Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

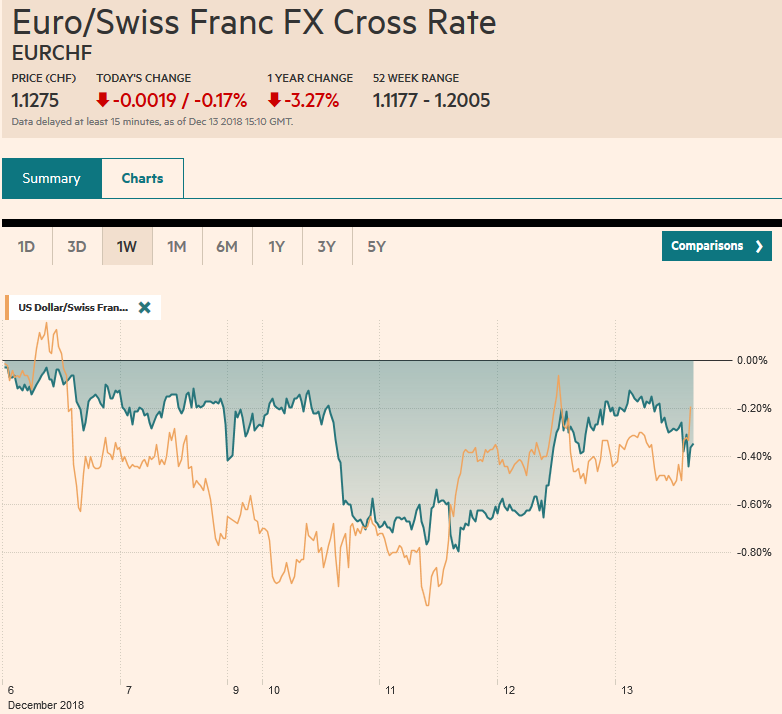

Swiss FrancThe Euro has fallen by 0.17% at 1.1275 |

EUR/CHF and USD/CHF, December 13(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: There is a sense of optimism among investors today that may be tested as the session progresses. News that China may reconsider its “Made in China 2025” initiative as an apparent concession to the US while reports suggest it has bought 1.5-2.0 mln tons of soy is easing trade tension fears. UK Prime Minister May survived a vote of confidence within her party and sterling’s recovery has been extended. Italy offers a 2.04% budget deficit to the EU. The improvement from the initial 2.4% projection may be enough to prevent excessive deficit procedures. The 10-year Italian bond yield is at three-month lows today slipping below 2.90%. Equities in the Asia Pacific region gained for the first back-to-back advance this month. European shares are struggling to extend its two-day advance. The dollar softer against most major and emerging market currencies. |

FX Performance, December 13 - Click to enlarge |

Asia Pacific

Now that the momentum of US tariffs against has been broken, Chinese officials appear willing to make compromises to try to avoid their resumption next March when the 90-day freeze expires. The 1.5-2.0 mln ton purchase of US soy is symbolic. After rising about 10 cents over the past couple of sessions to about $9.20 a bushel, January soy is trading a little softer today. Reports suggest Chinese officials are considering pushing out the “Made in China 2025” initiative out another decade, while it has already de-emphasized it. China also appears to be moving to unwind the retaliatory tariff on auto exports from the US. More concessions are likely from next week’s annual economic policy meeting.

Japan’s quarterly Tankan survey will be reported tomorrow. Although the economy seems to be recovering from the Q3 contraction, the survey is not expected to show much improvement. That said, sentiment among the large manufacturing has softened in each of the first three quarters of the year. The Bank of Japan meets at the end of next week and is widely expected to leave policy settings unchanged.

The dollar remains firm against the yen, though in tight ranges. It is knocking on the JPY113.50 level. It has not traded below JPY113 today. Almost $1.2 bln in JPY113.00-10 options expire today, and another option at JPY113.30 (~$465 mln) will also be cut. The recovery in equities and bond yields has helped lift the greenback to eight-day highs. The Australian dollar continues to recoup the losses that had pushed it to near $0.7170 at the beginning of the week to approach $0.7250 today. The first retracement objective of this month’s slide that began near $0.7400 is found closer to $0.7260 today. Easing trade tensions and the stronger risk appetites appear to have helped Aussie.

