Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss FrancThe Euro has fallen by 0.05% to 1.0941 |

EUR/CHF and USD/CHF, June 25(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: New record highs in the S&P 500 and NASDAQ yesterday helped lift most Asia Pacific markets today. China and Hong Kong led the regional gains and were sufficient to lift the MSCI regional benchmark to halt a two-week drop. European equities are little changed but will rise for the fifth week in the past six, barring a sharp sell-off ahead of the weekend. US indices’ futures are firm. The bond market is quiet. The US 10-year benchmark is hovering around 1.48%, little changed on the week. European yields are firmer on the day but are also flattish on the week. After last week’s exaggerated rally, the dollar drifted mostly lower this week. The yen is the notable exception, with the Scandis and dollar-bloc leading the move. On the day, the greenback is softer, with sterling the only major to be underwater. Emerging market currencies are also mostly firmer against the dollar, and the JP Morgan EM FX Index is up for the fifth consecutive session. It is the first week since February that it has risen every session of the week. The Mexican peso is firm after being propelled higher yesterday by the surprise rate hike by the central bank. Russia announced export tariffs on several industrial metals (steel products, nickel, aluminum, and copper) estimated to be around $2.3 bln for the fourth quarter. Many industrial metals traded higher today, including copper, which is paring yesterday’s loss, the only decline this week. August WTI is little changed in a narrow range around $73.00. Crude oil prices are up about 3% this week and have only fallen one week in the past two months. Gold is firm near $1783 after peaking in the middle of the week near $1795. |

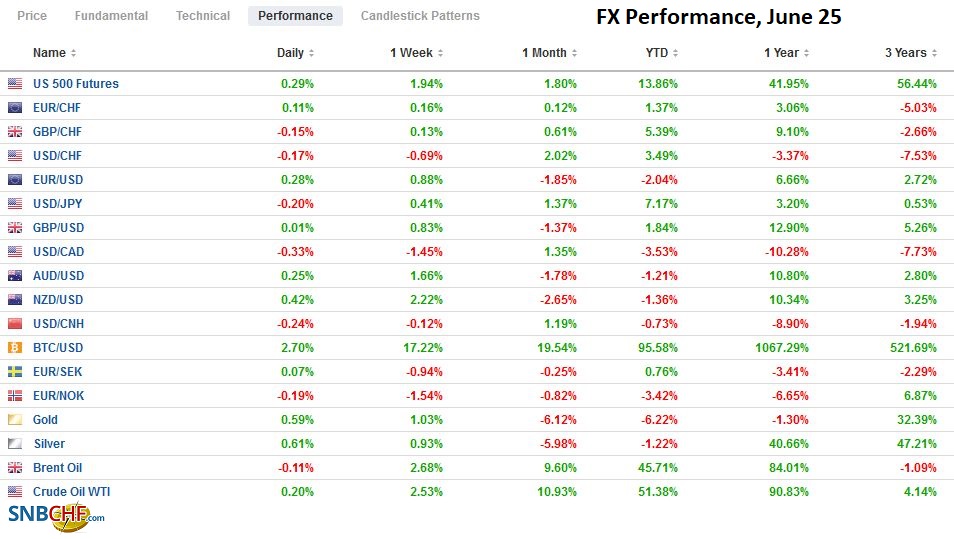

FX Performance, June 25 - Click to enlarge |

Asia Pacific

Tokyo reports consumer prices before Japan as a whole. Tokyo CPI defied expectations and did not show another month of deflation. All three measures, headline, core, which excludes fresh food, and another measure that excludes fresh food and energy, rose to zero from deflation. It is the first time the headline rate was not negative since last September. The core rate has been negative since last July. Japan’s economy appears close to bottoming out. Next week’s Tankan survey is likely to reflect this, with all major sectors likely improving, including capex plans.

Despite the increase in the required reserve for foreign currency deposits, Chinese banks are awash with dollars. Reports suggest their holdings have surpassed $1 trillion. While some observers may claim this is a reflection of stealth intervention, there also is a less nefarious explanation. Chinese banks acquire dollars from Chinese exporters. Most Chinese trade is conducting in US dollars. This is one of the implications of the low usage of the yuan on SWIFT. Also, the portfolio inflows leave banks with foreign currencies, often dollars. Separately, the decline in US oil inventories has been cited as a supportive factor for crude. Today, reports suggest China’s oil inventories are at their lowest levels since February. OPEC+ meets next week, and an increase in output seems likely. Lastly, next week China reports the June PMI. It is expected to have softened a little amid more speculation that the world’s second-largest economy may be near a peak.

The dollar appears to be trapped between two expiring sets of options. The first for $1.55 bln at JPY111.00. Today’s session is the first in three so far that the greenback has not traded above JPY111.00. On the other hand, there is an option for about $835 mln at JPY110.50. It has not traded below JPY110.60 since Tuesday.

Despite new social restrictions in Sydney, the Australian dollar is trading at its best level of the week to trade above $0.7600. The next target is near $0.7625 and then $0.7660. The $0.7570-$0.7580 area may now offer support. New Zealand posted its first 12-month trade deficit in 11 months, but the New Zealand dollar is also reached new highs for the week, slightly above $0.7080. As it recovers, the next target is near $0.7120.

