Jeffrey P. Snider

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

|

After a record three straight months of decline for the seasonally-adjusted core CPI March through May 2020, it turned upward again in June. Buoyed by a partially reopened economy, the price discounting (prerequisite to the Big D) took at least one month off. No thanks to Jay Powell, of course, who sits on the sidelines while consumer prices (like the dollar) are temporarily suspended in this wait-and-see interim. |

CPI less Food & Energy, 1964-2020 - Click to enlarge |

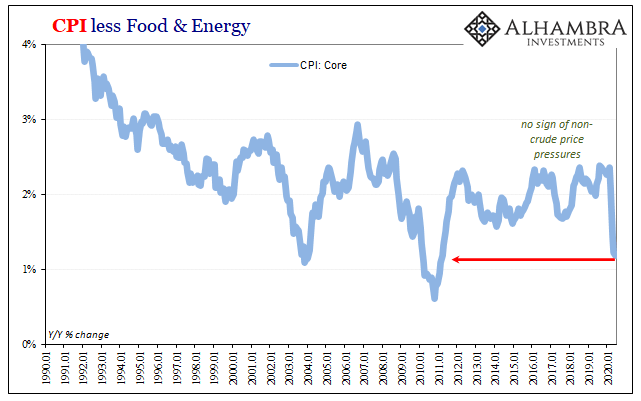

| While the losing streak has been broken, the lack of immediate downside, however, does not necessarily mean any upside. Year-over-year, the core CPI expanded at the lowest annual rate since near the depths of the Great “Recession.” At +1.19% in June, that was actually three tenths of a percent worse than May. Rarely has this key rate increased so slowly (disinflation bordering on the more serious). |

CPI less Food & Energy, 1990-2020 - Click to enlarge |

| In fact, in the series’ history it has only happened 17 times since 1963 – and a dozen of those were in 2010 in the labor market aftermath of the first global financial crisis; and another three more at the bottom of the jobless recovery following the 2001 dot-com recession.

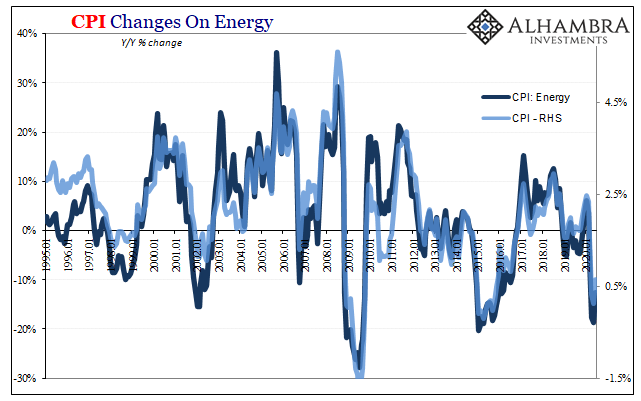

The headline CPI rate increased by just 0.65% year-over-year (unadjusted), turned away from a negative number (headline in May was just +0.12%) saved just in the nick of time by the global oil market’s very deep production cuts. |

CPI Changes on Energy, 1995-2020 - Click to enlarge |

| Despite a record (seasonally-adjusted) monthly increase in motor fuel prices, there is scant sign of inflation anywhere else (not there was much before COVID-19). Even figuring some kind of lag, if the Fed had been going nuts printing money as has been alleged, some sign of it would’ve been visible by now in consumer prices. |

CPI Changes on Energy, 1995-2020 - Click to enlarge |

| Of course, the Fed doesn’t print money and the alarmingly (if you’re Jay Powell) low levels of inflation throughout the CPI indices are nothing more than confirmation of what the bond market has been saying all along. Closer to crisis than anything like the massive monetary build up being built up (purposefully) in the public’s imagination. |

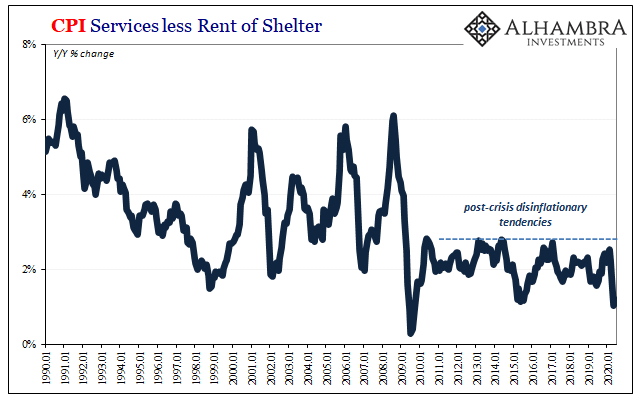

CPI Services less Rent of Shelter, 1990-2020 - Click to enlarge |

| The services rate (less rent), another key “core” inflation measure, increased by just 1.20% year-over-year in June. Outside of the prior month, May, it had been that low only three times (early 2015) since 2009.

