Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

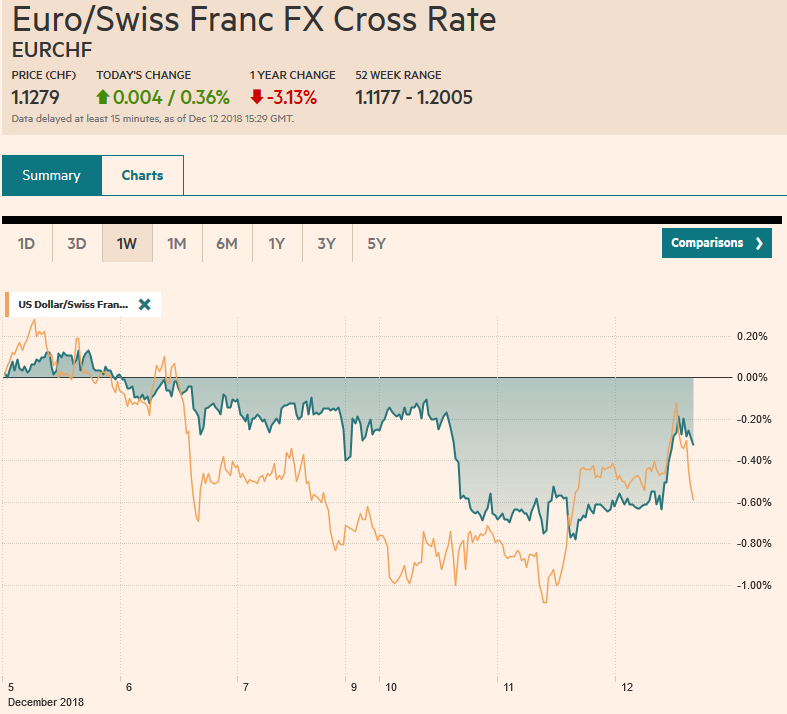

Swiss FrancThe Euro has risen by 0.36% at 1.1279 |

EUR/CHF and USD/CHF, December 12(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The US S&P 500 failed to sustain the early upside momentum, but global equities are moving higher today, and there is some optimism on the trade front. Emerging market equities and currencies are also doing well today. Canada granted Meng Wanzhou bail shortly after a former Canadian diplomat was arresting China threatening to escalate the delicate situation. Some US companies have been fined for embargo violations in the past without any corporate officers being arrested. In any case, the fact that US-China trade talks have continued also aided sentiment. All the equity markets in Asia rallied more than 1% with the exception of a few smaller bourses and China. European markets are following suit. The Dow Jones Stoxx 600 is up (~0.6% near midday) for the second consecutive session. It has not posted back-to-back gains in a little more than a month. JGBs, Bunds, Gilts, and Treasuries are seeing slightly higher yields while peripheral European bonds and French bond yields are easing (one-three basis points). UK’s May faces a vote of confidence among the Tory MPs today. Apparently, 48 letters were signed to trigger the challenge, but 158 is needed to win. Sterling is the strongest of the major currencies, but it is consolidating at the lower end of yesterday’s ranges, stalling near $1.2550. The Swedish krona is the weakest of the majors, losing above 0.4%. Although it is closer to putting together a government three months after the election, the softer than expected inflation will frustrate the Riksbank desire to normalize monetary policy. |

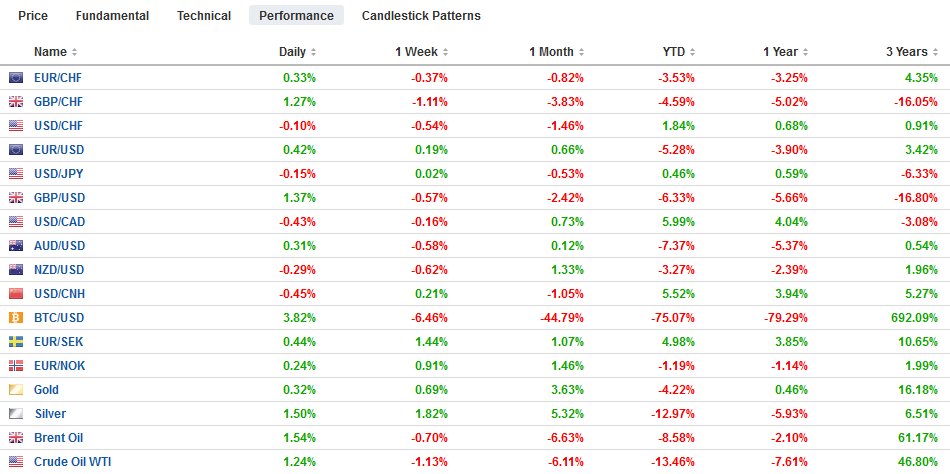

FX Performance, December 12 - Click to enlarge |

Asia Pacific

There is still no sign that the arrest of the Huawei CFO or other steps the US is taking to crack down on Chinese hackers and intellectual property theft is going to stall the still ill-defined G20 US-China trade talks. China is expected to soon if not already begun to purchase US soy. Reports suggest the process there is already underway to unwind the retaliatory tariff it imposed on US autos. For more than 16 years, the US and China had structured regular trade talks that were canceled by the Trump Administration. The resumption of discussions and the bringing the Chinese tariff back to 15% (from 40%) is a return to the status quo ante. Trump has also shown some willingness to keep the talks going. He indicated that if necessary he to interfere with the Huawei incident threatened (which it apparently is not).

