Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

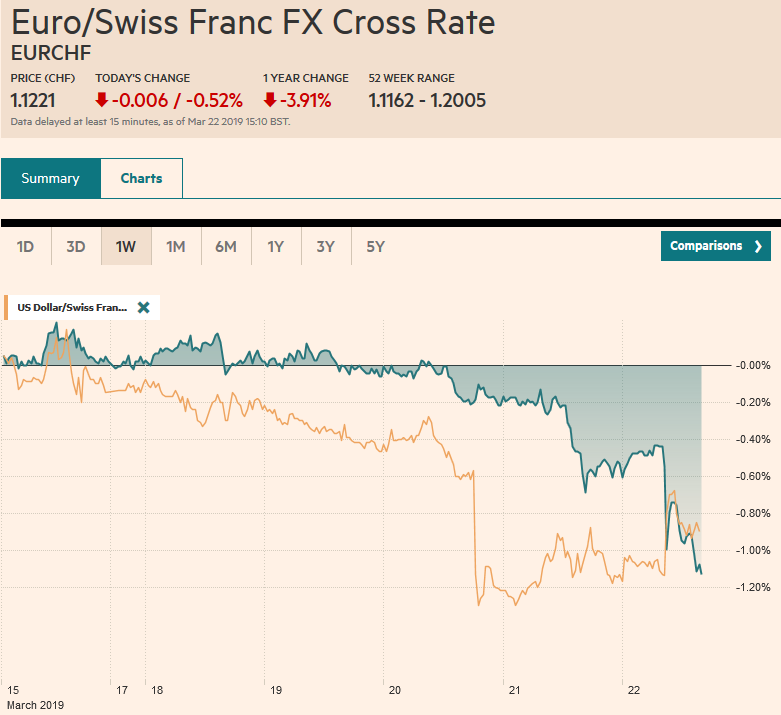

Swiss FrancThe Euro has fallen by 0.52% at 1.1221 |

EUR/CHF and USD/CHF, March 22(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The S&P 500 recovered from the post-FOMC reversal to close a new 5-month high yesterday, led by technology. Financials were the only main sector to retreat. The large equity markets in Asia, Japan, China, Australia, South Korea, and Taiwan all advanced. Europe’s Dow Jones Stoxx 600 reversed its initial gains and is nursing a small loss on the week. US shares were little changed but are being dragged down by the reversal in Europe. Benchmark 10-year yields are softer. Soft inflation data saw the 10-year JGB yield slip to nearly 2.5-year lows of minus 8.5 bp, while the yield on the 10-year Bund has fallen four basis points to almost zero after the dismal flash PMI. The US-German 10-year spread is virtually flat on the week. The 10-year US-Japan spread has narrowed by about four basis points. The dollar is mostly firmer, with the yen and sterling a little higher, and disappointing flash EMU PMI saw the euro slip below $1.13 after peaking after the Fed’s dovish surprise near $1.1450. The Scandis are the weakest as the recent advance is pared by profit-taking following Norway’s hike yesterday. The Mexican peso is the strongest currency in the world this week. Coming into today’s session, it is up about 1.5%. |

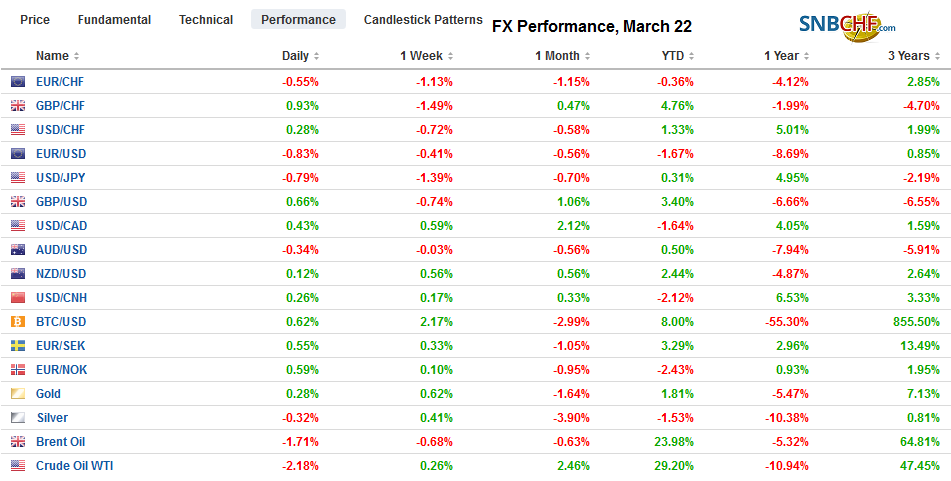

FX Performance, March 22 - Click to enlarge |

Asia Pacific

Japan’s February CPI disappointed. The headline rate was unchanged at 0.2% year-over-year. The core rate, in which the price of fresh food is excluded, slipped back to 0.7% from 0.8%. But even this is flattered by energy. When both fresh food and energy are excluded, price pressures were unchanged at 0.4%. At the same time, Japan’s flash manufacturing PMI was unchanged at 48.9. Finance Minister Aso reconfirmed the government’s intention to go forward with the sales tax increase in October.