Likewise, the “flexible” price CPI (goods in the basket whose prices are changed most quickly and often) was negative last month for the fourth straight. That suggests where prices are most likely to reflect immediate conditions there was still serious discounting taking place during the month of June – more than a full month into reopening. |

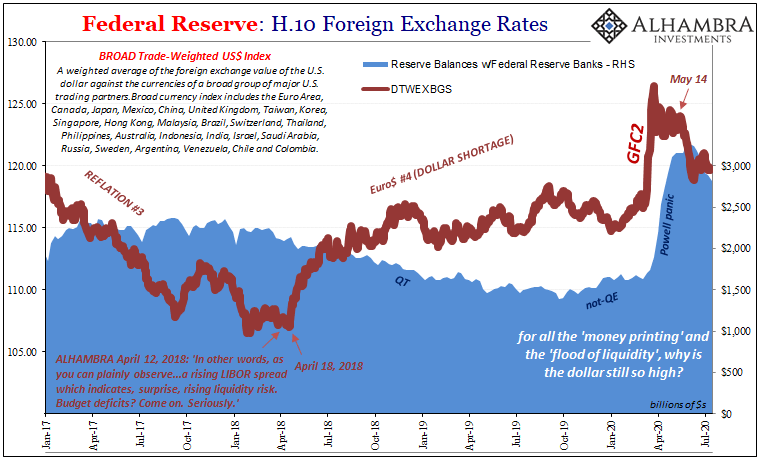

Federal Reserve: H.10 Foreign Exchange Rates, 2017-2020 - Click to enlarge |

| The CPI, like the dollar, indicates that Powell was saved by reopening rather than the common narrative of the Fed saving the world until reopening.

There’s an enormous difference between the two; the latter proposing successful policies that would, if needed again, keep everything from coming apart should risks materialize once more in the near future. The former is almost pure luck where the FOMC is concerned, policymakers mere bystanders thus leaving everyone exposed to the full weight of reversal should it come about over the coming months maybe even weeks. In fact, these inflation figures (again, like the dollar) lean more toward temporary reprieve rather than recovery or even rebound in the economy. |

. |

What the trend in consumer prices suggests is businesses still struggling with very serious imbalances (inventory, demand). While food and energy prices jump, the rest of the economy remains stuck precariously close to the edge of outright deflation.

Reopening looks very different in that category; rather than the beginning of recovery, it’s instead a transitory state between full shutdown and economic plus non-economic damage leading toward the next phase where non-economic factors dissipate leaving purely economic damage behind.

The CPI equivalent of the dead-cat bounce, perhaps, or just the payroll numbers.

Where the public narrative is concerned, the CPI really should’ve been more like stock prices and so much less like the dollar had the Federal Reserve printed any significant quantity of effective money, let alone the most ever in its troubled history. But, as the dollar, bonds, curves, etc., all show, the Fed doesn’t actually do anything like that.

The good news, so far as we may be able to classify it this way, is that Jay Powell is going to have some explaining to do over the coming months. You can’t claim to have flooded the world with dollars, as he said on 60 Minutes (lied his ass off to buy time), and then…

Where’s the inflation, Jay? It will definitely help at least some people to differentiate the myth and puppet show from what’s really going on. Money-less monetary policies are, in a word, deceitful.

Then again, ever since 2009 and QE1, there’s one thing Federal Reserve officials have gotten really good at, and it is coming up with explanations for undershooting their own inflation target (even for five years in a single stretch). Over here in reality, they better do more than hope deflation this time really will end up being “transitory.”

Full story here Are you the author?

Tags: Bonds,Consumer Prices,Core CPI,CPI,currencies,economy,Featured,Federal Reserve/Monetary Policy,inflation,inflation expectations,jay powell,Markets,money printing,newsletter