Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss FrancThe Euro has fallen by 0.02% to 1.104 |

EUR/CHF and USD/CHF, April 28(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: It appears that the backing up of US yields is giving the dollar a better tone and challenging the Eurosystem, which has stepped up its bond purchases. The US 10-year yield is around 1.65%, roughly a two-week high and back above the 20-day moving average. European yields are mostly 2-4 bp higher, but benchmark UK yield is up six basis points about 0.84%, which, if sustained, would be the highest close this month. For its part, the greenback is firm against all the majors, but to be sure, the gains are modest. After falling each day last week against the yen, it is posting gains for the third consecutive session. The dollar traded above JPY109 for the first time since April 14. The euro made a marginal new low for the week near $1.2055 but has steadied in the European morning. Soft inflation data weighed on the Australian dollar, but the other dollar-bloc currencies and Scandis are sporting only minor losses. Emerging market currencies are mixed, though of note the Indian rupee is recovering, and its equity markets advanced the most in the Asia Pacific region today. The JP Morgan Emerging Market Currency Index is little changed. The rising yield has sapped gold prices. After rejecting the $1800-level last week, the yellow metal was sold to almost $1766 today, a seven-day low. OPEC+ decision to go forward with returning some output it has cut next month, despite emergencies in Japan, the lockdown in India, and restrictions in parts of Europe, coupled with the build that API reported (which would be the largest in several weeks), leaves June WTI in roughly a 30-cent range on either side of $63. |

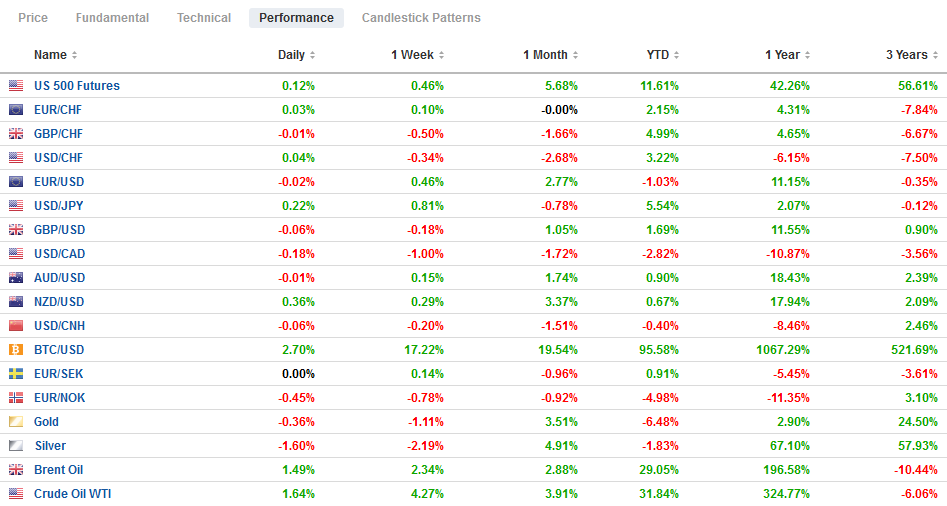

FX Performance, April 28 - Click to enlarge |

Asia Pacific

Japan retail sales rose 1.2% in March. That was twice the median forecast in the Bloomberg survey. Despite a reduction in hours, shops were open, consumers appeared resilient. In turn, that may encourage economists to shave forecasts that saw the economy contracting by 3.9% in Q1. Still, the real challenge is here in Q2. The third formal emergency for several large population centers began this past weekend and runs through May 11. However, recall that the first two emergency declarations were initially extended.

Australia’s Q1 inflation undershot expectations. The quarter-over-quarter increase of 0.6% missed the 0.9% median forecast, which anticipated a steady pace from Q4 20. The underlying measures were softer, and the trimmed mean rose 0.3% for a record low 1.1% year-over-year. If it weren’t for energy and administrative prices, inflation would have been even weaker. However, we are reluctant to read too much into today’s report for implications for monetary policy. Recall that in Q2 20, Australia’s CPI fell by 1.9%. This will drop out of the year-over-year calculations (base effect). The beginning of the exit for QE and yield curve control remains possible in Q4.

The dollar briefly dipped below JPY107.50 at the end of last week and today poked above JPY109.00 for the first time in a little more than two weeks. The correlation with US Treasury yields is about as tight as it gets. The halfway point of this month’s range comes in a bit higher, near JPY109.20. Note that there is a $1.2 bln option struck at JPY109 that expires tomorrow. Initial support is seen around JPY108.80. Despite some intraday probes, the Australian dollar has not closed above $0.7800 since early March and was again rebuffed earlier this week. Today’s low (~$0.7725) was set in the local market, but it has languished since and has been unable to recover above $0.7750. Last week’s low was a little below $0.7700, where an option for about A$515 expires today. The US dollar traded in a narrow range inside yesterday’s range, which itself was inside Monday’s range. The greenback slipped on Monday and Tuesday by a slight 0.2% and is virtually flat today near CNY6.4830.

