Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

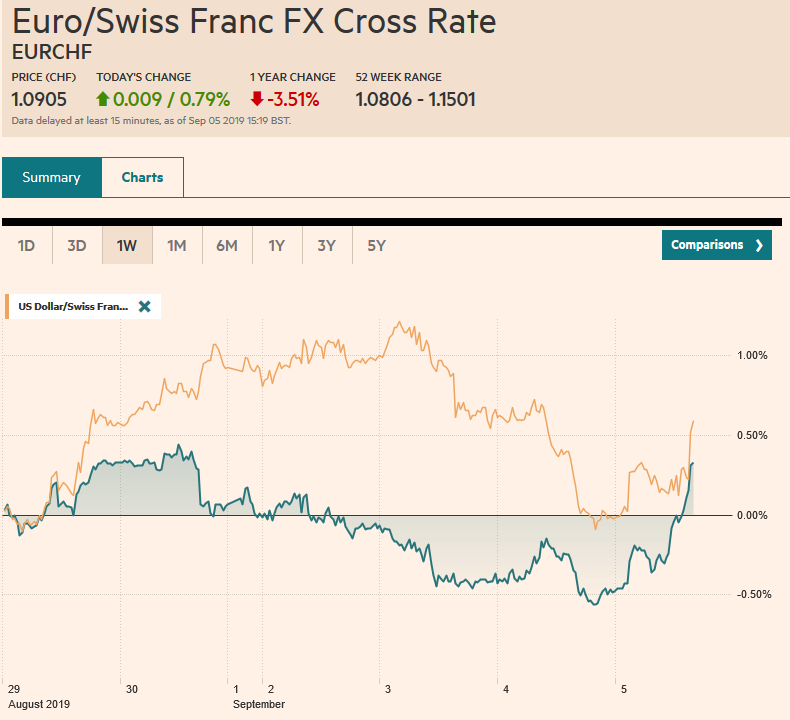

Swiss FrancThe Euro has risen by 0.79% to 1.0905 |

EUR/CHF and USD/CHF, September 05(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The Dollar Index fell the most in three months yesterday and is experiencing mild follow-through selling today. With hopes that Hong Kong has turned a corner, news that in-person US-China talks will resume next month, and a no-deal Brexit is well on the way to being averted, investor risk appetites are robust today. Global equities are higher as are benchmark yields, while gold is being pushed back below $1550. Most Asia Pacific equities advanced, though India and Malaysia were exceptions and Hong Kong saw a bout of profit-taking after yesterday’s surge. In Europe, the Dow Jones Stoxx 600 is advancing for the third consecutive session and the fifth in six sessions to trade at one-month highs. The S&P 500 has been crisscrossed the 2820-2950 range several times in recent weeks and is poised to gap above the top today. Interest rates are backing up, and the 10-year yields are 3-5 bp higher. The dollar is edging lower against most major and emerging market currencies. Among the majors, the yen and the Swiss franc are experiencing minor losses, while among the emerging markets, the Turkish lira is off about 0.25%. The lira may snap a three-day, five percent advance as Prime Minister Erdogan weighs in again on the need for aggressive rate cuts to ambitious growth hopes. |

