Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

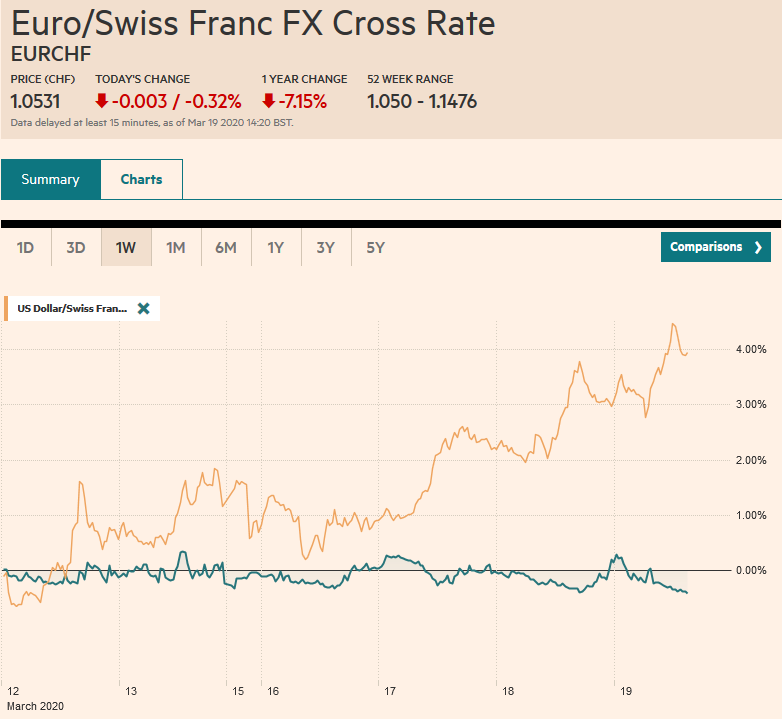

Swiss FrancThe Euro has fallen by 0.32% to 1.0531 |

EUR/CHF and USD/CHF, March 19(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

