Keith Weiner

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaFacebookAmazonGoogle +

For the first time since we began publishing this Report, it is a day late. We apologize. Keith has just returned Saturday from two months on the road.

Unlike the rest of the world, we define inflation as monetary counterfeiting. We do not put the emphasis on quantity (and the dollar is not money, it’s a currency). We focus on the quality. An awful lot of our monetary counterfeiting occurs to fuel consumption spending. And much of this, certainly a very visible part of it, is government borrowing to pay for the welfare state that is not supported by taxation.

There are four components to our definition of legitimate credit:

- The lender knows that he is lending

- The lender agrees to lend

- The borrower has the means to repay

- The borrower has the intent to repay

It is counterfeit credit, if one or more of these criteria are breached.

If the government cannot pay current expenses out of tax revenues, then obviously it can never amortize its debt. So this shows the Treasury bond itself to be counterfeit credit. But let’s consider the dollar.

The funny thing about the dollar, it is universally regarded to be money. This is no mere dispute over definitions or semantics. It means that people who hold dollars deny being lenders! They do not believe and would not agree if you told them that they are creditors, financing profligate welfare-state spending. The dollar is base money, end of story. Well perhaps not end of story, if push comes to shove. Yeah, the Fed accounts for it as a liability but since it’s not repayable, it’s not really a liability. And so on.

So the lenders cannot know that they are lending, as a definition neatly forecloses on this knowledge. Or admitting to having this knowledge.

Anyways, borrowing to finance welfare spending is covered under #3. Let’s consider a different case. It is when corporations sell a bond to finance a capital asset. Perhaps they are acquiring a profitable company. Or maybe they are building a new plant.

Corporate bonds today are often non-amortizing. They pay interest only, with a balloon payment at the end to return the principle. How do they plan to pay? Either they must sell more shares (raise equity), or else they must sell another bond to repay the first bond.

Obviously, this exposes investors to the risk that the market will not let the company sell equity or debt at the time when the bond matures. From where we sit today, after nearly a decade of endless bidding up of assets, this seems a remote risk. But 10 years ago, the market was closed and many companies were forced into bankruptcy as they were unable to pay debts when due. Including the acquirer of Keith’s previous company, Nortel Networks.

So this leads to a question: why is it this way? Obviously, a non-amortizing bond puts less pressure on borrowers’ cash flow. The borrower is not paying the principle. So of course borrowers prefer it. But why do investors tolerate this?

One reason is that it’s easier. The principle is not dribbled back. Picture an institutional investor who deployed $10,000,000 in a bond. It has the entire ten mill working for the entire 10-year maturity. If the bond amortized principle, the fund manager would have to work harder to deploy the principle that came back every payment period.

And of course, in a chronically-falling interest rate environment, if you buy a bond that’s yielding 6%, then you do not want to get some of it back and be forced to start buying bonds at 5.5%, then 5%, then 4%, etc. You want to lock the full ten million for 6% for the full 10-year maturity.

Does a non-amortizing bond signal the issuer’s breach of #4, lack of intent to repay?

This leads Monetary Metals to a dilemma, as we bring gold bonds. A future gold standard, if we are to have one, must be based on monetary integrity. If we are not to have integrity, if we don’t choose to have it, then we have no need of gold. Irredeemable paper serves the purposes of monetary counterfeiting just fine…

So the question we face is this. Should gold bonds be amortizing? If they’re borrowing to finance construction of a mine with a 20-year expected life, should the bond be amortized in 10 years (or less)? Or if they’re financing a vault or a refinery or a jewelry production line, should the bond be amortized in no more time than the business plan projects profits for the asset?

Or should the first gold bonds be designed meet investor (i.e. institutional investor) expectations? Expectations that were set in today’s world.

There is one other investor advantage to an amortizing bond. It reduces the exposure to the risk of default. Any principal that is repaid, is not lost if the issuer declares bankruptcy.

We would love your feedback. Please contact us with any thoughts you have to share. Thank you.

Supply and Demand Fundamentals

This week, the price of gold was down ten bucks and silver four cents.

Someone on Twitter demanded if we didn’t find it odd that the biggest sovereign debt bubble has managed to inflate a bubble in virtually every asset price except for gold. Given that he went on to assert there is a bubble in paper gold claims, he is trying to say that gold has to be suppressed. Otherwise its price would be much higher. We won’t reiterate here the proof that this conspiracy theory is false.

