong since there was no immediate correlation.

The problem is that valuation models are not, and were never meant to be, “market timing indicators.” The vast majority of analysts assume that if a measure of valuation (P/E, P/S, P/B, etc.) reaches some specific level, it means that:

- The market is about to crash, and;

- Investors should be in 100% cash.

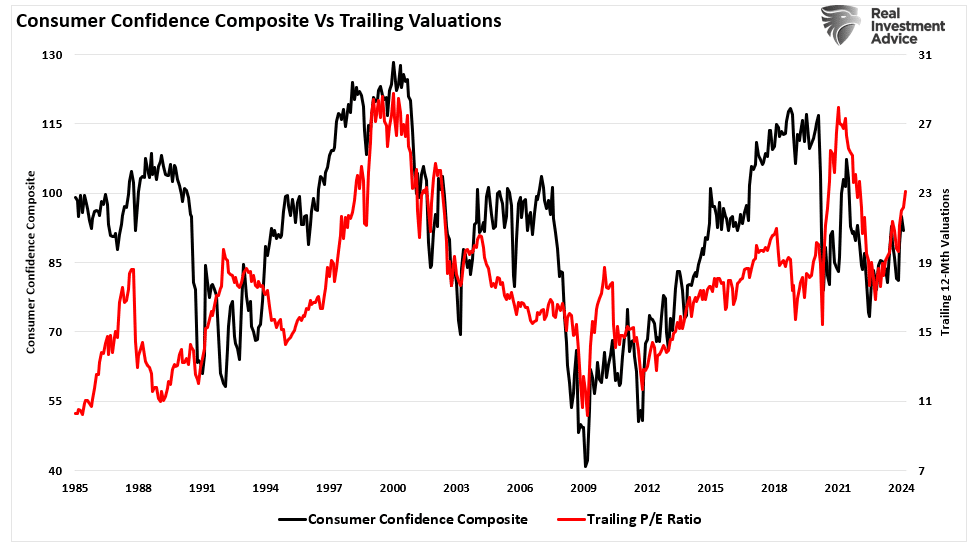

Such is incorrect. Valuation metrics are just that – a measure of current valuation. More importantly, when valuation metrics are excessive, it is a better measure of “investor psychology” and the manifestation of the “greater fool theory.” As shown, there is a high correlation between our composite consumer confidence index and trailing 1-year S&P 500 valuations.

