Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

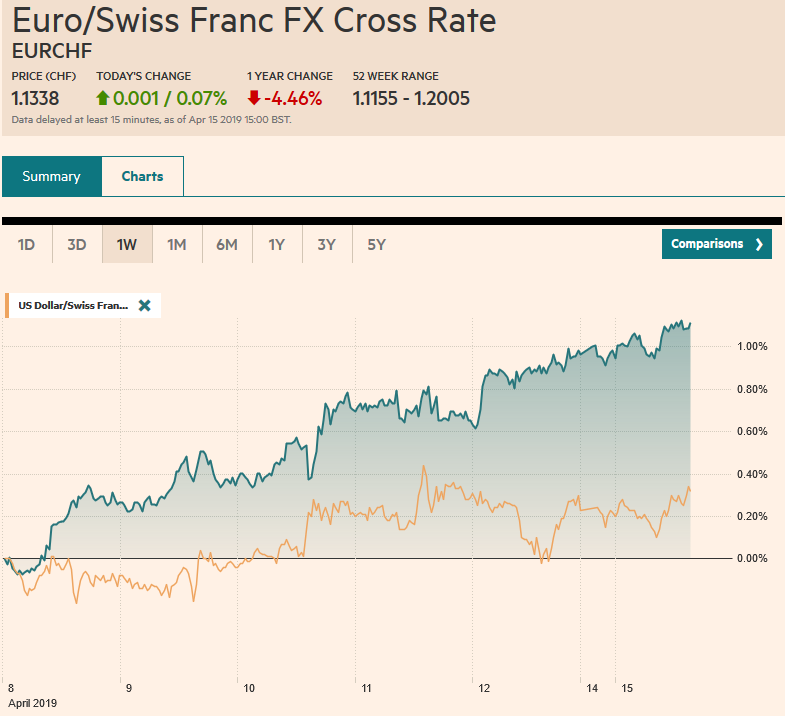

Swiss FrancThe Euro has risen by 0.07% at 1.1338 |

EUR/CHF and USD/CHF, April 15(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The holiday-shortened week is off to a slow, tentative start. The surge of the S&P 500 before the weekend failed to inspire today. Asia markets were mostly firmer, led by Japan, while China, Hong Kong, and Singapore moved lower. The Nikkei gapped higher, jumping above the 22k level that had been holding it back. It is at its best level since early last December. The US coattails are even shorter in Europe, where the Dow Jones Stoxx 600 is little changed, with a three-day rally in tow. US shares are a little heavier. US Treasuries are consolidating the pre-weekend drop, which weighed on Asia-Pacific bonds earlier today, and European benchmark yields are firmer, with Italy bucking the trend. The dollar is mostly softer, with sterling and the Swedish krona the strongest of the majors (~0.20-0.25% higher), while the Australian and Canadian dollars are lightly softer, alongside the Norwegian krone. The South Korean won is the strongest of the emerging market currencies today, helped by the rally in US stocks and Chinese economic data. |

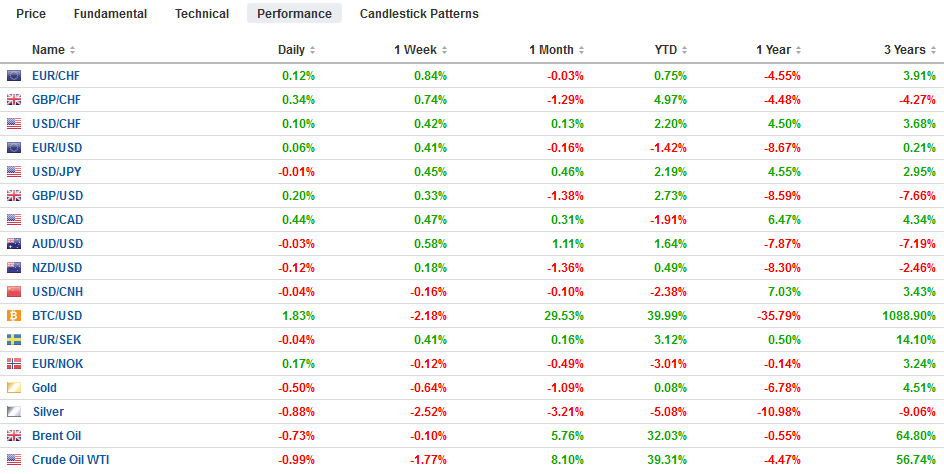

FX Performance, April 15 - Click to enlarge |

Asia Pacific

US Treasury Secretary Mnuchin suggested that the trade talks with China are nearly complete. He acknowledged, it seemed for the first time that the enforcement mechanism would work both ways, meaning that the US could also be subject to repercussions if it were to fail to make good on its commitments. Still, US officials have been claiming progress on a nearly daily basis. When a date is set for the next Trump-Xi meeting, that will be the best indication that a deal has been reached. Note that unlikely NAFTA 2.0, this is not a treaty that requires Congressional approval. This is an executive agreement.

The US-Japanese trade negotiations begin in the middle of the week. This too will be an executive agreement that does not require approval from Congress. Some critics see these executive agreements as a way to bypass the legislative branch. Talks this week will lay the groundwork for Abe’s US visit later this month. Part of the problem is that Japan has struck agreements with Europe and the Trans-Pacific Partnership and it now grants others greater access than the US This has hit the US agriculture, where US pork exports to Japan, for example, are off by more than a third this year. As the US insisted in the NAFTA 2.0 talks and in negotiations with China, it seeks protection against currency manipulation, which seems to be mostly a question of transparency of actions. Japan does not appear to have intervened in the foreign exchange market for several years.