Instead, we want to address two points. One, the term bubble is used quite flexibly. Does it mean the price of something is too high? For example, the S&P Index at nearly 3000. Or does it mean there is too much quantity of something, e.g. debt. Or that something is being done to unhealthy degree, e.g. sending non-students off to university to get degrees that will not increase their employability? One should use each word with care and precision. Otherwise ambiguity permits one to migrate freely between different concepts.

Clearly, this guy is jealous that the prices of other assets have gone up, making other speculators rich. But the price of gold has not, thus not making him rich. Instead of admitting he was wrong to believe the gold-to-$10,000 story, he blames the world. Also, he is wrong about something else. The price of oil has not exactly gone up. Or real estate in many non-trendy locations.

But that’s not quite our point. We think it’s important to understand that prices of things do not go up in an automatic way, as many take the quantity theory of money to imply. Prices go up when buyers are aggressive and sellers are reluctant. Whether or not an increase in the quantity of the counterfeit paper that is yet called money causes this, we leave to another day. But even if so, this would obviously be a two-step process. Step one is increase quantity. Step two is when many people take their surplus free cash and trade it for assets such as gold bars.

And even that is not quite right. There is no such thing as a helicopter drop of free cash. There is lending, perhaps at near-zero interest (in the US—in some countries, below zero). Would you borrow money to buy gold? You can, you know. It’s called margin. You can buy GLD with 2:1 leverage, or a gold futures contract with 10:1.

But people don’t do this casually, as leverage increases risk. They do this only for assets that are going up. We have already established that gold is used by people like our Twitter interlocutor for one thing. For betting on its price. We don’t know his portfolio, but we would bet that even he is not betting with leverage right now. It’s much easier—and less risky—to complain that others aren’t betting with leverage. I.e. driving the price up so he can sell and make profits in dollars.

He does not conclude that every asset is like the planchette of a Ouija board, moving around as speculators shift their preference. And instead of concluding that the price of gold is really just the mirror of the price of the dollar, which is strong right now for readily visible reasons, he feels hurt.

And he does not think through that if gold were useful only when it went up, then it would be useless for any other purpose (one of our main criticisms of bitcoin), and hence its price would move all over the place. Including downwards and sideways. And only begin moving up again, when all the frustrated speculators like him finally capitulated and sold off their gold. Then, unloved and neglected—not breathlessly anticipated by a whole sector full of self-declared contrarians—it would finally begin a stealth bull market once again.

Of course, the whole point of our extended bout of snark today is that this is not so! Gold does have uses other than betting for dollars.

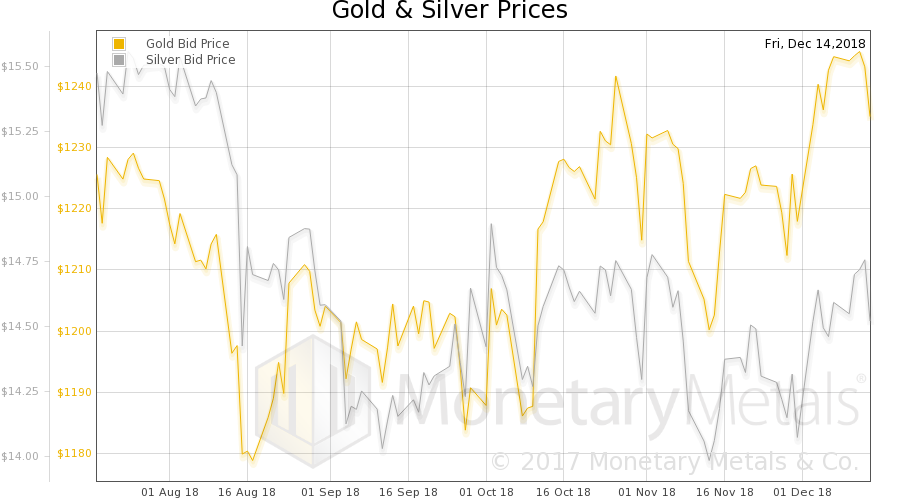

Gold and Silver PricesGold is the once and future unit of finance. There is a way to analyse the likely price direction of gold. It’s not to buy into stories, even true ones much less manipulation conspiracies. It is to look at the basis, the spread between spot and future prices. So let’s look at the only true picture of the supply and demand fundamentals of gold and silver. But, first, here is the chart of the prices of gold and silver. |

