Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

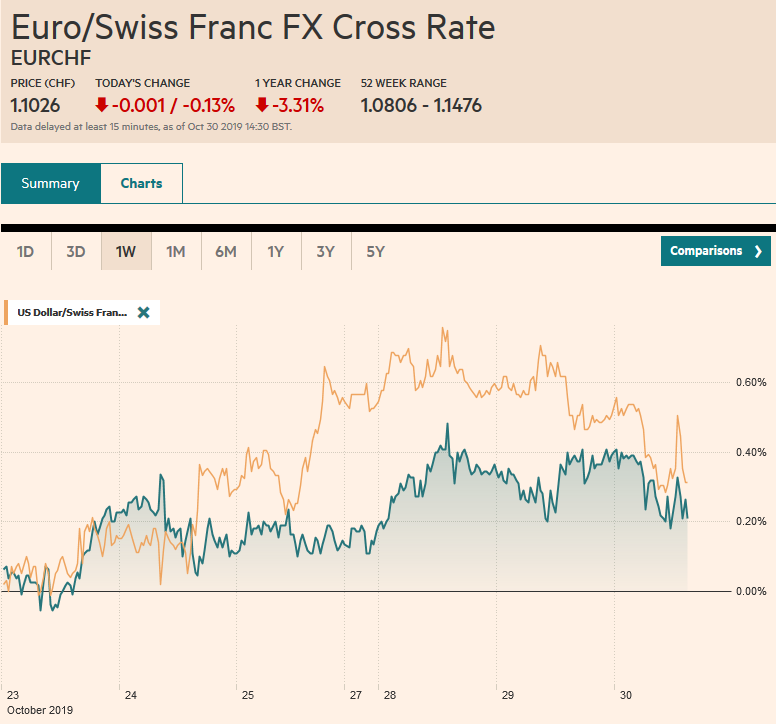

Swiss FrancThe Euro has fallen by 0.13% to 1.1026 |

EUR/CHF and USD/CHF, October 30(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

