Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

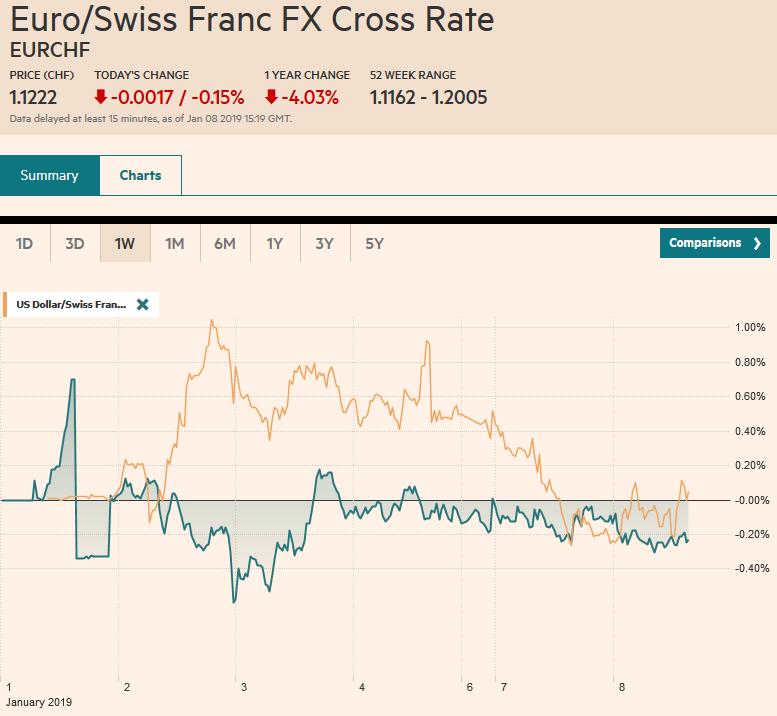

Swiss FrancThe Euro has fallen by 0.15% at 1.1222 |

EUR/CHF and USD/CHF, January 8(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The global capital markets remain calm after the surge in volatility seen over the last couple of weeks. Asian equities were mixed, with the Japanese, Australia and Indian shares gaining, but other large regional markets, like China, South Korea, and Taiwan fell. European equities are firmer. Benchmark bond have edged higher. The US dollar is steady to a little higher against most currencies. Oil is extending its rally into the seventh consecutive session. |

FX Performance, January 8 - Click to enlarge |

Asia Pacific

There appears to be growing optimism on the US-China trade conflict. Commerce Secretary Ross fed such ideas, suggesting that the basis for an agreement could be that China agrees to buy more US agriculture and energy and agree to longer-term structural reforms. In essence, this is similar to what happened with NAFTA. The Trump Administration criticized it as the worst deal ever and pulls out of the TPP, which would have modernized it, among other things. And the final product, which was heralded as the best agreement ever, was little more than the old NAFTA plus TPP and a new domestic content rule. China has already taken steps to appease the US, making intellectual property protections more robust, granting greater market access in finance, and buying more US soy (as recently as yesterday).

The Japanese benchmark 10-year bond yield rose back to almost zero after falling to minus five basis points last week. Japan auctioned a new 10-year bond today amid strong demand. The bid-cover rose to 4.04 from 3.82 at last month’s auction. The auction may have been aided by the fact that tomorrow the BOJ conducts its 5-10 year bond purchases.

Australia reported a smaller than expected trade surplus in November. The November surplus of A$1.93 bln follows a downward revision of the October surplus to A$2.01 bln (from A$2.31bln initially). Exports rose 1% on the month, while imports rose 2%.

With today’s gain through JPY109, the greenback has retraced the entire flash crash losses against the yen. However, it looks the dollar ran out of steam in early Europe. Support is pegged in the JPY108.50-JPY108.60 area. The Australian dollar has been unable to push above yesterday’s high (~$0.7150), which corresponds to a retracement (61.8%) of the decline from $0.7400 at the start of last month through the flash crash low (~$0.6740). Initial support is seen near $0.7100. All the currencies in Asia fell, but the Chinese yuan has fared the best. Many suspect that officials are keeping the currency steady to prevent a distraction during the trade talks. Rising oil prices may begin weighing on the Indian rupee. Disappointing Samsung profit news weighed on Korean shares and the won.