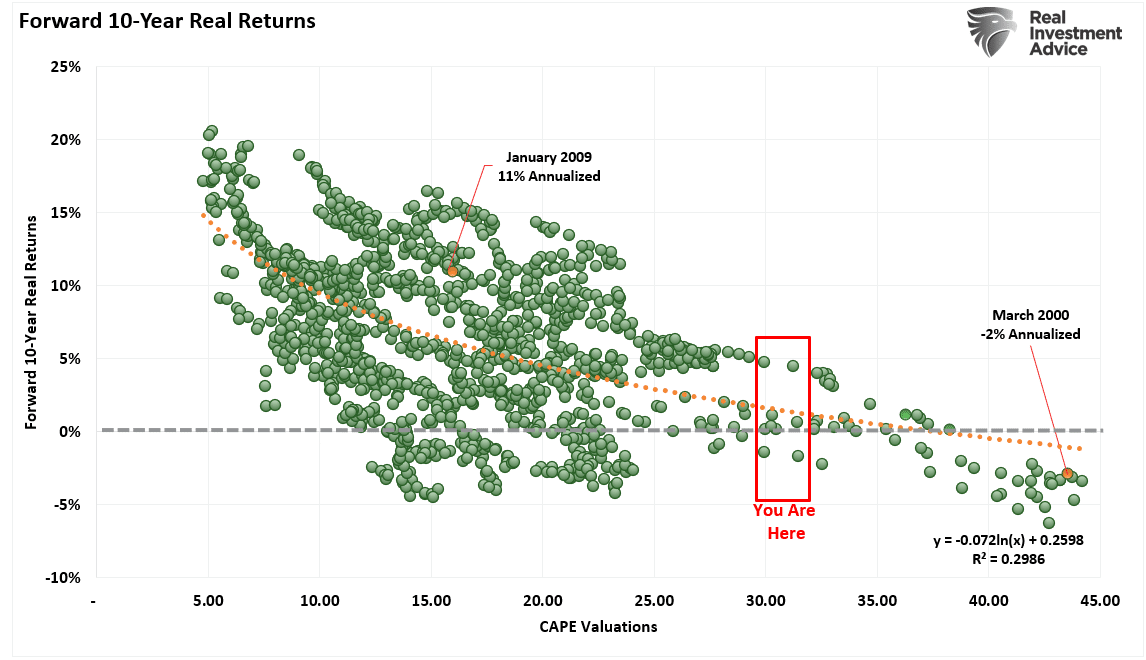

What valuations do provide is a reasonable estimate of long-term investment returns. It is logical that if you overpay for a stream of future cash flows today, your future return will be low.

I previously quoted Cliff Asness on this issue in particular:

“Ten-year forward average returns fall nearly monotonically as starting Shiller P/E’s increase. Also, as starting Shiller P/E’s go up, worst cases get worse and best cases get weaker.

If today’s Shiller P/E is 22.2, and your long-term plan calls for a 10% nominal (or with today’s inflation about 7-8% real) return on the stock market, you are basically rooting for the absolute best case in history to play out again, and rooting for something drastically above the average case from these valuations.”

We can prove that by looking at forward 10-year total returns versus various levels of PE ratios historically.

Asness continues:

“It [Shiller’s CAPE] has very limited use for market timing (certainly on its own) and there is still great variability around its predictions over even decades. But, if you don’t lower your expectations when Shiller P/E’s are high without a good reason — and in my view, the critics have not provided a good reason this time around — I think you are making a mistake.”

Which brings me to Warren Buffett.