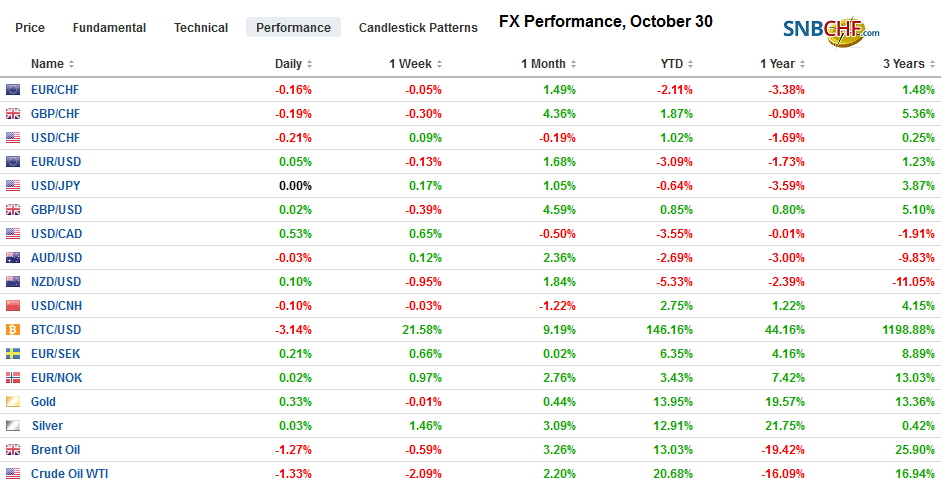

FX RatesOverview: The global capital markets are mostly treading water ahead of the Federal Reserve meeting. Asia Pacific and European equities drifted lower. The MSCI Asia Pacific Index appears to have snapped a four-day advance, while the Dow Jones Stoxx 600 was trading slightly lower for the second consecutive session following a six-day rally. The S&P 500 gapped higher on Monday did not enter the gap yesterday. It is found between 3027.4 and 3032.1. Benchmark 10-year yields fell in Asia but are narrowly mixed in Europe. The US 10-year yield is around 1.83%, having begun the month closer to 1.66% and settled last week a little below 1.80%. Note that the US Treasury will provide details of the quarterly refunding. While the size of the refunding may not change much, some are expected a couple innovations, including a 20-year bond and maybe an instrument tied to SOFR, the intended replacement of LIBOR. The dollar is sporting a slightly softer profile against the major currencies, and the Scandis are a notable exception. Meanwhile, the larger and accessible emerging market currencies have also edged higher against the greenback. On the other hand, the Korean won, which has rallied for four consecutive weeks, is off about 0.5% amid profit-taking ahead of month-end. Gold is a little firmer though below $1500, and oil has slipped a bit with December WTI though within yesterday’s ranges. |

FX Performance, October 30 - Click to enlarge |

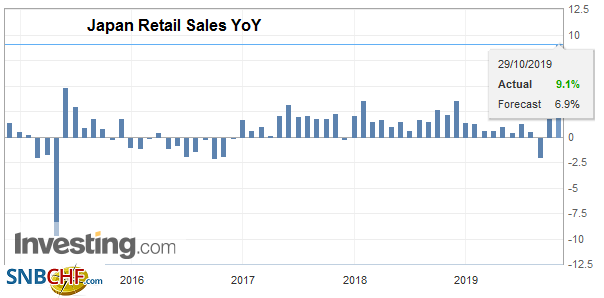

Asia PacificAhead of the increase in Japan’s sales tax, households went shopping. September retail sales jumped 7.1%, which is a little more than twice when the median forecast anticipated. The August figure was revised slightly (4.6% from 4.2%). The year-over-year rate rose to 9.1% in September from a revised 1.8% in August. The sales tax increase brought forward purchases, but in the past, it was followed by a deep swoon. The Bank of Japan meets tomorrow. Expectations of a rate cut have diminished, but many expect officials to extend their forward guidance about how long rates can remain low. It could shift from a date-specific back to a data-focused approach. The BOJ is the only major central bank that buys equities (ETFs) as part of its quantitative and qualitative easing. Its holdings are draining liquidity from the equity market, though Nomura, the largest brokerage firm, reported its best profits in almost 20 years. Some reports are suggesting that the BOJ could begin a securities lending program for these ETFs in an attempt to restore liquidity. |

Japan Retail Sales YoY, September 2019(see more posts on Japan Retail Sales, ) Source: investing.com - Click to enlarge |

Australia reported Q3 CPI figures, and they were mostly as expected, showing little change in the pace. The headline rose 0.5% the same as in Q2, which saw the year-over-year rate rise to 1.7% from 1.6%. The trimmed mean rose 0.4%, also matching the Q2 increase and expectations, keeping the year-over-year rate unchanged at 1.6%. The weighted-median rose 0.3%, compared to 0.4% in Q2. The year-over-pace slipped to 1.2% from a revised 1.3%. The takeaway is that expectations for the Reserve Bank to be on hold next week hardened. Indeed, the next rate cut appears to have been pushed into late Q1 2020.

The dollar has flatlined against the yen. It has been in about a 10-tick range below JPY108.90 through the Asian session and into the European morning. The JPY109 level remains important. There are $2.1 bln in options struck there today that will be cut and another $1.4 bln tomorrow. The Australian dollar has traded mostly in the quarter-cent above $0.6850. Last week’s high was a little shy of $0.6885, and the September high was a touch below $0.6900. These denote the nearby obstacles. The Aussie has not traded above $0.6900 for three months. Meanwhile, the greenback remains stuck near its recent trough against the Chinese yuan around CNY7.0560 in quiet turnover. The market seems to accept that the current tariff truce can persist as both economies are slowing.

