Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

It seems to be well appreciated among by policymakers and investors that the system is ill-prepared to cope with another financial crisis. It is understandable that so many are concerned that the end of the business cycle could trigger a financial crisis. In practice, it seems like it has worked the other way around. The financial crisis triggered the Great Recession. The economy previously contracted when the tech bubble popped.

Similar thinking emerged after WWII. The fear of a return to the pre-existing depression conditions and the threat of the spread of communism shaped both the domestic and foreign policy objectives. Stimulative policies and a stable monetary order (Bretton Woods), reduced trade barriers (GATT) and the World Bank and IMF were to assist development and external imbalances.

The causes and triggers of the equity market slide in Q4 may not be fully understood, but policymakers have been spooked by the tightening of financial conditions and the loss of economic momentum. The Federal Reserve went from balance sheet reduction and rate hikes in December to a neutral stance. Even before the ECB staff revised its economic forecasts, Draghi had changed the risk assessment. A new targeted loan facility will be forthcoming, and there is increased talk in tiering the deposit rate with the idea in mind to lower the cost of negative interest rates.

GermanyTwo different things may be at work here. First, simply the consideration of tiering means that negative rates will last longer. Until now, the ECB officially has implied that the negative interest rates are working and generating little secondary damage. However, the longer it goes, the risks would seem to rise. Moreover, given the contraction in the Germany economy in Q3 18 and the flattish figure for Q4, perhaps Germany needs some of the same stimulus that Italy can use. Second, it could be a way to keep the creditor nations on-side. The long-term loan facility is understood to benefit the debtors in Southern Europe, who especially relied on the past TLTRO operations. A tiering of the negative deposit rate would help those with the deposits, namely the creditors, like Germany and the Netherlands. Germany’s manufacturing remains challenging. It declined in March (-0.2%) for the fifth time in six months. The external sector appears to be the main drag (it was what pushed factory orders into contraction). Germany export-driven economy was hit with three shocks, the slowing of China, Brexit, and Turkey. The challenges to its diesel-heavy auto sector did not help matters. However, the strength of retail sales and construction suggest the domestic economy has some traction. |

Economic Events: Germany, Week April 08 - Click to enlarge |

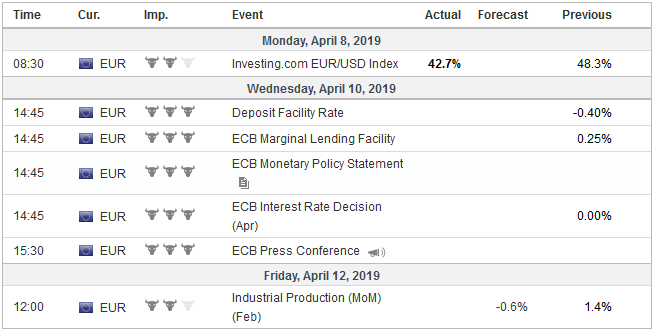

EurozoneThe ECB meets on April 11. The focus will be on two elements. The forward guidance and any details on the terms of the new TLTRO. There is talk that the ECB would extend its commitment not to lift interest rates. The challenge here is that President Draghi steps down later this year and it is impolitic to handcuff his successor for too long. The terms of engagement for the new loan facility may not be ready until June. In some ways, since the bulk of the funds will likely be used to repay previous borrowings, there is not much urgency now, even if it may impact Net Stable Funding Ratio metrics in H2. There are two other considerations here. First, the euro has fallen on days the ECB has met with one exception since the start of last year. This is not technical. It is fundamental. For most of this period, the ECB has been dealing with an economic slowdown and has been dovish. Second, German, France, and Italy have revised down GDP forecasts since the 2019 budgets were approved by the EU. Slower growth means larger deficits as a percentage of GDP, which in turn may require remedial action, such as a VAT increase in Italy. The early animosity between the populist-nationalist Italian government and the EC has been dialed back, and neither are questioning the other’s legitimacy. The League is poised to do well in the EU Parliament elections at the end of next month. There is no need for drama. The drama maybe not from the ECB as much as from the ongoing theatric tragedy of Brexit. The House of Commons could not agree on any alternative course but did manage to see a majority instruct the Prime Minister to seek an extension in Brussels. Meanwhile, May had reached out to Labour to see if a resolution could be found. The talks apparently have not gone anywhere. When an extension was requested, it was for the end of June. Ostensibly this is before the next EC takes office, though after the EU Parliament election. Previously, it seems clear that May was told by Brussels that the next request for an extension should be a long one as they had no interest in repeated extensions. This would be the second. An EU summit late next week that will decide. The general sense was that the shortest extension that many officials see is a year. Besides disappointing those who had hoped the UK would be out of the EU by now, and extending the economic and financial uncertainty, such an extension would require the UK to participate in the EU Parliament elections and other EU-decision making procedures. Could anyone do that in good faith? |