Europe

Germany has followed yesterday’s poor factory orders report with equally dismal industrial output figures today. The median forecast in the Bloomberg survey called for a 0.3% rise in November after a 0.5% decline in October. Instead, Germany reported a 1.9% decline in November output and a downward revision to the October series (-0.8%). If it wasn’t for the strong retail sales report yesterday (1.4% in November and October’s decline revised away), more economists would likely be looking for an economic contraction in Q4, which after the fall in GDP in Q3, would meet the rule of thumb definition for a recession in Europe’s biggest economy.

The Brexit drama continues, and the outlook becomes murkier. There are three new developments. First, the government is considering supporting an opposition measure that limits the Treasury’s ability to raise taxes in a no-deal divorce. Second, reports indicate that UK and EU officials have recently discussed the possibility of extended the Article 50 timeframe that has the UK leaving at the end of March. Third, London First has reportedly pulled back from supporting the deal May negotiated with the EU in favor of a second referendum, which polls suggest would be won by those who favor remaining in the EU.

Italy’s populist-nationalist government is being tested by the needs of Banco Carige. The Five Star Movement, ostensible the senior partner in the coalition but consistently being overshadowed by the junior partner the League, has been critical of government’s previous efforts to support banks, such as facilitating Intesa’s takeover of two trouble Veneto banks in 2017 and the aid to Monte dei Paschi. Carige is the last large lender in Italy that faces ECB calls to bolster its balance sheet. Salvini, the League leader and Deputy Prime Minister, seems to want to use state guarantee and, possibly a precautionary recapitalization to make the bank a more attractive acquisition for a large bank. Carige is under new and temporary administration, ordered by the ECB in an unprecedented move, and given a three-month mandate to reduce the balance sheet rises and find a possible partner.

The euro marginally took out yesterday’s high in early Asia but remained below last week’s high of nearly $1.15, the upper-end two-month range. It has traded down to almost $1.1430, just above the $1.1425 level, where about a 530 mln euro option expires today. There are 1.2 bln euros in struck at $1.15 that also expires today. The intraday technicals suggest additional albeit modest losses are likely in North America. Sterling tested $1.28 in late Asia. The high from New Year’s Eve was $1.2815. The short-term technical indicators suggest that the $1.2740-$1.2780 may contain most of the price action for the remainder of today’s session.

North America

The closure of the US government continues to interrupt data releases. It is also increasingly disruptive to employees and their families. Reports indicate that the IRS will issue tax refunds during the government shutdown. Private sector generated data, like the NFIB small business sentiment report (slipped to 104.4 in December from 104.8 in November, but better than the 103 economists were projecting) and data from the Department of Labor, like today’s JOLTS report on job openings, will be released. That includes the CPI figures at the end of the week, which come from the Bureau of Labor Statistics (BLS). President Trump will address the nation tonight and discuss the border wall, which is at the center of the fight that has led to the shutdown.

This week’s heavy schedule of Fed officials takes the day off today. Yesterday’s comments from Atlanta Fed’s Bostic were notable. Even though he is not a voting member of the FOMC this year, he is widely perceived as among the most dovish members. He now sees only one hike this year (the market is pricing in none), and he fully endorsed the continued unwinding of the Fed’s balance sheet.

The Bank of Canada meets tomorrow. Ideas that the Bank of Canada will continue to signal its intent to raise rates to neutral has helped lift the Canadian dollar. Recall that on New Year’s Eve, the US dollar traded near CAD1.3665, its best level of 2018. It has subsequently been sold-off, dipping below CAD1.3270 today. We had expected the CAD1.3330 area to offer support for the greenback, but it cut through there yesterday. The next important technical area is seen near CAD1.3220. As recently as last month, Bank of Canada officials still seemed intent on pushing the overnight rate to a more neutral setting, which it sees between 2.50% and 3.50%. It currently sits at 1.75%, after three hikes last year and two hikes in 2017. We expect the Bank of Canada to signal that it can be more patient about reaching a neutral setting. The dramatic reversal in the Canadian dollar appears corrective in nature, and the technical readings are getting stretched and the US-Canadian two-year differential, which the exchange rate seems sensitive, has begun moving back in favor the US.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$CAD,$EUR,$JPY,EUR/CHF,newsletter,USD/CHF