Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Weekly Market Pulse: On The Road Again

Weekly Market Pulse: On The Road Again12 May 2025

Weekly Market Pulse: Tune Out The Noise

Weekly Market Pulse: Tune Out The Noise24 Feb 2025

Weekly Market Pulse: Are Higher Interest Rates Good For The Economy?

Weekly Market Pulse: Are Higher Interest Rates Good For The Economy?15 Apr 2024

US Treasury Yields Come Back Softer After Moody’s Cut Outlook, and the Dollar Rises to New Highs Against the Yen13 Nov 2023

The Dollar Posts Corrective Upticks, while the Market Digests China’s Initiatives14 Nov 2022

Weekly Market Pulse: Just A Little Volatility

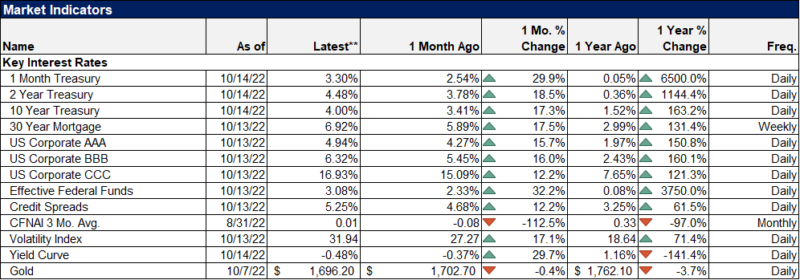

Weekly Market Pulse: Just A Little Volatility17 Oct 2022

Weekly Market Pulse: No News Is…12 Sep 2022

US Dollar Offered but Stretched Intraday9 Aug 2022

Weekly Market Pulse: Things That Need To Happen5 Jul 2022

Weekly Market Pulse: TANSTAAFL

Weekly Market Pulse: TANSTAAFL16 May 2022

You Know What They Say About The Light At The End Of The Tunnel14 Apr 2022

Media Attention All Over FOMC, Market Attention Totally Elsewhere19 Mar 2022

One Shock Case For ‘Irrational Exuberance’ Reaching A Quarter-Century22 Dec 2021

Weekly Market Pulse: Growth Scare?

Weekly Market Pulse: Growth Scare?1 Nov 2021

Weekly Market Pulse: Inflation Scare!