Europe

UK Prime Minister May lost about a third of the Tory vote but survived the confidence vote. She has gone to Brussels to plead her case to the European Council, seeking some concessions that will strengthen her hand at home. After exhaustive negotiations and a more-than-500-page agreement that all the heads of state have approved, the EC is reluctant to re-open talks. Still, reportedly the EC is willing to provide some additional assurances that even if the Irish border backstop comes into effect, it would continue to negotiate with the UK. This would be meant to ease British fears that the backstop would be permanent.

It is not clear how much the broader situation has changed from the start of the week. May remains Prime Minister, and she has an agreement with the EC that will not pass Parliament. When May decided to pull the vote that had been planned for December 11, the looming defeat was estimated to have been by a margin of more than 100. Additional assurances from the EC are unlikely to be particularly persuasive, we suspect.

Draghi is center stage today. There are several elements of the ECB decision:

- Nearly everyone expects Draghi to confirm that asset purchases will end this month.

- The monetary policy setting remains extraordinarily accommodative and repeating the forward guidance that rates will not be lifted until after next summer comes at little cost. The market has already largely pushed the hike from late 2019 into 2020.

- The new forecasts are likely to shave growth and inflation projections next year. The 2020 forecasts are likely to be less impacted, but this is something to keep an eye on next year. For the first time, the 2021 projection will be presented.

- The ECB’s risk assessment will likely remain balanced. The improvement in the labor market and wages continue to be the source of optimism despite weaker than anticipated economic performance

- Many investors will be looking for insight into the reinvestment process. This is mostly a technical discussion of how the maturing issues will be reinvested. The ECB may introduce greater flexibility such as expanding the maximum period between when an issue matures and when the proceeds need to be reinvested. There is much interest in whether the ECB will encourage an Operation Twist-type of approach where longer-term maturities would be emphasized.

Three other EMEA central banks met today: Turkey, Switzerland, and Norway. All three kept policy rates steady. Economic pressure on the central bank to cut rates in Turkey is likely to grow in Q1 19 as the economic slump deepens. Market expectations are mostly in Q3 19, and this could gradually shift into Q2. The Swiss National Bank signaled no intention on hiking rates by cutting next year’s inflation forecast from 0.8% to 0.5% and warning that the risks are still to the downside. Norway’s Norges Bank kept signaled a rate hike in March 2019. The first hike in the cycle was in September, and the central bank forecasts now imply a more slightly more gradual cycle than previously.

The euro has fallen on days that the ECB announces its decision this year except in September. The euro is slightly firmer in the run-up to today’s announcement. The week’s high was set on Monday near $1.1440. The single currency has not been above today in Asia or the European morning. It has held above $1.1360 since moving above there in the US morning yesterday. There are three sets of maturing options that could be in play today. There is the $1.13 strike for around 1.2 bln euros. Between $1.1340 and $1.1350, there roughly another 1.65 bln euros, and at $1.14 there is an option for about 830 mln euros. We suspect many short-term traders will look to fade the initial reaction of Draghi headlines on ideas that the ranges are likely to prevail ahead of the FOMC meeting next week. Sterling is firm near yesterday’s best levels. After the uncertainty pushed sterling below $1.25 the past two sessions, it reached almost $1.2690 in the European morning. While the technical indicators leave sterling more room to run, we suspect that an extension toward the 20-day moving average (~$1.2750) may draw in fresh sellers.

North America

US 10-year yields have recovered from the test near 2.80% earlier this week, but above 2.90% has brought in new buyers. The FOMC meeting next week is the last big event of the year. A rate increase is widely expected. According to the CME’s model, the probability of a hike in Q1 19 has fallen to about a third from a half a month ago. Over the last two sessions, the S&P 500’s upside momentum faded in the afternoon. The recovery from the eight-month low on Tuesday faltered yesterday near the 20-day moving average (~2692), which also corresponds to a 50% retracement of this month’s drop.

The US dollar rose against the Canadian dollar in all but one week since the end of September. Near CAD1.3360, the greenback is nursing about a 0.25% gain this week. With a brief exception on Tuesday, the US dollar has remained within Monday’s broad range (~CAD1.3290-CAD1.3470). The US dollar tested the MXN20.00 level yesterday, the lower end of its one-month range. The Mexican peso is one of the emerging market currencies (along with the South African rand and Turkish lira) that is lower on the day. The dollar has softened against the peso for the past two weeks and is still off about two-thirds of one percent (at ~MXN20.13)

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,EUR/CHF and USD/CHF,MXN,newsletter