Separately, we note that the MOF data shows foreign investors were heavy sellers of Japanese shares for the second consecutive week. The last time foreign investors were such heavy sellers as in mid-September and that time before that was the middle of last March. Although foreign investors are not good timers of Japanese shares, it appears these stepped up sales are seasonal, related to the end of the Japanese fiscal year and a half.

At the same time that US officials are playing down the likelihood of a near-term trade resolution with China, the US has signaled it intends to sell as many as five dozen f-16 fighter jets to Taiwan. This will provoke China and reverses a decision made by the Obama Administration in 2011. Many Americans are perturbed by China (and Russia’s) support for Maduro in Venezuela, as think Venezuela should be in the US sphere of influence. Yet selling high-grade weapons to what the US officially recognizes as a province of China (that should be reunited peacefully) is seen copacetic.

There that are two sets are expiring options that may mark the dollar’s range against the yen. There are about $3.3 bln in option between JPY110.90 and JPY111.05. Another set for around $2.7 bln struck between JPY110.40 and JPY110.65. The greenback looks to be finding a bid in the European morning near JPY110.50. The Australian dollar peaked yesterday near $0.7170 and today is struggling to hold above $0.7100. Expiring options may be important. There are a little more than A$600 mln at a $0.7110 strike and nearly A$520 at $0.7075. There is another large expiry at $0.7050, but it may not be in play.

Europe

When the ECB recently cut its growth forecast for this year to 1.1% from 1.7% and warned that the risk was to the downside, the pessimism seemed exaggerated. The flash PMI justifies the concern. Germany’s news was dismal, while France was dreadful.

The German flash manufacturing PMI fell to 44.7 from 47.6. The service PMI slipped to 54.9 from 55.3. The composite fell to 51.5 from 52.8. France’s manufacturing PMI fell to 49.8 from 51.5, and the service sector dropped to 48.7 from 50.2. The composite slumped to 48.7 from 50.4.

The flash manufacturing for EMU fell to 47.6 from 49.3. Economists had forecast a small increase. The service reading eased slightly to 52.7 from 52.8, in line with expectations. The composite eased to 51.3 from 51.9.

Meanwhile, the EC took steps yesterday to ensure that the UK will not crash out of the EU next week. Specifically, it gave May until April 12 for the UK to either endorse the agreement, which has been rejected overwhelmingly twice, or seek a longer extension. April 12 is not a random date. When May asked for an extension to the end of June, the UK showed little sensitivity to the European Parliament election at the end of May. April 12 is the last date for the UK to decide to participate in the election, which a longer extension will require. If perchance, a third vote on the Withdrawal Bill is allowed by the Speaker, and it passes, the EU will grant an extension to May 22 to formalize the decision. A petition calling for Article 50 to be revoked has gained over two million signatures.

With the help of disappointing US industrial output data a week ago and the dovish Fed, the euro recovered from the ECB-induced 18-month low just below $1.1180 to nearly $1.1450. It slipped below $1.13 today to retrace nearly 61.8% of those recovery gains. There is a $1.1300 option expiring today for about 570 mln euros and a $1.1350 strike for around 850 mln euros. Sterling bounced off $1.30 yesterday and ran out of steam a little above $1.3150. It has given back about half of those gains but still looks vulnerable.

America

Yesterday’s US Philly Fed survey and Leading Economic Indicators were better than expected, but there may be some disappointment with today’s flash PMI. However, existing home sales may have snapped a three-month slide in February as mortgage rates have begun easing. That said, the Fed’s statement essentially rendered Q1 data moot. It is looking past it, as apparently are investors.

The Trump Administration has signaled it will recognize the Golan Heights as Israeli territory. Israel has occupied this strategic area for more than 50 years. On one hand, it would seem to simply recognize the facts on the ground. On the other hand, it is fraught with risks as it would seem to set a dangerous precedent in overruling what is known as “UNSCR242”, which does not recognize territory taken in a war. That UN resolution is fundamental to the peace between Israel and Egypt and Jordan. It is part of the legal case against recognizing Russia’s territorial grabs on what it calls its “near abroad.” This may come back to haunt the US.

Canada reports January retail sales and February CPI. After a poor December (-0.5% excluding autos), retail sales are expected to have stabilized (0.1% ex-autos), while the headline may pick up to 0.4% from -0.1%. Seasonally, prices rise in Canada in February, but even the 0.6% headline increase expected would keep the year-over-year pace steady at 1.4%. The underlying measures are expected to be steady to lower. There does not look to be anything that will prevent the central bank from continuing to transition away from its tightening bias. The US dollar tested CAD1.34 yesterday and is consolidating a little below it now. The high for the month is near CAD1.3470, and that is the next immediate if the greenback can resurface above CAD1.34. The Dollar Index is making new highs for the week and is entering an important technical band between 96.70 and 97.00.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,EUR/CHF,FX Daily,newsletter,USD/CHF