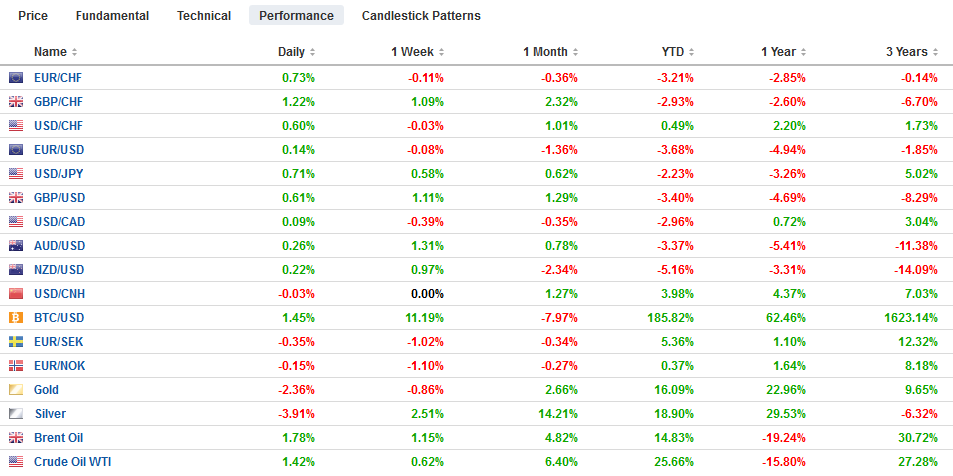

FX Performance, September 05 - Click to enlarge |

Asia Pacific

The PBOC’s dollar reference rate has been extremely stable in around CNY7.0850, and it is the market that blinked first. The dollar’s broad pullback yesterday saw the model projections eased below CNY7.0940. The onshore and offshore yuan has also converged near 7.1460. Chinese officials have been slower to roll-out additional stimulus than many observers have expected. We had thought there was a good chance of a cut in reserve requirements over the summer. Nevertheless, the State Council appears to be hinting of action soon, and a window of opportunity is seen before the October 1 national holiday.

With the latest round of tariffs and counter-tariffs in the US-China spat going into effect on the start of the month, securing face-to-face meetings proved difficult. This had contributed to the pessimism. However, now Chinese officials will come to the US next month, according to reports. Still, the prospects of a deal are remote. Trust between the two at a low ebb after two tariff truces were ended by the announcement of new action on Twitter, and China shows reluctance to change fundamental behaviors. Separately, the US trade figures show that China was the third-largest buyer of US crude oil in June and July (buying 5.7 mln barrels and 7.1 mln barrels respectively). South Korea was the largest buyer, followed by Canada. China puts a 5% levy on US crude as of September 1.

Japan auctioned new 30-year bonds and saw healthy demand (bid-cover 3.45x after 3.50x last month). Although 20- and 30-year bond yields fell to fresh three-year lows, the yields are still positive. Japanese investors are eager for positive returns and stepped up their purchases of foreign bonds last week (~JPY1.5 trillion), the most in a couple of months. For some investors who can hedge their Japanese bonds back into dollars, the shapes of the relative yield curves and cross-currency swaps mean that the return can be greater than US Treasury yields.

With one exception, the dollar has been confined to a JPY105 to JPY107 range for a full month. The greater risk appetites are helping lift the dollar toward the upper end of the range. It traded to JPY106.75 in early Asia. It pulled back to about JPY106.35 and appears poised to retest the highs today, though JPY107 may be a formidable barrier still. The Australian dollar is pushing higher for the third consecutive session, its longest winning streak in nearly two months. It reached $0.6825, which is its strongest level since August 1. Note that the five-day moving average is poised to move above the 20-day moving average for the first time since July 25. The $0.6830 area corresponds to a (38.2%) retracement of the leg down that began in mid-July. The next retracement target is near $0.6880.

Eurozone

UK Prime Minister Johnson suffered two defeats yesterday. First, the House of Commons again passed the motion to compel a request for a three-month extension unless an agreement with the EU is approved by the middle of October. Although the motion was amended to include a reconsideration of Withdrawal Bill negotiated by May, no agreement is likely by the mid-October, as the government has reportedly failed to make a single new proposal. It was betting that the EC would capitulate at the last moment. An attempt to filibuster in the House of Lords ended relatively quickly. Following its approval, the bill will return to the House of Commons tomorrow. Johnson, some thought, maneuvered to force an election, which he said he did not want. But, another gift of Cameron’s, was to make it difficult for a Prime Minister to call a snap election. Johnson again gambled and misread his opposition. They successfully blocked his effort. There is some talk that he may try again next week to force an election.

In the strange, convoluted tactical battle, Corbyn appears to have become the first opposition leader to stand in the way of an election. An election is coming but just not on Johnson’s terms. It is not clear if the 21-22 rebellious MPs really lost the whip, which would mean that could not stand as Tories in the election. The referendum that Cameron wagered would unite the party has torn country and party apart. Most importantly, the extension is not a done deal. Why is the UK seeking an extension? Will it simply prolong the uncertainty? Labour accepts the need for an election after the October 31 deadline is averted, meaning an election in November, which might be the condition for a final extension.

