Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

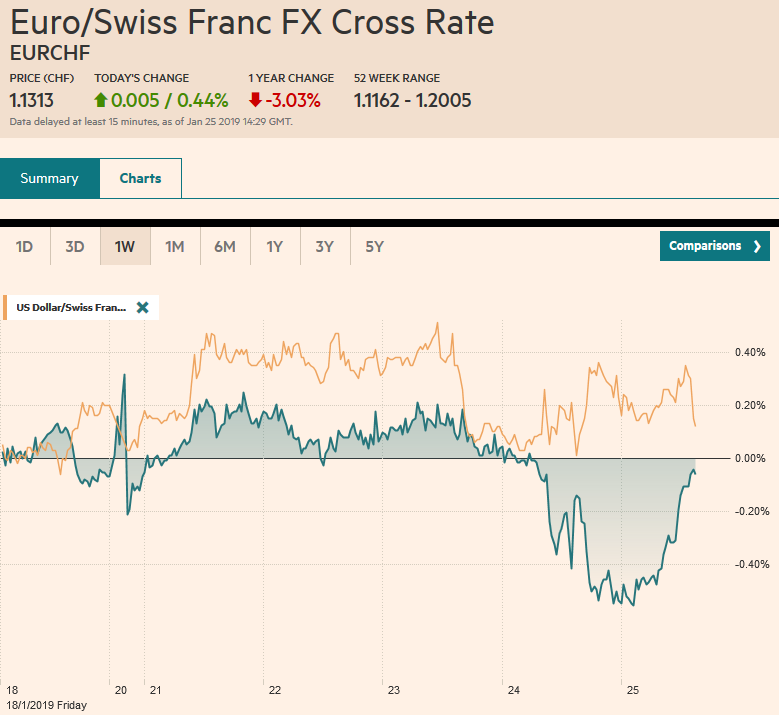

Swiss FrancThe Euro has risen by 0.44% at 1.1313 |

EUR/CHF and USD/CHF, January 25(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The US dollar is paring yesterday’s gains against most of the major and emerging market currencies. Sterling pushed above $1.31, an 11-week high on news that the DUP would support Prime Minister’s Plan B that calls for limits on the backstop with Ireland, something that the EC and Ireland have indicated are not on the table. Global equities are finishing the week on a firm note. Nearly all the markets but India rose in Asia while in Europe, the Dow Jones Stoxx 600 gapped higher, as it did a week ago, to see its best level since December 4. If modest gains can be retained today, the benchmark will close higher for the fourth consecutive week. The S&P 500 comes into today off about 1% for the week, threatening to end its three-week advance. |

FX Performance, January 25 - Click to enlarge |

Asia Pacific

Japan reported Tokyo CPI figures for January, which are reported a month ahead of the national figures and is often seen as a lead indicator. Headline CPI rose by 0.4%, twice the median forecasts and follows the upward revision in the December series to 0.4% from 0.3%. The core rate, which excludes fresh food, rose 1.1% compared with 0.9% previously. It was expected to be unchanged. Although this was an upside surprise, the market did not seem to react much. In the middle of the week, the BOJ has shaved its growth and inflation forecasts.

India’s high court upheld a law that in essence prevents business founders from regaining control of the failed business. This is seen helping banks resolve the bad loan burden, which is estimated around $210 bln, according to reports. There is an important case from a steel company coming up shortly for which today’s ruling may impact.

China announced a new facility to jump-start credit expansion. It allows Chinese banks to swap perpetual bonds for central bank bills. Perpetual bonds with ratings of at least AA can be used as collateral, as well, for borrowing from other lending programs at the central bank. Approval was given to the Bank of China in the middle of January for a CNY40 bln (~$5.9 bln) perpetual bond offering. Perpetual bonds sound like a way forward but the proceeds count as tier one capital (equity), and a capital buffer must be established to cushion losses.

The US dollar is virtually unchanged on the week against the Japanese yen. It has traded in a little less than a one yen range all week. It remains spitting distance of JPY110.00, where a $1.2 bln option expires today. The dollar has not traded above there so far this month. Initial support is seen around JPY109.40. The Australian dollar stabilized after slipping to new lows for the move near $0.7075. Its nearly 1% decline this week leads the majors, as the market prices in a greater chance of a rate cut. Nearby resistance is seen in the $0.7130 area. The Chinese yuan strengthened by 0.35% today, the most in a couple of weeks. Some linked the yuan’s gains to reports that US Treasury Secretary Mnuchin said the currency was part of the trade talks. The US can push for implementation of G20 best practices of letting the markets determine exchange rates, more transparency of intervention, and the like, but it will be hard pressed to make a case that the yuan is significantly undervalued.