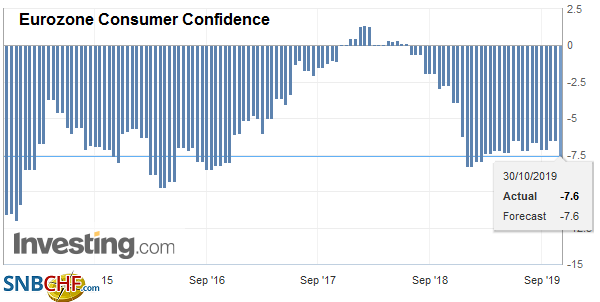

EuropeThe UK is going to hold its third election in four years on December 12, as Labour capitulated. The claim is that the election will resolve the issue, but what if it doesn’t? Is that the underlying problem? Even the referendum in 2016 showed a narrowly divided country. As nearly everyone has relearned, the devil is in the details. How to leave? What to leave? There seems to be a substantial risk that the election does not resolve the issue. No party may get a majority and six-seven weeks later the next deadline, and it is not clear that another extension will be granted. The triggering of Article 50 without have a consensus on a range of other issues seems backward. The EU could insist on the UK revoking it to overcome the end of the January deadline. France is the first of the G7 economies to report Q3 GDP. It expanded as expected by 0.3% the same as in Q2 for a 1.3% year-over-year pace (1.4% in Q2). However, it appears households went on strike in September as consumption fell unexpectedly by 0.4%. This is the biggest decline since February. German states are reported October CPI figures ahead of the national estimate later today. The early estimate suggests that the year-over-year pace on the national level may have slowed from September’s 0.9% rate. Prices edged lower (0.1%) in both August and September. Three consecutive monthly declines have not been reported since 2002. Separately Germany reported twice the rise in unemployment (6k) than the median forecast anticipation in the Bloomberg survey. The ECB’s bond-buying program resumes today. It will buy roughly 20 bln euros a month in sovereign bonds. The program is open-ended, and this irked some officials and former officials from several creditor members. Many private-sector economists worry about the proximity of the self-imposed caps on ECB holdings. Draghi tried to play the urgency down, reiterating the claim by the ECB’s chief economist, that the limits will not be approached until late next year. This gives Lagarde and the ECB time to develop a more granular strategy. |

Eurozone Consumer Confidence, October 2019(see more posts on Eurozone Consumer Confidence, ) Source: investing.com - Click to enlarge |

The euro posted an outside up day yesterday by trading on both sides of Monday’s range and then closing above Monday’s high. Follow-through buying today lifted it to almost $1.1125 in the European morning. There is an option for nearly 850 mln euros that is struck there and expires today. We had anticipated a bit more weakness in the euro, as the market looked past the likely Fed cut to focus on the pause that is widely expected to follow today’s move. However, we had looked for the euro to recover ahead of the weekend after what we expect to be a soft jobs report. So far, today is the first day since October 23 that the euro has not traded below $1.11. Sterling is trading in the upper end of yesterday’s range, but like yesterday, the air about $1.29 is thin.We note that three-month volatility is steady near 9.9%, which, to give some perspective, is a little above the 200-day moving average and new three-month lows. The euro has formed a shelf over the past couple of weeks near GBP0.8600. An option for about 460 mln euros struck at GBP0.8650 that will be cut today is nearby (at pixel time it is around GBP0.8635).