Europe

European markets are quiet, and although the focus is on US developments later today, several ECB officials speak, including President Lagarde and board members Schnabel, Centeno, and Rehn. But the message is clear: essentially, there is no new message until June, when the ECB meets again and will review its policies, including the stepped-up bond purchases. The ECB’s balance sheet expanded by almost 36 bln euros, the most in a month. Remember, its balance sheet expansion is through loans and bond-buying. The Federal Reserve’s balance sheet, growth, in contrast, is a function of bond buying. The ECB’s balance sheet is now a little over 70% of GDP, almost twice the proportionate size of the Fed’s.

Apple reports its earnings today, but the EU appears poised to take up anti-trust action against it. Although other investigations are reportedly being conducted, Sweden’s Spotify claims about access to Apple’s app store and other disadvantages appear to be the focus. Separately, Australia’s regulators have given Apple and Google a year to open their app stores to competition or face legislative action.

For the second session, the euro encountered selling pressure near $1.2095, and it made a marginal new low for the week, 1/100 of a cent below yesterday’s low, according to Bloomberg, just above $1.2055. There is a large option for 2.56 bln euros struck at $1.20 that expires today, and given the subdued volatility, it looks safe. That said, the euro’s this month’s uptrend has lost some momentum, and there seems to be little chart support ahead of the $1.20 area. Sterling also appears to be going nowhere quickly. It remains within the range established Monday and Tuesday (~$1.3860-$1.3930). The cross is also flattish near GBP0.8690. We favor the downside, but the euro has been resilient.

America

Today’s US story is about nuances and the big picture. The FOMC meeting is about nuances. Policy is not going to change. The key may come down to a couple of words here or there. Previously Fed officials have intimated that it would be “some time” before “substantial further progress” toward the targets is met, though the word does not appear in the FOMC statement. The statement itself in March was nearly identical to the January statement. The changes were in the second paragraph that summarizes the recent economic data. However, as Fed Chair Powell recognized, the US economy is at an inflection point. The median forecast of the early forecasts in the Bloomberg survey sees next week’s nonfarm payrolls rising by 900k (916k in March) and the private sector employment rising more than 10% faster than the 780k gain in March. The unemployment rate is expected to fall below its 10- and 20-year average (6.0% and 6.1%, respectively).

Various measures of inflation are rising. It is, of course, difficult to separate noise from the signal. There is little doubt that some of the measured inflation is indeed temporary, like the base effect. That is not a question of opinion. Some supply bottlenecks, like semiconductor chips, may take several months to work out. It is a bit of an echo chamber too. A corporate earnings call means inflation, and then the journalists and analysts write about it, and then the alt-data folks chime and tell us the word count of inflation has increased. People in high-income countries spend more money on services than goods, and services are not so impacted by commodity prices. Even many goods prices are not really driven by the cost of the raw materials, like the computer you are using or your cell phone. After recognizing the increased importance of intangible capital, it seems improper to ignore it and talk about how the record high copper price, for example, is inflationary. Nevertheless, with the macro backdrop, it will be increasingly difficult to claim that there has not been significant progress toward the maximum employment and price stability targets. A small, nuance change now will be understood to lay the groundwork to begin tapering, not raising rates later this year.

Shortly after Asia Pacific markets open tomorrow, on the eve of his 100th day in office, President Biden will, for the first time, address the House and the Senate. This is about the big picture. He is expected to formally present the second half of his agenda. The Americans Family Plan complements the American Jobs Act (infrastructure-plus bill), and they both follow the $1.9 trillion American Rescue Plan. Biden’s plan will include several tax increases. There is much consternation about the partisanship in American politics at a high level, but the most immediate threat to Biden’s plan is not the GOP. It is moderate Democrats in the Senate, and given the parity of the Senate, every key decision must have each aboard if the GOP discipline is maintained in the face of apparently widespread public support for the initiatives. These initiatives will form the battle lines for next year’s midterm elections. It is already evident the rhetoric.

Ahead of the FOMC meeting outcome and Biden’s address, the US reports the advanced goods trade balance and some inventory data. They will be the last data points for economists to make last-minute revisions to the Q1 GDP forecasts ahead of tomorrow’s report. While some observers still attribute the US trade surplus to the policies of surplus countries, the US monetary and fiscal stimulus that is boosting growth is also the key driver behind the recent deterioration of the trade balance. Expect another record shortfall. Canada reports February retail sales today, and a strong gain is expected after a drop in January. The data, however, is dated after last week’s central bank meeting that tapered the bond purchases and brought forward into H2 22, when the economic slack will be absorbed. Mexico has a light economic agenda today and tomorrow and reports Q1 GDP on Friday. Many are looking for a small contraction, especially after yesterday’s unexpected large trade deficit. Lastly, note that yesterday’s inflation report from Brazil that put the year-over-year rate at 6.17% (from 5.52% in March) solidifies expectations for another 75 bp hike in the Selic rate next week.

The US dollar is in a narrow range against the Canadian dollar so far today, confined to mostly a 20-tick range above CAD1.2400. It traded in a narrow range yesterday, as well. The greenback is finding support ahead of the multiyear low set last month near CAD1.2365. Initial resistance is seen near CAD1.2435. Rising US yields appear to be eclipsing demand for the Mexican peso. The dollar rose above MXN20.00 for the first time in two weeks yesterday and remains above there so far today. It bottomed on April 20 around MXN19.7850 and retested it at the start of this week, and reached MXN20.0855 today. A band of resistance begins near MXN20.20.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Apple,Australia,Currency Movemeent,ECB,Featured,federal-reserve,newsletter