Europe

For the first time, the ECB altered its risk assessment between staff updates and took us and many others by surprise. This may reflect a greater sense of urgency, or it may also have been dictated by the need to remain credible in the face of the poor PMIs, downward revisions to growth forecasts, and as Draghi noted, international uncertainty. The hawkish members appear to have strategically retreated ostensibly to be in a better position to shape the policy response. The evolution of Draghi’s references a new TLTRO shows that it is becoming more salient. An announcement is likely at the next meeting in early March, even if not all the details. Draghi also seemed to validate the market pushing the first hike into 2020.

Following news earlier this week that the German manufacturing PMI fell below the 50 boom/bust level for the first time in four years, investors learned today that the IFO survey fell for a fifth month in January. The overall reading fell to 99.1 from 101 in December. The drop in the expectations component (94.2 from 97.3) warns of an erosion in confidence. The current assessment slipped to 104.3 from 104.9 (revised from 104.7). The German government reportedly will cut its growth forecast shortly.

There is a certain optimism over Brexit now that lifted sterling above $1.31 earlier today, a level not seen since November 8. However, May’s Plan B, even with DUP support, seems like a non-starter. The idea of a backstop was to be in place in case a deal was not struck. Having a time limit on it defeats the purpose and shifts the burden to the EC from the UK. The UK could play obstructionist until the time limit expires. The EC and Ireland have already rejected it. May might be more support for her bill however as it may be seen by some Brexiters to be preferable to a referendum that could see Remain win or an election that could see Labour win. Even if May’s bills wins, it is not clear how this forwards the negotiations with the EC.

The euro slipped through $1.13 yesterday but did not close below it and has edged higher today. Some chunky options that are expiring today and could impact trading. There is a 1.3 bln euro option at $1.13 and nearly 660 mln euros at $1.1325. A bit further up, in the $1.1350-$1.1360 area, are options for about 1.9 bln euros. These may very well mark today’s range. Sterling has pulled back after reaching $1.3130 in Asia. Support is seen now around $1.3050. Sterling is the strongest of the majors this week, gaining almost 1.6% (@$1.3070) and has extended its advance for a sixth consecutive week.

North America

The ECB and Draghi overshadowed a series US data that suggests the economy is off to a better start than feared. First, weekly initial jobless claims and continuing claims fell to new cyclical lows. These are state filings only. Federal filings, which pick up the impact of the partial government shutdown, rose by about 15k to 25.4k. The flash PMI was also better than expected. The manufacturing component rose to 54.9 from 53.8. Economists had forecast a decline. The services PMI did decline (54.2 vs. 54.4) but less than expected. The composite edged up to 54.5 from 54.4. These are the not reading one would expect for a recession-bound economy. Even the 0.1% decline in the Leading Economic Indicators, which matched expectations, is still up 3.1% at an annualized pace over the past six months, in effect returning to where it was before the fiscal stimulus.

US Commerce Secretary Ross indicated the China and the US are “miles and miles” apart but tacked on that both sides want a deal to take some of the sting away from the assessment. Treasury Secretary Mnuchin played down the trade hawk’s view and said the positions were narrowing. Early next week there will reportedly be the preliminary talks to prepare for Liu He and Lighthizer face-to-face. The Chinese request for a preparatory meeting was apparently turned down for this past week. Economic adviser Kudlow said that the negotiations with Lighthizer are critical.

The US dollar is snapping a three-week slide against the Canadian dollar. The US dollar briefly traded above its 20-day moving average against the Canadian dollar for the first time since January 3. It failed to close above it (~CAD1.3365) and is a bit heavier today. Initial support is seen near CAD1.3300. Meanwhile, if the dollar does not close above MXN19.09, its losing streak will be extended for a ninth consecutive week. The US dollar has not risen on a weekly basis against the peso since the week ending November 23. The high yield, the surprisingly orthodox budget of the new government, and the recovery in emerging markets, in general, have underpinned the peso.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: $AUD,$CAD $GBP,$EUR,$JPY,EUR/CHF,EUR/GBP,FX Daily,MXN,newsletter,USD/CHF