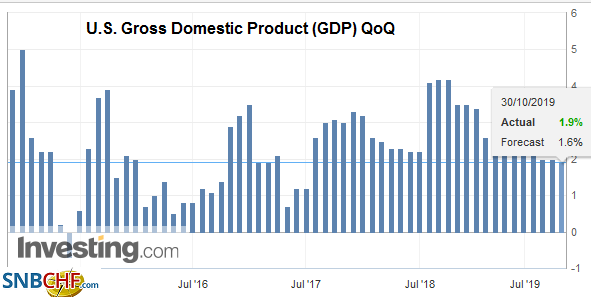

AmericaThe US begins with the ADP private-sector jobs estimate followed quickly by the first estimate of Q3 GDP. Attention will briefly turn to the outcome of the Bank of Canada meeting and then in the afternoon the conclusion of the FOMC meeting and Chairman Powell’s press conference. The ADP estimate is expected to show around 110k increase in private sector jobs. It is unlikely to reflect the full impact of the labor strife, which will more likely be picked up by the government’s estimate at the end of the week. Nevertheless, the trend is clear. According to ADP, the private sector has created an average of 164k jobs a month this year. The average in the first nine months of 2018 was 222k. After expanding at a 3.1% year-over-year clip in Q1, the economy slowed to 2.0% in Q2, and the question at hand is how much did it slow in Q3. Most estimates are around 1.5%. Still, the risk may be on the downside given that the consensus forecasts have been above what has been actually delivered in recent weeks, especially for the more significant economic reports. The economy finished Q3 with little forward momentum. |

U.S. Gross Domestic Product (GDP) QoQ, Q3 2019(see more posts on U.S. Gross Domestic Product, ) Source: investing.com - Click to enlarge |

Yesterday, we explained why midcourse correction (three rate cuts) will be completed later today and that the most important part of tomorrow’s meeting is likely to be the forward guidance. The impact of that forward guidance is contextual. What are the current market expectations? The CME’s model suggests a little less than a one-in-four chance of a December hike has been discounted, and the Bloomberg model puts it just below a 30% chance. The point is that a pause is mostly expected. The next question where is the bar to another a continuation of the easing cycle, the morphing of the midcourse correction to “let’s blow some air the parachute” to ensure a soft landing. We suspect that further economic slowing will get the Fed to resume its easing.

The other issue is how the Fed is addressing the pressure on the short-term funding market. While some observers continue to insist that it is QE, it appears that most institutional economists and analysts do not. The Federal Reserve is defending the transmission mechanism. That is its motivation for conducting overnight and term repo operations and buying $60 bln a month in T-bills until into Q2 2020. Many do not appreciate the change in the regimes at the Federal Reserve from a system based on the scarcity of reserves to a system of an abundance of reserves. Despite some numbers that look like banks should have sufficient reserves, the argument is that new post-crisis liquidity regulations encumber excess reserves and provide incentives to prefer cash to securities. Treasury Secretary Mnuchin seemed sympathetic to bank calls to lighten the regulation. This will be not an important factor in the Fed’s deliberations. They have to deal with present conditions. Changing the regulations cannot be in time for year-end pressures, for example.

The Bank of Canada meets and is widely anticipated to stand pat. The economy and prices have been resilient in the face of the global slowdown and the weaker US growth. After peaking near CAD1.3350 on October 10, the US dollar has fallen toward the year’s low below CAD1.3050, some short-covering in an extended market appeared to lift it back toward CAD1.3100 yesterday. The US dollar posted a potential key reversal yesterday. It is an outside up day that made a new extreme for the move. Yesterday, the US dollar fell to new three-month lows near CAD1.3040 before reversing higher. However, while still early for it, there has been no follow-through US dollar buying today.

Mexico reports Q3 GDP today. The economy was virtually flat in Q2 (.02) after contracting by 0.26% in Q1. It appears to have down a bit better in Q3, with the median forecast in the Bloomberg survey looking for a 0.2% increase. If so, the year-over-year pave, which slipped into contraction in Q2 for the first time since 2009, would be flat. The central bank has begun easing policy, and it meets again on November 14. The official cash rate as cut in August and September. The market appears to be looking a cut in December rather than next month, though disappointing data and lower inflation could spur an earlier move. From those scary days in late August, when the dollar pushed through MXN20.20, the peso has staged an impressive recovery. Its 6%+ advance has seen the greenback test support ahead of MXN19.00. The dollar remains pinned near the lows though the downside momentum has eased.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Bank of Canada,Brexit,Currency Movement,EUR/CHF,Eurozone Consumer Confidence,federal-reserve,Japan Retail Sales,newsletter,U.S. Gross Domestic Product,USD/CHF