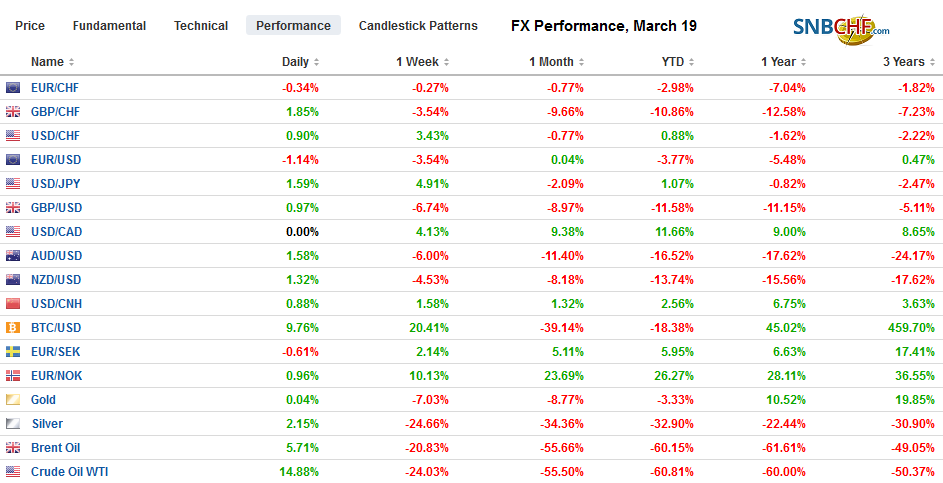

FX RatesOverview: It is not just that the dollar soared while stocks and bonds continued to plunge. The dollar’s strength is, in effect, a powerful short-covering rally. It was used to fund a great part of the global circuit of capital. The circuit of capital is in reverse now, and the funding currency is being bought back. The dollar’s strength is a function of the sell-off of other assets. Meanwhile, officials continue to announce more measures to combat the economic and financial fallout of the coronavirus. The ECB announced a substantial increase in its efforts, and the markets have responded well. Although Asian Pacific equities saw some large declines (e.g., South Korea -8.4%, Taiwan -5.8%, Australian -3.4%) Europe equities are firmer (Dow Jones Stoxx 600 +1.4%). The Philippines ‘ market re-opened for the first time since Monday (after a unilateral shutdown) and tumbled more than 13%. US shares are trading with a firmer bias. The more significant reaction to the ECB’s moves is the dramatic rally in European bonds (around Italy -70 bp, Greece -170 bp, Spain and Portugal -45 bp, France -25 bp). The US 10-year yield is about four basis points lower at 1.15%. The US dollar continues to motor higher. The Norwegian krone, dragged by the collapse of oil prices and illiquidity, has dropped around 6.5%. The Reserve Bank of Australia delivered an emergency 25 bp rate cut, and the Australian dollar is off almost 1%. The dollar is firmer against most of the major currencies. The Canadian dollar is the exception, and it is little changed. Indonesia and the Philippines cut rates too. While the rupiah is off 4.3%, the Philippine peso is a little firmer. Gold is pinned near its recent lows as it found new sales when poked above $1500. Oil is rebounding smartly (~+16%) after yesterday’s 24% swoon. |

FX Performance, March 19 - Click to enlarge |

Asia Pacific

Summary of policy actions in Asia-Pacific:

Japan–the BOJ offered to lend JPY2 trillion in an unscheduled auction. Tokyo is reportedly preparing a JPY30 trillion aid package, the third effort.

Australia–cut interest rates 25 bp to 25 bp, the effective floor and will target the three-year yield of 25 bp, as well. It will provide A$50 bln of funds for banks

Philippines–cut the borrowing and deposit rates by 50 bp to 3.25% and 2.75%, respectively. Local markets re-opened.

Indonesia–reduced the seven-day repo rate by 25 bp to 4.5%.

There are now more cases of the Covid-19 infection in Europe than in China. There were no more new cases reported in Wuhan today. The concern there is two-fold. New clusters of infection have been traced, according to reports, to people returning from overseas. There is also concern that as economic and social activity picks up, will there be a new flare-up?

The dollar reached new highs for the month against the Japanese yen near JPY109.55. Recall that on March 9, the dollar recorded a low around JPY101.20. At JPY108, the dollar has retraced (61.8%) of its losses. Since the high was made, the greenback has found support by JPY108.50, ahead of the option at JPY108.25 (for $1.2 bln) that expires today. The JPY110 offers psychological resistance. Before last weekend, the Australian dollar above $0.6200. Earlier today, it traded to almost $0.5500. It recovered later into the regional session to about $0.5800. A move above $0.5825 area could spur a move toward $0.5900. The US dollar’s strength is no match for the Chinese yuan. The dollar rose about 0.75% today after a 0.6% advance yesterday. It is above CNY7.10 for the first time since mid-October.

Europe

The ECB held an emergency meeting as European bonds cratered. In the five sessions since last week’s meeting, the 10-year German Bund yield has risen by 50 bp. The similar Italian bond yield is more than doubled by rising 125 bp. Last week the ECB increased its bond-buying program from 20 bln euros a month to about 33 bln euros (averaging out the 200 bln euro increase until the end of the year). At its peak during the sovereign bond crisis, it was buying 80 bln euros a month. Leaving aside a couple of miscues, the ECB, like other officials around the world, has slowly gotten their heads around the magnitude of the economic, financial, and social challenge that lies ahead.

Ahead of the open of the Asian market, the ECB announced a “Pandemic Emergency Purchase Program to buy 750 bln euro of public and private debt, flexibly guided by the capital key. The purchases will include Greek bonds, for the first time, and commercial paper. If this is averaged out over the next nine months, which is most likely will not be, it more than doubles the current buying by 73 bln euros a month. The issuer limit of 33% is under-review. Moreover, now loans to small and medium-sized businesses will be acceptable collateral. Recall the evolution. A 20 bln euro bond-buying program was announced late last year. Earlier this month, the ECB announced intentions to buy 120 bln euros of bonds this year.