China

China reports March industrial production and retail sales and Q1 GDP in the middle of the week. Sequentially, March industrial output and retail sales are expected to have improved, while Q1 GDP is expected to have slowed to 6.3% (year-over-year) from 6.4%. Chinese lending and trade figures released last week confirm officials have switched gears and are doing more to support the economy. The strong export figures are good for China but also reflect stronger world demand.

The dollar has been confined to about a 10-tick range on either side of JPY112.00, where a $640 mln option expires today. Technically, a convincing move above JPY112 would target JPY114. We remain concerned that not only is the Japanese economy struggling to show any meaningful traction but the closure of the markets for a long period at the end of the month, as the abdication of the Emperor and the ascension of the new Emperor, is potentially disruptive. The market is pausing after bringing the Australian dollar close to $0.7200. It has not closed above this level in more than two months, and the market has not given up on it. Initial support is seen in the $0.7140-$0.7160 band. Foreign investors continue to favor South Korean shares. This month, they have plunked down more than $2.0 after buying more than $4.5 bln in Q1. Demand for Indian shares appears to have cooled this month after foreigners bought roughly $8.2 bln in Q1.

United Kingdom

The UK Parliament is on recess until April 23. In the meantime, the government and Labour continue to talk. The situation still looks fluid and continues to be talk of some kind of customs union arrangement. A referendum on the final agreement remains an open possibility. In the end, maybe it is a be reminiscent of how France removed its troops from joint NATO command, but still exercised and prepared with NATO and later relented, and its forces were again part of NATO’s command structure. Observers will scrutinize the May 3 local elections for signs of the political consequences.

Eurozone

The Social Democrats came out narrowly ahead in the national elections in Finland for the first time in 16 years. The populist Finns came in second. It has added a hostility to policies (and taxes) meant to address climate-change to its anti-immigration rhetoric. The market reaction appears to be limited to some additional pressure on the short end of its curve, where the two-year yield is up four-five basis points, the worst performer in Europe. The stock market is heavy, losing about 0.4% today and paring this month’s gain to a still-impressive 3.6%. The 10-year yield is up half of a basis point at 0.27%. The Social Democrats now need to forge a coalition, and this may force it to be centrist.

An estimated 31k Yellow Vest protesters took to the streets this past weekend. This evening in Paris (before the US equities close), President Macron will make a national address. Later this week, Markit will report the flash April PMI. Recall in March that both the manufacturing and service PMIs were below the 50 boom/bust level. While France’s voice in Europe has not lessened, as illustrated by the shorter Brexit extension than the European Council President Tusk proposed, the economic weakness keeps Macron on the defensive nationally. The European Parliament elections at the end of next month may seem him punished.

The euro is consolidating last week’s gains that took it above $1.13 for the first time since March 26. It is not managed to push through the pre-weekend high of just below $1.1325. There is an option for 555 mln euros at $1.1335 that will be cut today. Chart resistance is seen near $1.1350, though some are talking about a move to $1.1400. Initial support is pegged near $1.1290, and a break of $1.1280 would likely signal a near-term top and the start of a potential reversal. Sterling is firm in a narrow range. The general consolidative tone remains intact. The $1.3120 area is important. It houses a GBP300 mln option that expires today and the 20-day moving average. Sterling has not closed above its 20-day moving average since March 27. Support is pegged near $1.3050.

United States

President Trump again took to Twitter to criticize the Federal Reserve, claiming the stock market and the economy would be much stronger had the central bank not engaged in quantitive tightening. The President’s comments and his candidates for the Federal Reserve Board of Governors have sparked widespread criticism and concern about the central bank’s independence. ECB Draghi, who rarely comments on US developments, expressed concern about the Fed’s independence. Although we will address it in a longer note later, for now, allow us to make two points. First, observers may be tut-tutting, but investors see past it. Market prices, level of interest rates and the slope of the curve do not indicate investor concern that the Fed has been compromised. Second, neither Moore nor Cain has been officially nominated. The Senate has sometimes failed to confirm nominees. Many expect Cain to remove himself or that the President does not go forward with the nomination. The power of appointment to the central bank is the approved way to influence the direction of monetary policy in many countries, leaving aside the ECB. The system of checks and balances is working.

Eight Fed officials speak this week, beginning today with Evans and Rosengren. The data diary begins with among the first looks at April (outside of the weekly jobless claims which point to a robust labor market). It is expected to have improved, but this week’s focus is on March industrial output and retail sales. Both are expected to have improved sequentially. Also this week, earnings from the financial sector are among the highlights. Canada reports March existing home sales today. They fell 9% in February, and a small bounce is expected. The Canadian dollar will likely be the brunt of disappointment. The Bank of Canada’s Senior Loan Officer Survey results will also be announced.

The Dollar Index is trading in a narrow range near the pre-weekend low (~96.75). Additional support is seen near 96.60. Some observers think that that stale longs have to be forced out and this may take a push through the 200-day moving average (~96.10). With a few minor exceptions, the US dollar has chopped betweenCAD1.33 and CAD1.34. Playing the range makes money now for the nimble, but leaves on not necessarily prepared for an eventual breakout. Meanwhile, the market seems reluctant to extend the greenback’s 3.5% two-week loss against the Mexican peso. It is finding a modest bid near MXN18.75.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,EUR/CHF and USD/CHF,Federal Reserve,MXN,newsletter