Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

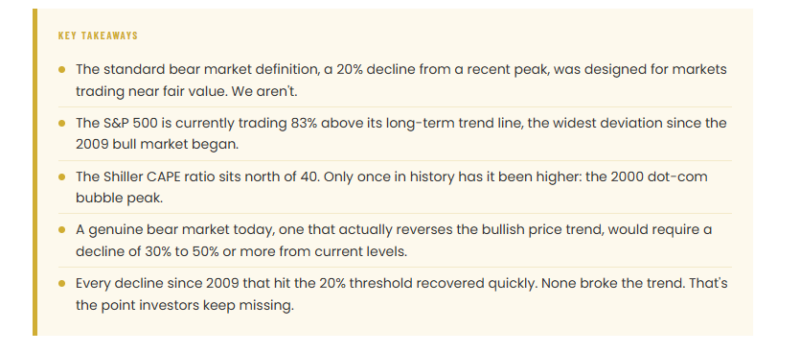

Corrections vs. Bear Markets: Why 20% Declines Are Obsolete

Corrections vs. Bear Markets: Why 20% Declines Are Obsolete25 May 2026

Buffett Cash Hoard: Why $397 Billion Sits On The Sidelines18 May 2026

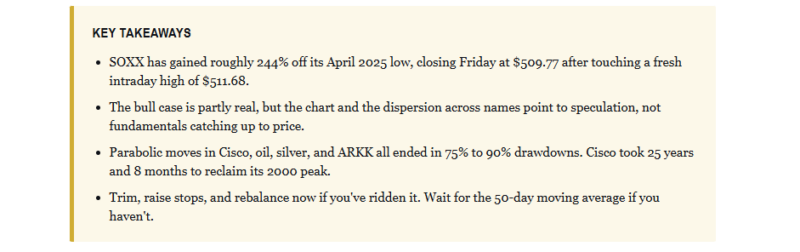

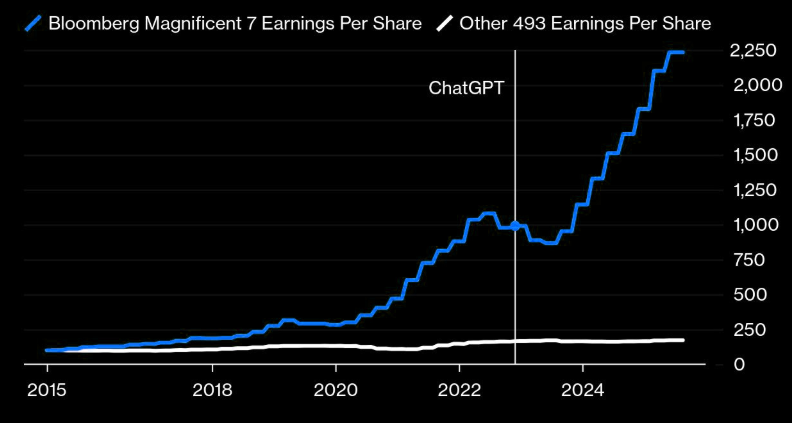

Parabolic Semiconductor Rally Is Pricing In 2028 Already

Parabolic Semiconductor Rally Is Pricing In 2028 Already11 May 2026

Market Correction Risk: Why Summer 2026 Looks Risky

Market Correction Risk: Why Summer 2026 Looks Risky4 May 2026

Hormuz: Why Markets Are Shrugging Off The Oil Shock27 Apr 2026

Market Lesson: Why Panic Is A Costly Mistake20 Apr 2026

S&P 500 Outlook: The 8.2% Rally & What Comes Next.

S&P 500 Outlook: The 8.2% Rally & What Comes Next.13 Apr 2026

The Stock Market Rally: Buy Or Fade It?

The Stock Market Rally: Buy Or Fade It?6 Apr 2026

Stock Market Breadth: Warning Or Opportunity?30 Mar 2026

The 200-DMA Just Broke: What Every Investor Should Know23 Mar 2026

Treasury Bond Yields Don’t Lie: But Wars Don’t Drive Them

Treasury Bond Yields Don’t Lie: But Wars Don’t Drive Them16 Mar 2026

9 Mar 2026

SaaS: Is There Opportunity In The Destruction?

SaaS: Is There Opportunity In The Destruction?2 Mar 2026

Is China Really Dumping US Treasuries?

Is China Really Dumping US Treasuries?23 Feb 2026

Market Sector Review: Extreme Market Bifurcation

Market Sector Review: Extreme Market Bifurcation16 Feb 2026

Speculative Narrative Unwinds

Speculative Narrative Unwinds9 Feb 2026

The Market Cycles Potentially Driving 2026 Returns

The Market Cycles Potentially Driving 2026 Returns2 Feb 2026

The South Park Market Of 2026

The South Park Market Of 202623 Jan 2026

2026 Earnings Outlook: Another Year Of Optimism12 Jan 2026

New Year’s Resolutions For 2026 – Investor Version

New Year’s Resolutions For 2026 – Investor Version9 Jan 2026