The Swiss National Bank did not cut rates, as some expected. Although central banks are easing policy, those with negative rates, like the ECB and the BOJ, were reluctant to cut the negative rates any deeper too, and Sweden’s Riksbank did not return to negative rates but chose to resume its bond-buying program. The Swiss instead confirmed what many suspected, and that is it has stepped up its intervention, despite risking being taken to task by the US Treasury in its reports about the foreign exchange market. Also, the SNB tweaked the tiering or the amount of deposits subject to negative rates.

While the ECB’s announcement has helped the bond market, it has done little for the euro. It initially extended the bounce seen in the North American afternoon after approaching $1.08. However, it ran into fresh sales near $1.0980 in Asia and is back near the lows in the European morning. There is an option at $1.0825 for 2.3 bln euros that expires today. There is little chart support ahead of $1.05. Sterling’s slide is extending for an eighth session today. On March 9, sterling settled above $1.31. Yesterday it tested the $1.1450. Today, it has not been below $1.1470, but there is little enthusiasm for bottom-picking from 30-year+ lows. Ir ran into resistance in Asia near $1.1660 and has not been able to take that out in the European morning. If it does in North America, additional resistance is seen in the $1.1700-$1.1720 area. The UK is backtracking on its “herd immunity” approach and is closing schools and many subway (tube) stations. Prime Minister Johnson pushed against talk that Brexit (leaving the standstill agreement at the end of the year) may need to be delayed.

America

The Federal Reserve continues to dust off support programs that were used in the Great Financial Crisis. Support for commercial paper and prime deal lending has been announced, and yesterday support for the money market was announced. Re-starting the facility to support asset-backed securities (backed by student loans, auto loans, credit cards) may also be necessary.

The Senate approved the House bill, and President Trump signed it. The bill is the second effort after a small program (~$8.3 bln) had initially been launched. The House bill included sick-pay for small and medium-sized businesses, easier access to unemployment insurance, and food support. Another a much larger bill is in the making. The situation is fluid, but it is looking to be around $1.3 trillion. It would include around $500 bln for cash payments to households, perhaps means-tested, aid to the airlines (~$50 bln), and other industries (~$150 bln) and a payroll savings tax cut (which reportedly is seeing some pushback).

The Philadelphia Fed manufacturing survey for March, like the Empire State survey at the start of the week, will give some preliminary sense of the economic dislocation that is taking place. Still, the focus may be on the weekly US jobs claims. It is the most real-time economic report. Today’s report covers the week through last Saturday. Economists expect a modest rise, followed by a dramatic increase when this week’s report is made on March 26. Still, the risk is that there is a large bounce from the 211k reported in the week through March 7. The median forecast on Bloomberg calls for initial weekly jobless claims to rise to 220k. The high here in Q1 was in the middle of January at 223k. In the coming weeks, it will soar. Unemployment in the US is expected to more than triple, and the weekly jobless claims, while a different time series, will be a lead indicator.

The relentless dollar appreciation for the last two weeks has not been addressed via the dramatic action of the Federal Reserve in slashing rates, resuming QE, and providing new support facilities for segments of the capital markets and bank lending. Nor has reduced the cost of currency swaps with other central banks eased the pressure on the greenback. In fact, the cross-currency basis swaps are again under pressure. Our understanding of the shortage of dollars is a different type of shortage than seen during the Great Financial Crisis, which was more about counterparty risk. Coordinated intervention is at the upper end of the escalation ladder. More talk along these lines will likely surface unless the dollar stabilizes shortly.

The US dollar was below CAD1.35 ten days ago. It is near yesterday’s high now above CAD1.45. The risk-off and the collapse in oil prices are the main drivers. The Bank of Canada has slashed rates (by 100 bp) and has resumed unconventional policies. Support is seen CAD1.44 now, and the target is the CAD1.4690 area seen in January 2016. The greenback saw almost CAD1.4670 in Asia earlier today. Above there, CAD1.50 beckons. The Mexican peso continues to tumble. The US dollar is extending it gains further into uncharted territory and is approaching MXN25.00. Yesterday and today, the dollar found support at the previous day’s settlement. Yesterday, the dollar finished near MXN23.70.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Currency Movement,ECB,EUR/CHF,federal-reserve,newsletter,USD/CHF