Economic Events: Eurozone, Week April 08 - Click to enlarge |

II

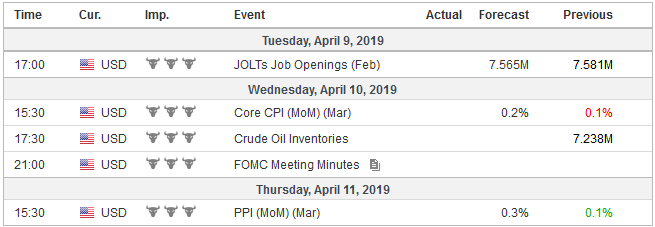

United StatesThat inversion of the US yield curve (three-month to 10-year) that caused so much consternation? Never mind. It finished the week with a positive slope of a little more than 10 basis points. The two-year to 10-year spread also steepened slightly. While the US jobs data were not spectacular, they were solid. There were 196k net new jobs created in March, underscoring that the revised 33k increase (from 20k) in February. The unemployment rate remained at 3.8%, despite the decline in the participation rate. The day before the national figures, weekly jobless claims fell to new 50-year lows. There were some troubling elements, like a loss of 6k manufacturing jobs. The risk here is some observers will blame the strong dollar instead of lagging capital investment and boosting productivity. Earnings growth disappointed as it slowed to 3.2% year-over-year from 3.4%. However, this was partly driven by another element of good news–the work week expanded to 34.5 from 34.4 hours. An increase in the work week often sees a decline in average hourly earnings. The participation rate fell to 63.0% from 63.2%. The labor force declined by almost 225k. It is tempting to write this off as the baby-boomers retiring, but something else is at work, or not, as the case may be. The participation by 34-44-year-old men ties a record low set in the 1950s. The important takeaway from the employment data is that it is not signaling a recession. Calls for a 50 bp rate cut, or Trump’s call to restart quantitative easing seem far from the Fed’s thinking. No sitting Fed president or Governor has endorsed those calls. We correctly anticipated the Fed officials to push back, justify their neutrality. Short-term real interest rates in the US are still negative. The Fed’s “wait and see” posture will be on display in the FOMC minutes that will be released on April 10. A few hours before the minutes, the US will release March CPI figures. Our “green shoots” hypothesis also requires that disinflation pressure ease. Headline CPI is expected to firm from 1.5% in February to 1.8% in March. The core rate needs to rise by 0.2% (after a 0.1% increase in February) to keep the year-over-year rate at 2.1%. Separately, import prices are also expected to continue to firm with a 0.4% gain following February’s 0.6% increase. Import prices had fallen 1.3% year-over-year in February and March may have seen the decline pared to 0.4%. A big part of the story is oil prices. Light sweet crude oil (WTI) for May delivery finished 2018 near $46 a barrel. It traded a whisker away from $63 a barrel. This nears an important technical retracement of the decline in Q4 18. Despite Trump’s plea to boost output, OPEC+ is showing discipline. Meanwhile, later this month, the Administration will announce if the exemptions to the Iranian oil embargo will be extended. The most likely scenario seems to not to renew all the exemptions. Those that did not use them would be low-hanging fruit without altering supply. The more dangerous shot across the bow were reports suggesting that if the US revokes OPEC’s exemption from its anti-trust lows as some in Congress continue to press, Saudi Arabia threatened to accept payment for its oil in currencies other than the US dollar. While the bill has been debated since 2000, Trump’s criticism of OPEC and his support for the bill in a 2011 book has revived such efforts. Qatar quit OPEC last year ostensibly because of the US threat. Last year, the Saudis sold about $356 bln of oil. If it did come to it, some of Saudis assets in America would also likely be sold. The Saudis own roughly $1 trillion of US assets, including around $160 bln in US Treasuries. |

Economic Events: United States, Week April 08 - Click to enlarge |

III

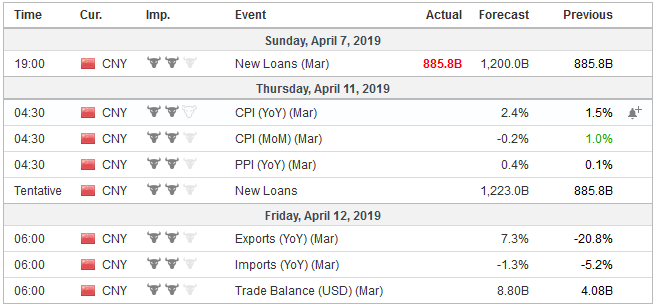

ChinaOur green shoots hypothesis requires the Chinese economy to find better traction. The PMIs were one piece of the puzzle, The next pieces may fall into place in the coming days. Aggregate lending should recover strongly if Chinese officials had what we called a Draghi moment, and have committed themselves to strengthen the economy and avoid the loss of face associated with economic weakness under the pressure of US tariffs and the 70th anniversary of the Revolution. More telling is at the next level of detail. A pro-growth policy may create room again for shadow banking. In February, shadow banking contracted, which is to say that new yuan loans exceeded aggregate financing. It ought not in March. Separately, price pressures likely picked-up. Consumer prices may have accelerated to 2.3% in March from 1.5% in February. The CPI finished last year at 1.9% but averaged 2.1%. Producer prices collapsed alongside energy prices in Q4 18 from a 3.3% year-over-year pace in October to 0.1% in January and February. Producer prices are expected to have edged higher in March. One of the startling transformations underway is the rise of the Chinese consumer. According to reports, in 2007 China’s consumption was 1/25 of the world. As of 2017, it was a tenth. While the rise of China is well known, we suspect the rise of India is not fully appreciated. India surpassed France last year to move into the sixth spot in world GDP. This year it will push past the UK to move into fifth (behind the US, China, Japan, and Germany). India’s month-long national elections begin at the end of the week ahead. Foreign investors have flocked to India this year, investing over $8 bln in equities and $500 mln in Indian bonds. |

Economic Events: China, Week April 08 - Click to enlarge |

Switzerland |

Economic Events: Switzerland, Week April 08 - Click to enlarge |

Tags: Brexit,China,ECB,Europe,Federal Reserve,newsletter,OIL,US