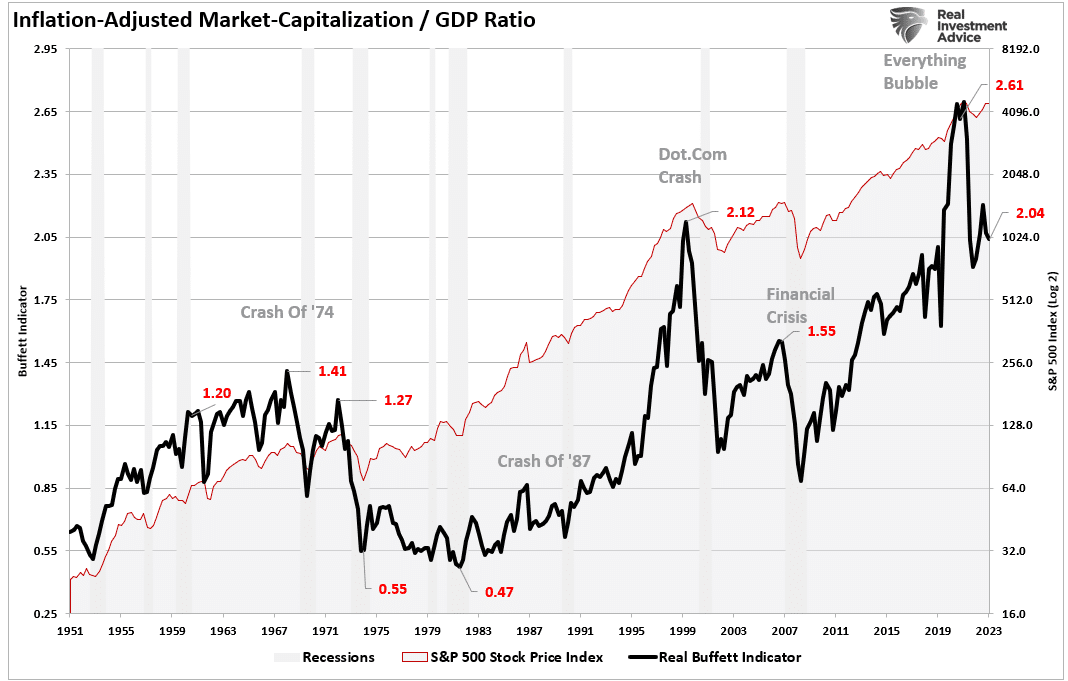

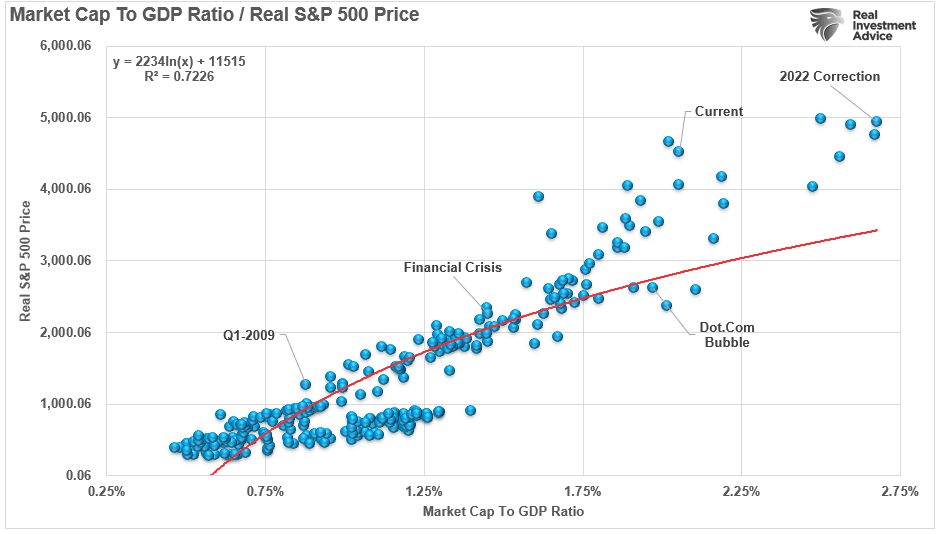

Market Cap To GDP

In our most recent newsletter, I discussed Warren Buffet’s dilemma with his $160 billion cash pile.

The problem with capital investments is that they take time to generate a profitable return that accretes to the business’s bottom line. The same goes for acquisitions. More importantly, concerning acquisitions, they must both be accretive to the company and reasonably priced. Such is Berkshire’s current dilemma.

“There remain only a handful of companies in this country capable of truly moving the needle at Berkshire, and they have been endlessly picked over by us and by others. Some we can value; some we can’t. And, if we can, they have to be attractively priced.”

This was an essential statement. Here is one of the most intelligent investors in history, suggesting that he cannot deploy Berkshire’s massive cash hoard in meaningful size due to an inability to find acquisition targets that are reasonably priced. With a $160 war chest, there are plenty of companies that Berkshire could either acquire outright, use a stock/cash offering, or acquire a controlling stake in. However, given the rampant increase in stock prices and valuations over the last decade, they are not reasonably priced.

