Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

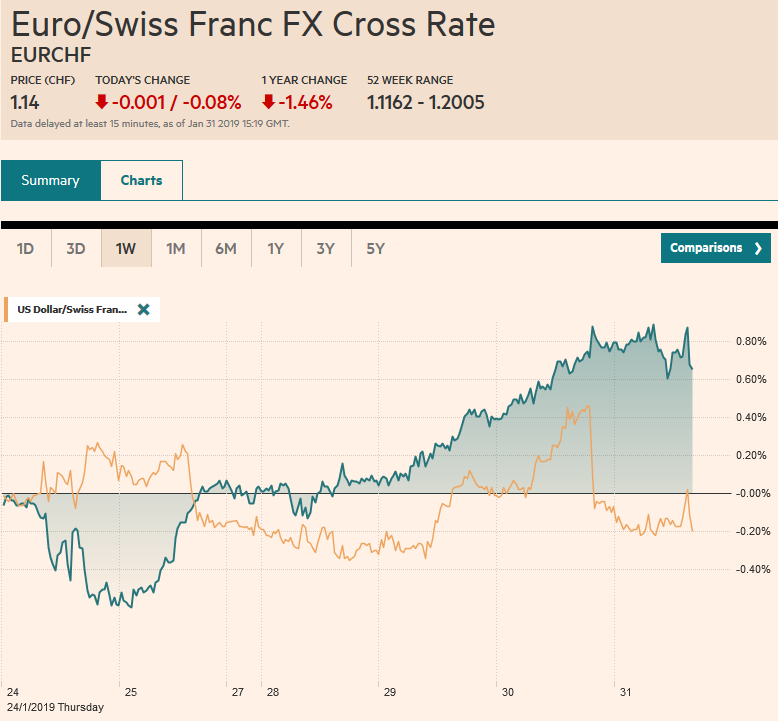

Swiss FrancThe Euro has fallen by 0.08% at 1.14 |

EUR/CHF and USD/CHF, January 31(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The Fed’s dovish tone and earnings news are the main drivers of the capital markets today, helping lift stocks, bonds, and currencies. Large equity markets in Asia, including Japan, Hong Kong, China’s CSI 300, India, and Indonesia, all rose more than 1%, putting the MSCI Asia Pacific Index in a good position to extend its rally for a fourth consecutive week. European shares are higher, but the gains are not as impressive, and the leading sectors are energy and healthcare. Financials, information technology, and communication sectors are laggards. Sovereign 10-year benchmarks are mostly 2-3 basis point lower, though Japan and Australia were flat. The dollar is seeing yesterday’s Fed-inspired losses extended against the major and most emerging market currencies. The euro, sterling, and the Canadian dollar are the weakest, while the yen and the Antipodean currencies are the strongest. |

FX Performance, January 31 - Click to enlarge |

Asia Pacific

Industrial output edged 0.1% lower in Japan in December, which was a smaller than expected decline. On a year-over-year basis, output in December was off 1.9%. In December 2017, it had risen by 3.2%. Japan’s economy contracted by 0.6% in Q3, and although it has stabilized in Q4, it has not covered fully recovered. The Q4 18 GDP estimate is not released until toward the middle of the month. A 0.3%-0.4% increase is likely.

China’s official PMIs did a little better than expected. The manufacturing PMI ticked up to 49.5 from 49.4, though many forecast another decline. It was helped by output and raw materials, while the decline in export orders slowed. The non-manufacturing PMI rose to 54.7 from 53.8 to stand at a four-month high. The rise in services offset the weaker construction reading. Tomorrow the Caixin PMIs will be reported. Caixin’s survey covers smaller and more private sector enterprises than the official measure.

Australia reported favorable terms of trade developments in Q4, but slower private credit expansion in December. In Q4 18, import prices rose 0.5%, while export price rose 4.4%. It is a key factor behind Australia’s improved trade balance, where the six-month average surplus is near record levels. On the other hand, private credit growth slowed to 0.2% in December, putting the year-over-year pace at 4.3%, the slowest in four years.

The dollar was turned back from JPY110 last week and posted an outside down day yesterday (trading on both sides of Tuesday’s range and closing below its low). There has been follow-through selling today, which pushed the greenback near JPY108.50. There is a nearly $440 mln option struck there that will be cut today, but stronger support is not seen until closer to JPY108.00. The $760 mln at a JPY109 option that also expires seems safe. The Australian dollar is firm, in narrow ranges, around yesterday’s highs, a little below $0.7300. It is up nearly a cent from last week’s close. We have argued that the dollar’s “approved” range against the Chinese yuan is CNY6.70 to CNY7.0. It slipped through the lower end briefly but snapped back to close onshore session above the floor.