We suspected that the yuan’s pullback, encouraged by the PBOC, had largely run its course, and today the yuan strengthened by more than 0.25%, the most this month. It is the third consecutive advance. The PBOC set the dollar’s reference rate at CNY6.4744 compared with the median projection bank models in Bloomberg’s survey for CNY6.4740. Note that S&P affirmed China’s A+/A- ratings with a stable outlook.

Europe

When Germany and France are united, they typically carry the issue at European Union. However, their gambit to have a rapprochement with Russia met stiff resistance and ultimately was dropped from the final communique. Since Russia annexed Crimea in 2014, the EU has not invited Putin to attend summits. Some saw it as Merkel’s swan song, her last summit, but her overture was rejected. Eastern European countries were deadset against it. Still, Merkel and Macron’s position is understandable. The “America is Back” is predicated on the confrontation with China. US interests lie with the Pacific. Europe cannot be sure that the US will not elect another president who is not committed to unilateralism. It needs to forge its own modus vivendi with Russia.

The Bank of England did not surprise yesterday, keeping policy steady. It did underscore the importance of two events in the coming months. First, the central bank does not meet in July, and when it meets in August, new economic forecasts will be provided. Second, the income-support furlough program ends in September, and how the labor market fares is a key consideration. Still, the BOE sees the economy accelerating to 5.5% growth this quarter, well above the 4.3% pace anticipated in May, with stronger price pressures. The BOE, like the Fed and the ECB, see the price pressures as transitory. For the record, the market appears to be pricing in a doubling of the 10 bp base rate by the end of H1 22.

The euro traded between roughly $1.1910 and $1.1970 in the middle of the week. It has not been out of the range since. Lower highs and higher lows have been recorded yesterday and so far today. A move above $1.20, which houses the 200-day moving average and the (50%) retracement of the slide since the middle of the month’s high near $1.2150, is needed to lift the tone.

Sterling stalled in the middle of the week near $1.40. The halfway point of this month’s range is a little higher, near $1.4020. 21. Support is seen in the $1.3870-$1.3895 area. The euro has been trending lower against sterling since the end of April. The downtrend line is near GBP0.8620 today. It may be too far today (from the current ~GBP0.8580 area), but it looks set to be tested next week.

America

Three notable events took place in the US yesterday. First, a bipartisan infrastructure initiative appears to have been struck. The nearly $580 bln package will proceed with a second bill that focuses on the “human infrastructure” that the Democrats intend to pass under the reconciliation process. The funding of it is a bit murky. It includes sales from the US strategic oil reserves (intended for emergencies but used as a piggybank before), stepped up IRS collections, unspecified public-private partnerships, and an anticipated boost to growth. Second, the Biden administration extended by a month, to the end of July, the moratorium on evictions. There is an estimated $47 bln emergency rent assistance that still needs to be distributed. It is expected to be the last extension. Third, large US banks passed the Fed’s latest stress test, and this will lead to increased dividend and share buyback programs that will likely be announced next week. Some estimates suggest shareholders may get $140 bln from the largest half dozen banks.

Banxico surprised the world yesterday by delivering a 25 rate hike.It was decided by a 3-2 vote shortly after the bi-weekly report showed CPI poking above 6% (and the unemployment rate slipping below 4%). The central bank now projects that inflation will peak in Q3 22, a quarter later than it previously anticipated. Diaz’s term as governor of Banxico’s term ends at the end of the year, and President AMLO has already nominated his success, Herrera, the outgoing finance minister. Still, the market does not expect “one and done.” The market appears to be discounting another hike at the next meeting on August 12.

The US reports May’s personal income and spending. Income is expected to continue to fall as a function of the winding down of cash assistance. Spending is expected to remain steady at elevated levels. April’s 0.5% increase may be matched or nearly so in May. The headline and core deflators are expected to have ticked up to 3.9% and 3.4%, respectively. The final June consumer confidence report from the University of Michigan contains the long-term inflation expectation. After a spike to 3% in May, the preliminary estimate was for it to back off to 2.8%. It stood at 2.2% at the end of 2019 and 2.5% at the end of last year. Canada and Mexico have light economic calendars today. Brazil reports its IPCA inflation measure. The year-over-year pace is still accelerating, and it is expected to push above 8%. Brazil’s central bank does not meet until August 4, but another (fourth) 75 bp hike in the Selic rate has been tipped.

The US dollar finished last week near CAD1.2465. It fell to around CAD1.2250 in the middle of the week and has been consolidating since. It reached CAD1.2340 yesterday but is holding below it today. Support is seen in the CAD1.2280-CAD1.2300 band today.

The greenback was offered before Banxico’s surprise hike yesterday and fell further on the announcement. The greenback’s 1.7% loss was the largest since last September. Yesterday’s low was near MXN19.7170. That can be challenged today, and a test on the five-month lows set earlier this month, a touch below MXN19.60, can be seen in the coming days.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Bank of England,Banxico,China,Currency Movement,EU,EUR/CHF,Featured,Japan,newsletter,USD/CHF