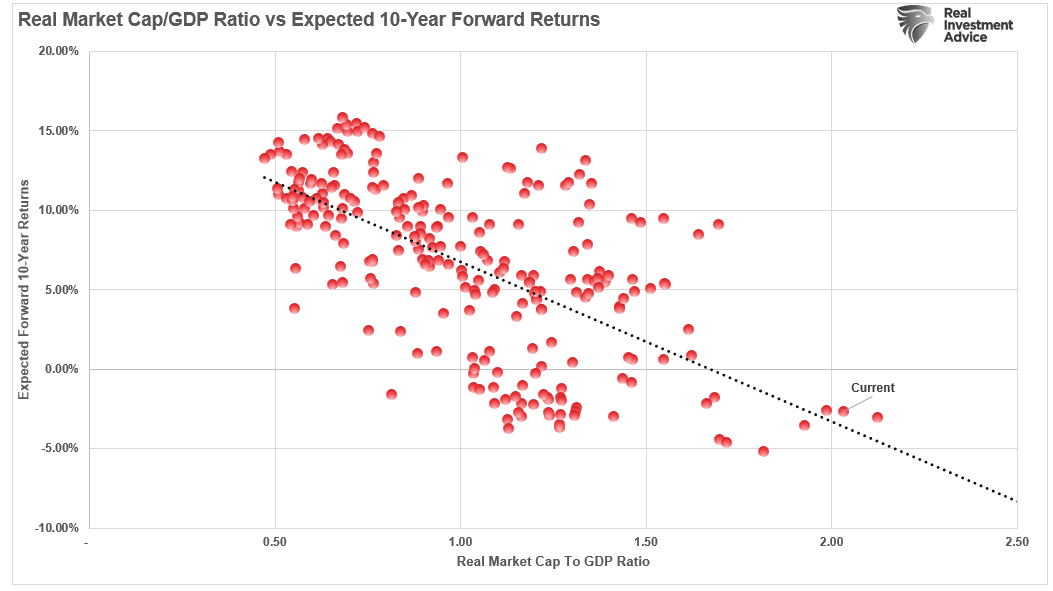

One of Warren Buffett’s favorite valuation measures is the market capitalization to GDP ratio. I have modified it slightly to use inflation-adjusted numbers. The simplicity of this measure is that stocks should not trade above the value of the economy. This is because economic activity provides revenues and earnings to businesses.

The “Buffett Indicator” confirms Mr. Asness’ point. The chart below uses the S&P 500 market capitalization versus GDP and is calculated on quarterly data.

Not surprisingly, like every other valuation measure, forward return expectations are substantially lower over the next ten years than in the past.

None of this should be surprising. Logics suggests that overpaying for any asset in the present inherently will generate lower future expected returns versus buying assets at a discount. Or, as Warren Buffett stated:

“Price is what you pay. Value is what you get.”

F.O.M.O. Trumps Fundamentals

In the “heat of the moment,” fundamentals don’t matter. In a market where momentum drives participants due to the “Fear Of Missing Out (F.O.M.O.),” fundamentals are displaced by emotional biases. Such is the nature of market cycles and one of the primary ingredients necessary to create the proper environment for an eventual reversion.

Notice, I said eventually.

As David Einhorn once stated:

“The bulls explain that traditional valuation metrics no longer apply to certain stocks. The longs are confident that everyone else who holds these stocks understands the dynamic and won’t sell either. With holders reluctant to sell, the stocks can only go up – seemingly to infinity and beyond. We have seen this before.

There was no catalyst that we know of that burst the dot-com bubble in March 2000, and we don’t have a particular catalyst in mind here. That said, the top will be the top, and it’s hard to predict when it will happen.”

Furthermore, as James Montier previously stated:

“Current arguments as to why this time is different are cloaked in the economics of secular stagnation and standard finance workhorses like the equity risk premium model. Whilst these may lend a veneer of respectability to those dangerous words, taking arguments at face value without considering the evidence seems to me, at least, to be a common link with previous bubbles.“

As BofA noted in its analysis, stocks are far from cheap. Based on Buffett’s preferred valuation model and historical data, return expectations for the next ten years are as likely to be close to zero or negative. Such was the case for ten years following the late ’90s.

Investors would do well to remember the words of the then-chairman of the SEC, Arthur Levitt. In a 1998 speech entitled “The Numbers Game,” he stated:

“While the temptations are great, and the pressures strong, illusions in numbers are only that—ephemeral, and ultimately self-destructive.”

Regardless, there is a straightforward truth.

“The stock market is NOT the economy. But the economy is a reflection of the very thing that supports higher asset prices: earnings.”

The economy is slowing down following the pandemic-related spending spree. It is also doubtful the Government can continue spending at the same clip over the next decade as it did in the last.

While current valuations are expensive, it does NOT mean the markets will crash tomorrow, next quarter, or even next year.

However, there is a more than reasonable expectation of disappointment in future market returns.

That is probably something investors need to come to grips with sooner rather than later.

The post Valuation Metrics And Volatility Suggest Investor Caution appeared first on RIA.

Full story here Are you the author?Tags: Bear Market,earnings,economy,Featured,Federal Reserve,Financial markets,Financial Planning,Interest rates,Investing,newsletter,recession,retirement income,S&P 500,stocks,valuations