Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

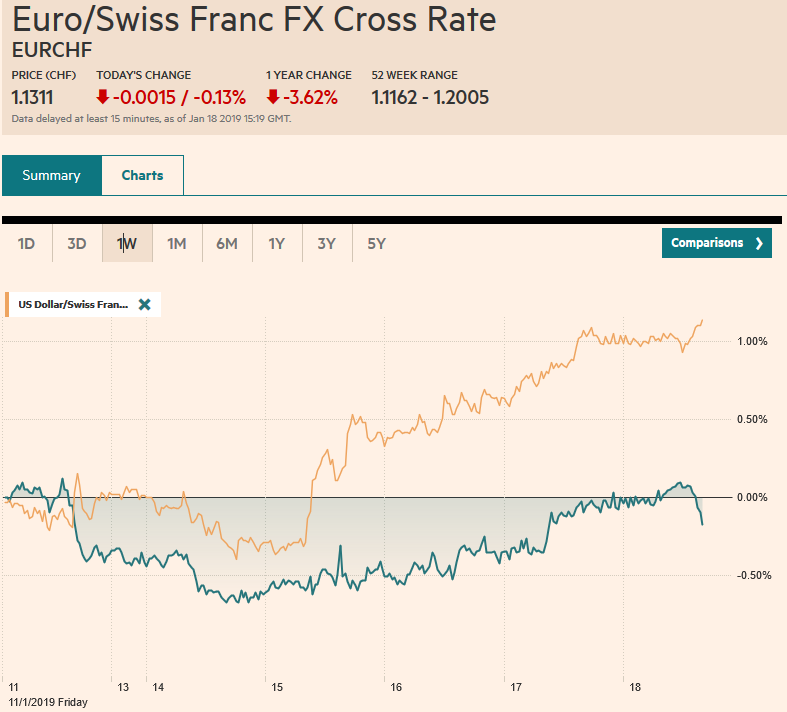

Swiss FrancThe Euro has fallen by 0.13% at 1.1311 |

EUR/CHF and USD/CHF, January 18(see more posts on EUR/CHF and USD/CHF, ) - Click to enlarge |

FX RatesOverview: Sentiment has improved since the volatility last month spooked investors and, perhaps, some policymakers. Global equities are rallying. The Shanghai Composite and the Nikkei are at their best levels in almost a month, while the Dow Jones Stoxx 600 is at its best level since early December, gapping above a downtrend in place since late last September. The S&P 500 is expected to open higher after yesterday’s advance saw it reach the midpoint between last September’s record high and the late December low. Core bond yields are firmer, with the US 10-year yield at its highest level of the year (~2.77%). European peripheral yields are lower, led by Italy, despite Fitch cutting Carige ratings to CCC yesterday and the government passed by decree its controversial measure to lower the pension age, The dollar is mixed but mostly a little firmer. |

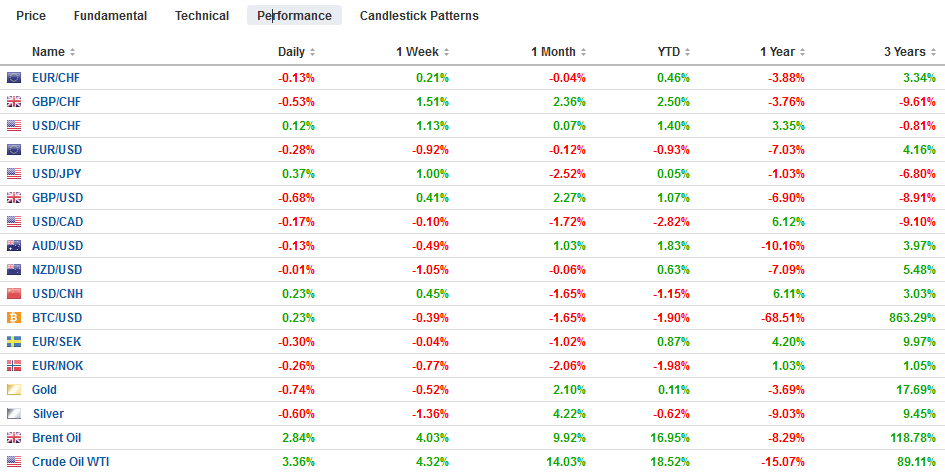

FX Performance, January 18 - Click to enlarge |

Asia Pacific

The Wall Street Journal reported of a debate in the Trump Administration with Mnuchin proposing some concession on tariffs to enhance chances of structural concessions from China. Lighthizer, reportedly, pushed back. The Treasury denied Mnuchin made such recommendations and a senior Administration official who reportedly attended the meeting denied there was a discussion to lift tariffs. Earlier this week and via a Senator, reports indicated that recent talks did not produce much. It seems fair to assume that before China’s Vice Premier visits the US at the end of the month, the Administration’s strategy and position is discussed. While Trump says he wants a deal, he did reject a deal less than a year ago, before the tariffs, negotiated by Mnuchin that would have boosted Chinese purchases of US goods. Trump may have changed his mind, but it seems highly doubtful that tariffs will be lifted unilaterally. The kernel of truth may be that the small globalist wing and the America First wing in the Administration continue to be at odds.