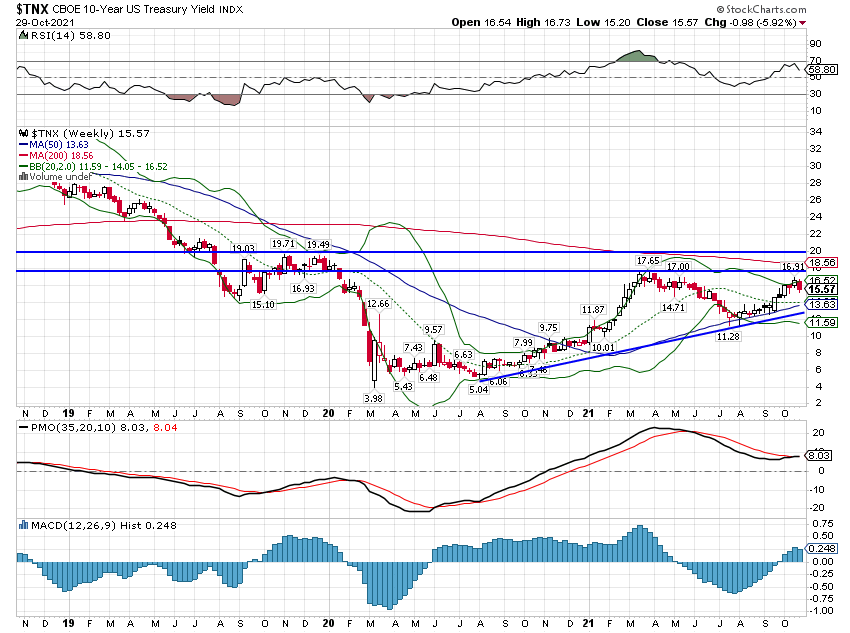

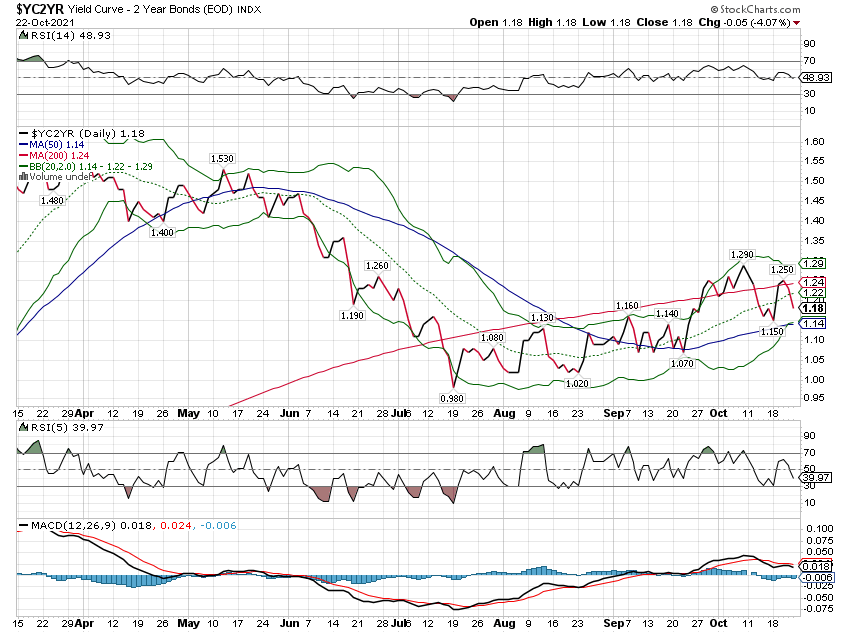

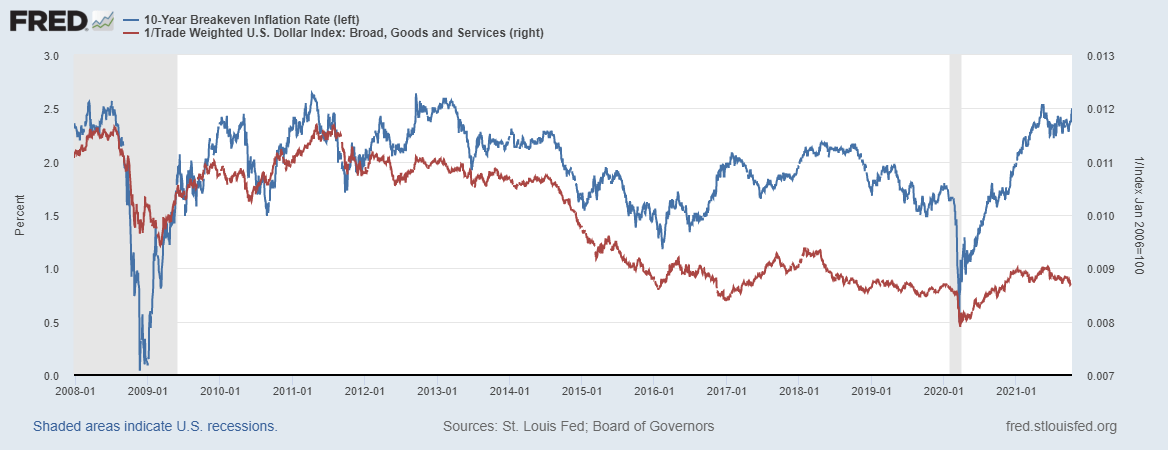

Weekly Market Pulse: Inflation Scare!25 Oct 2021

You Don’t Have To Take My Word For It About Eliminating QE24 Oct 2021

Weekly Market Pulse: Inflation Scare?

Weekly Market Pulse: Inflation Scare?11 Oct 2021

And Now Three Huge PPIs Which Still Don’t Matter One Bit In Bond Market15 Jul 2021

Rechecking On Bill And His Newfound Followers9 Apr 2021

What’s Going On, And Why Late August?29 Oct 2020