Gold and Silver Prices(see more posts on gold price, silver price, ) - Click to enlarge |

Gold:Silver RatioNext, this is a graph of the gold price measured in silver, otherwise known as the gold to silver ratio (see here for an explanation of bid and offer prices for the ratio). It fell this week. |

Gold:Silver Ratio(see more posts on gold silver ratio, ) - Click to enlarge |

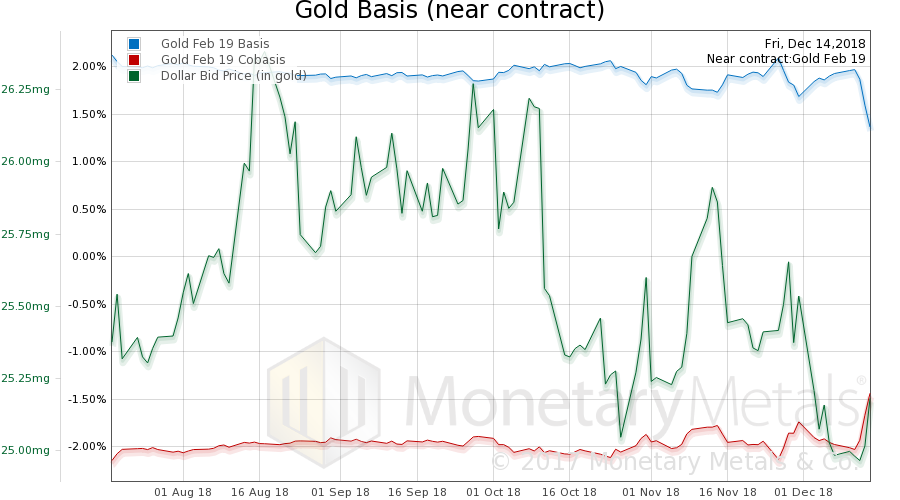

Gold Basis and Co-basis and the Dollar PriceHere is the gold graph showing gold basis, cobasis and the price of the dollar in terms of gold price. As the price of the dollar rises (inverse of the price of gold, which fell), we see a rise in the scarcity of metal (i.e. cobasis). The Monetary Metals Gold Fundamental Price fell another $5 this week to $1,288. |

Gold Basis and Co-basis and the Dollar Price(see more posts on dollar price, gold basis, Gold co-basis, ) - Click to enlarge |

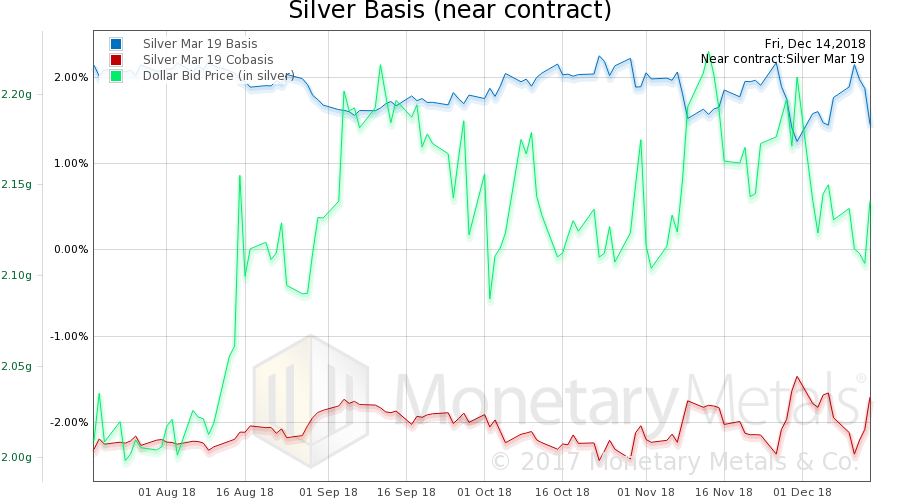

Silver Basis and Co-basis and the Dollar PriceNow let’s look at silver. In silver, we see the same pattern. And unlike in gold, the Monetary Metals Silver Fundamental Price rose 8 cents, to $15.14. © 2018 Monetary Metals |

Silver Basis and Co-basis and the Dollar Price(see more posts on dollar price, silver basis, Silver co-basis, ) - Click to enlarge |

Full story here Are you the author?

Tags: Basic Reports,dollar price,gold basis,Gold co-basis,gold price,gold silver ratio,inflation,newsletter,silver basis,Silver co-basis,silver price