Europe

Beginning on the aggregate level, EMU reported Q4 GDP rose 0.2% for a 1.2% year-over-year rate. In Q3, the regional economy also expanded by 0.2%, but then the year-over-year pace was 1.6%. Unemployment finished the year at 7.9%, matching the cyclical low set in November. At the end of 2017, EMU unemployment was at 8.6%. In a difficult year for growth, after posting 0.7% growth each quarter in 2018, but the continued decline in unemployment was an important bright spot. The labor market may be a chief consideration behind the ECB’s patient response to steep economic moderation.

Italy and Spain are the first EMU to report national GDP figures. Italy disappointed. It had already been tipped to contract against after the economy shrank by 0.1% in Q3. In Q4, growth fell by 0.2%. That unemployment slipped in December to 10.3% from 10.5% did not take the sting out of the disappointment, and the rate among 15-24-year olds firmed to 31.9% from 31.8%. Spain reported its Q4 GDP rose by 0.7% for a 2.4% year-over-year pace, which will likely prove among the strongest in Europe. Separately, Spain reported that January CPI eased to 1.0% from 1.2%.

French CPI in January moderated to 1.4% from 1.9%. This follows German news yesterday that its January was unchanged at 1.7%. Germany reported a simply atrocious retail sales figures for December. The 4.3% drop is the largest drop in 11 years. The median Bloomberg forecast was for a 0.6% decline after a 1.6% rise in November (initially 1.4% increase). Germany Q4 GDP is due out near the middle of the month. It had contracted 0.2% in Q3, and the central bank suggests it narrowly missed posting back-to-back contractions.

The euro has mostly traded between $1.13 and$1.15. Twice this month there was a break, and both times the euro quickly snapped back into the range. The third attempt to breakout is being seen today. The euro reached near $1.1515 in late Asia but has come back offered in the European morning. Initial support may be seen near $1.1450. Sterling is firm, marginally extending yesterday’s gain. Brexit uncertainty has not been lifted by any means, but beside posturing, little may happen until May returns to the House of Commons in the middle of the February to confirm there have been no fresh compromises by the EC over the backstop.

United States

The Fed’s independence is being challenged on two fronts. The first is the President’s willingness to eschew recent tradition and berate the central bank publically. The second is investment capital’s willingness to go on strike (pull its wealth away from risk-taking activity) tightening financial conditions and forcing the shift in the policy stance. Many observers see the FOMC meeting as having capitulated to one or both of these challenges. In the past, Fed pauses marked the end of a cycle, but it need not be that way. The Fed’s baseline economic view has not changed.

Some of the cross-currents Powell mentioned will ease in the coming weeks. Brexit and US-Chinese trade issues will be clearer. The fight over funding for the US government and the debt ceiling (~early March) may also be resolved. It may take a bit longer to see whether Chinese stimulative measures will bear fruit and if the European economy can find better traction. While the March updated forecasts are six-weeks away, based on what we know now, the median dot is still likely to anticipate scope for additional normalization of rates. How to best remove itself from the market drivers and as a political lightning rod, so that it can continue to do its job, may have required the Fed to change its rhetoric while maintaining its path, patiently and flexibly. The balance sheet may not be on automatic pilot, but the Fed has not altered its course. It acknowledged that it can be a policy tool if needed, but is not now.

We have been critical of the Fed in the past for seeming to over-promise and under-deliver. To the extent that the Fed is being criticized today it is for over-delivering. We suspect it is more complicated than that and emphasize the differences between the rhetoric and the actions. The Fed had long signaled that 2018 was the peak pace of Fed normalization. It had anticipated three hikes this year after four in 2018 and reduced it to two. Press conferences after every meeting give it flexibility. The mixed data and what Powell called cross-currents and the steady inflation readings allow the Fed to be patient, flexible, and data dependent. We expect the data will allow the Fed to raise rates again.

The Canadian dollar lagged behind the other dollar-bloc currencies, but its two -day gain of 1% beats the other majors. It reports November GDP. It is expected to have fallen after a 0.3% expansion in October. The more troubling reading will be the year-over-year pace, which is forecast to slow to 1.6% (from 2.2%). This would be the slowest pace since late 2016. It may reinforce the sense that the central bank is on the sidelines. The US dollar slumped to new lows for the year and three-month lows against the Canadian dollar near CAD1.3120. The US dollar needs to regain CAD1.3180, and ideally, CAD1.3200 to begin repairing the technical damage.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: $AUD,$CAD $GBP,$CNY,$EUR,$JPY,EUR/CHF,FX Daily,newsletter,USD/CHF