German factory orders disappointed. After a 2.5% increase in June orders, economists had expected a modest 1.4% decline. Instead, factory orders fell 2.7% offsetting the June increase that was revised to 2.7%. The year-over-pace decline slumped to 5.6% from a 3.5% decline in June. Domestic orders fell by 0.5%, while foreign orders were off 4.2%.

Sweden’s Riksbank surprised the market by not giving up its hawkish tilt. The unanimous decision maintained the bias toward exiting its negative interest rate policy but at a slower rate than envisioned previously. The central bank is signaling a rate hike either late this year or early next year. With the ECB poised to ease policy next week and the elevated trade tensions, many are skeptical that the Riksbank can deviate so much. Still, the krona is the strongest of the majors today following the surprise.

The euro is firm near yesterday’s highs but is bumping against important resistance. The $1.1045 level that has been tested today corresponds to a (50%) retracement of the leg lower from August 26. There are also two option expirations today that may also slow the upside progress. There is a nearly 530 mln euro option at $1.1035, and 1.6 bln euros are $1.1050. A move below $1.10 would likely be seen as a signal that a high is in place. Sterling is bid and extending yesterday’s gains slightly. It appears poised to challenge last month’s high set near $1.2310. There is an option for about GBP516 mln at $1.23 that expires today. Look for initial support near $1.2240.

United States

The US reports a slew of data today, but it is unlikely to impact deeply held ideas that the Federal Reserve will deliver its second rate cut of the year in a couple of weeks. The most market-sensitive report today is the ADP estimate of private-sector jobs growth. It comes ahead of the government employment report tomorrow and is expected to be consistent with a modest slowing of job growth. The ADP estimated job growth in July was 156k, and the government’s initial estimate was 164k. The August service/non-manufacturing PMI/ISM are expected to show some resiliency while manufacturing was soft. July durable goods is a revision, while factory orders may be boosted by transportation orders.

The Canadian dollar posted its biggest advance since January after the Bank of Canada seemed to have issued a fairly neutral statement after it decided not to change policy. It is seeing some follow-through buying today. However, it acknowledged that the economy is likely to weaken in H2 and underscored trade risks and related issues, leaving many still looking for a rate cut this year. The odds of a rate cut in October eased from around 60% to closer to 50%. A move ahead of year-end was tweaked to about 68% from 70%, interpolating from the OIS market. Prior to the Bank of Canada meeting, the July trade figures were released. Exports fell by 0.9% while imports rose 1.2%, resulting in a widening of the trade deficit (C$1.125 bln). This was about the average recorded in H1 19. The decline in exports is misleading. It was largely a reflection of the 7.7% drop in Canadian crude prices which cut oil exports by 6.7%. On a volume basis, exports slipped 0.1%. Exports to China fell by 15.5%. This is not only a result of the slowing of the Chinese economy and the US-Chinese trade tensions, but Canada has also been subject to China’s wrath.

The US dollar traded below CAD1.32 for the first time August 13, which corresponds to a (50%) retracement of the rally since mid-July. The intraday technicals are stretched and suggest not chasing it. A US dollar bounce is likely to be limited to the CAD1.3230 area. There are $1.1 bln in expiring options struck between CAD1.3240 and CAD1.3250. The Mexican peso has done well as risk-appetites return. The US dollar, which pushed through MXN20.20 last week, approached MXN19.64 today. The MXN19.60 area marks the (50%) retracement of the greenback’s gains since the end of July. Below there, the next target is in the MXN19.40-MXN19.45 area. The Dollar Index has spent the last several weeks alternating between gains and losses. Last week was an up week, and the pattern is being maintained by the heavier tone this week. It is approaching the (50%) retracement of its gains from the August 23 low and the 20-day moving average, which converge near 98.20. It probably will take a break of 98.00 to temper the bullish sentiment.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Bank of Canada,Brexit,Currency Movement,EUR/CHF and USD/CHF,newsletter,Riksbank,SEK