Japan’s headline inflation in December fell to 0.3% from 0.8% in November, in line with expectations. The core rate, which only excludes fresh food, and is the targeted rate by the BOJ eased to 0.7% from 0.9%. Excluding fresh food and energy, Japanese inflation was unchanged at 0.3%. This is where it stood at the end of 2017 too. At the end of 2016, it was at 0.1%. There is some speculation that the BOJ may shave its inflation forecasts at next week’s meeting. Separately, weekly data from the Ministry of Finance shows that Japanese investors took advantage of the strong yen to step up their purchases of foreign bonds. Last week, JPY2.2 trillion of foreign bonds was bought (~$20 bln), the most since last September (~JPY2.3 trillion), which itself was the most in a couple of years.

The dollar is poised to snap a four-week slide against the Japanese yen and around JPY109.50, it is up just shy of 1% for the week. The high this year has been about JPY109.80. Some of the dollar buying today may have been spurred by the options market, where large expiring options were thought to have been out of the money are now in the money. There is a $2.2 bln option struck at JPY109, and almost $930 mln struck at JPY109.10 that roll-off today. The JPY110.00-JPY110.30 offer the next important technical area. The Australian dollar continues to straddle the $0.7200 area but recovered from yesterday’s dip below $0.7150. Both the Australian and New Zealand dollar have been confined to yesterday’s ranges. The dollar’s four-week losing streak against the Chinese yuan appears to have also been broken. On the week, it rose a little less than 0.2%.

Europe

Prime Minister May is to deliver “Plan B” on Monday to the House of Commons, and a vote is expected by the end of the month. Although Chancellor of the Exchequer Hammond reportedly indicated that a no-deal Brexit is not likely, May refused to rule it out, saying it is not within the government’s power to do so. Preparations continue. The DUP from Northern Ireland was the key to May’s survival of the vote of confidence this week. It said it could support a Norway-style agreement to stay in the customs union if it meant removing the threat of an indefinite backstop. May rejected it. A YouGov poll showed that the Remains now at a post-2016 high.

The eurozone’s current account surplus fell to 20.3 bln euros in November from a revised 26.8 bln surplus in October (initially 23 bln euros). The 2018 average through November was 29.5 bln euros, virtually unchanged from the 2017 average of 30.2 bln. Still, the November surplus is the smallest since April 2017and reflects the more recent deterioration. In the three months through November, the average surplus was 22.8 bln euros compared with an average of 37.1 bln euros in the same year-ago period. We suspect the main driver has been the slowing of the world economy rather than a structural shift in the euro area.

For the third session, the euro is confined to narrow ranges of around a quarter of a cent on either side of $1.14, which itself is a broader $1.13-$1.15 range that has limited the price action, for the most part, since the second half of last October. Large options are expiring today. There are 2.7 bln euros in options between $1.1400 and $1.1405 and another 1.3 bln euro between $1.1420 and $1.1425. Sterling met our $1.30 target late yesterday, its best level since the middle of last November, before backing off today on what seems to be a light bout of profit-taking. The risk is that sterling retraces a bit more of the rally from the vote-of-confidence low near $1.2670. Technical retracements targets are about $1.2875 and then $1.2835. Note that there are aboutGBP500 mln in option struck $1.2950 and $1.2960 that expire today. One could not tell by looking at the Swedish krona that it has been unable cobble together a new government since the election last September until today. Lofven has secured another four-year term. The krona is up about 0.25% against the dollar today, making it the strongest of the majors at the time of this note.

North America

Rather than the suspect press report that there is a debate in the Trump Administration about the US unilaterally lifting tariffs against China, an alternative explanation for the improved sentiment notes constructive US data. Weekly initial jobless claims fell more than expected and remain near cyclical lows, which is not something one would expect if the US were recession-bound. Also, the Philadelphia Fed survey was stronger than expected, nearly double (17) the median forecast in the Bloomberg survey (9). Today US industrial production and manufacturing output will be reported. While the former may slow (~0.2% from 0.6% in November), the latter is expected to have risen by 0.3% after a flat showing in November.

The Canadian dollar is steady after falling to eight-day lows yesterday. The Loonie is off to a strong start to the year, but it seems to be exaggerated. ADP estimated yesterday that Canada lost about 13k jobs in December (though it did revise its November estimate to 74k from 39k) citing losses in trade and transportation sectors. Today Canada reports December CPI figures. Due to the base effect, a 0.4% decline in the headline pace that is expected will keep the year-over-year rate at 1.7%. The three core rates that are published are also expected to be unchanged at 1.9%. The technical tone of the Canadian dollar is turning, and the US two-year premium over Canada has begun widening, which is also supportive for the greenback. We look for a test on CAD1.3365 over the next couple of weeks.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,$AUD,$CAD,$CNY,$EUR,$JPY,EUR/CHF and USD/CHF,newsletter,SEK