The Japanese economic contracted at a 2.5% annual rate in Q3, twice the initial estimate, but the economy is bouncing back. The contraction was a function of earthquakes and other natural disasters. October industrial production jumped 2.9% on a preliminary basis, and the final estimate is due ahead of the weekend. Today, Japan reported core machinery orders rose 7.6% in October after an 18.3% plunge in September. Japan’s December Tankan survey is out tomorrow and sentiment is not expected not to have changed very much.

The Nikkei gapped higher, and this follows the gap lower on Monday, leaving a potentially bullish two-day island in its wake. The dollar is at seven-day highs against the yen near JPY113.50. There is an option for about $360 mln at JPY113.40 that expire today. This month’s high is about JPY113.85, and the trend line connecting the September, October, and November highs comes in near JPY114.00 today. A close below JPY113.00 would be disappointing. The Australian dollar is flattish around $0.7200. For the fifth consecutive session, it has slipped below there but has closed below it only once (Monday). A move above $0.7250, and ideally the 20-day moving average (~$0.7265) would lift the tone and confirm the base.

Europe

Prime Minister May’s decision to pull the meaningful vote in Parliament on the Withdrawal Bill which has been months in the making because it was going to be decisively defeated was the last straw for many Tory MPs. Enough letters from Tory MPs have been turned in, after weeks of threats and feints, that a confidence vote with the Conservative Party will be held later today. The results will be likely be known late in the US trading session. If May survives, she cannot face another such challenge for a year. If she loses, she cannot run in the next contest. Her defeat is seen as more likely to produce a more hardline Brexit Prime Minister. A new Tory Prime Minister may have limited room to move, as May found. The EC is in no mood to re-open negotiations and time is running out in any event. Article 50 could be revoked but would have to be part of a larger plan, and it is not clear the legitimacy of a second referendum. Rather than the uncertainty being lifted, it appears to be intensifying.

Despite Germany having reported an unexpected 0.5% decline in October industrial output, the eurozone as a whole saw industrial production rise 0.2%, a little more than expected. However, some of the good news was dampened by the fact that the 0.3% decline in September was revised to a 0.6% fall. The ECB’s two-day meeting ends tomorrow. There is little doubt that it will confirm the end of its asset purchase program. While monetary policy will remain quite easy, the risk assessment will likely remain balanced. Part of the economic slowdown is temporary, and this part already appears to be recovering. The continued strength of the labor market underpins the optimists’ case. The new forecasts are expected to shave next year’s growth and inflation projections, but the 2020 and for the first time 2021 forecasts are likely to depict a continued moderate expansion in the eurozone.

Although the reversal of the French government’s fiscal position, with private sector projections that next year’s deficit could be near 3.5%, Italy’s 2.4% deficit proposal by the populist-nationalist government does not seem like such problem, though of course, the debt levels are quite different. Italy’s Prime Minister Conte is in Brussels with some small compromises in hand, but the projected deficit is still coming in near 2.1%, which may not be enough to head of the excessive deficit procedure, which could ultimately lead to a fine next year. The situation in Italy is more fluid than it may appear and with the junior coalition member (League) overshadowing its partner (Five Star Movement), seeing its popularity rise, maneuverings next year, maybe ahead of the EU Parliamentary elections in the spring, could see a new government coalition or new elections. There have been more than 65 Italian governments since the end of WWII.

The euro started the week with a push toward $1.1445 and tested $1.1300 yesterday. It is consolidating in a quarter-cent range below $1.1340 today. Intraday resistance is seen in the $1.1350-60 ara. Support near $1.13 appears strong, and there are nearly 3.7 bln euros in options struck between $1.1275 and $1.1300 that expire today. There are another roughly 830 mln euros at $1.1400 as well that will be cut today, but it seems too far off to be in play. Sterling closed near $1.2560 on Monday and, despite the consolidative tone, it has been unable to test it. The outcome of the Tory vote is expected around 3:00 PM ET.

North America

The US November CPI is the data highlight of the day. The headline and core rates are expected to converge at 2.2% year-over-year. This will represent a slowing of the headline rate from 2.5% and a slight acceleration in the core rate from 2.1%. The report is unlikely to have much impact on expectations for the FOMC meeting in a week’s time. The CME’s model sees a 76.6% chance of a hike has been discounted in the fed funds futures. This is up slightly from the 75.8% chance seen a month ago (November 12). Separately, the API oil inventory estimate showed a large 10.2 mln barrel drawn down. If confirmed by the EIA today, it would be the largest since July. The market is looking for the EIA estimate of oil inventories to fall around 3.5 mln barrels.

In fairness, part of the challenge is that the fed funds futures contract settles at the average effective fed funds rate and it is being impacted by technical factors. That had been around the middle of the target range but has risen toward the upper end. The Federal Reserve tried to re-establish control by hiking the interest rate on reserves (and it pays interest on both required and excess reserves) only 20 bp while hiking the target range by 25 in September. The Fed may repeat this exercise next week, or tweak it a bit more. The FOMC is so serious about this that the November minutes suggested it was prepared to act before the December meeting, if necessary.

The Canadian dollar is consolidating in narrow ranges with the greenback holding a little below CAD1.34. Support for the US dollar is seen near CAD1.3360. Sentiment seems negative and while there has been much discussion of the flattening of the US curve, the Canadian curve (2-10 year) may become inverted first. The on-the-run 2-year yield is near 2.03%, and the 10-year yield is 2.07%. The Mexican peso is firm. The US dollar was turned back again after probing MXN20.50 last week. It tested the MXN20.1250 area in thin European dealings. The intraday technicals suggest it can recover back into the MXN20.20 area.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,EUR/CHF and USD/CHF,MXN,newsletter