Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

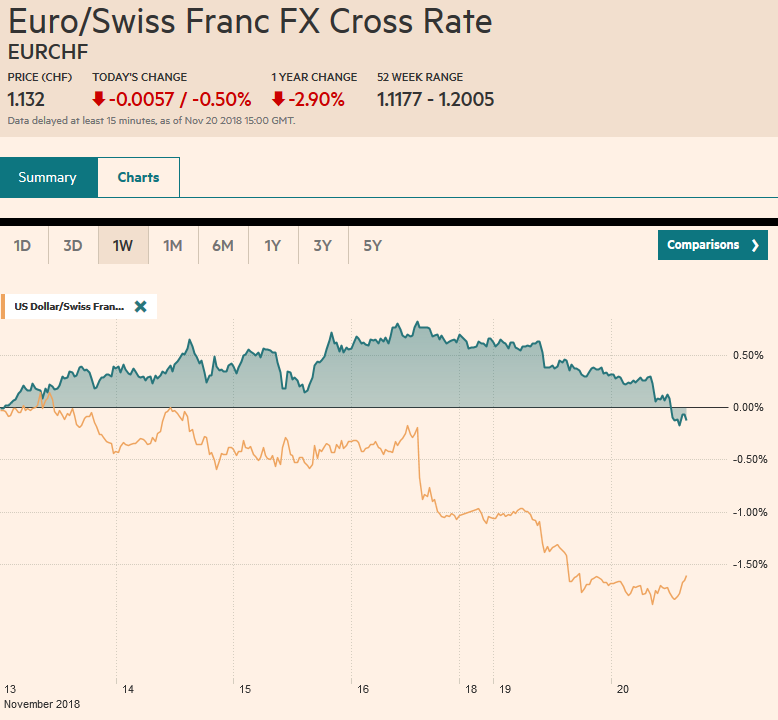

Swiss FrancThe Euro has fallen by 0.50% at 1.132 |

EUR/CHF and USD/CHF, November 20(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

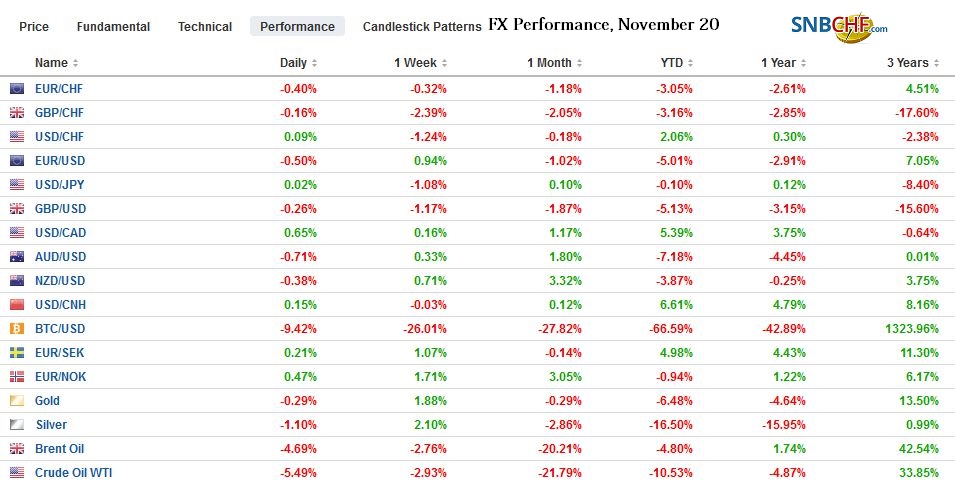

FX RatesOverview: Yesterday’s 3% drop in the NASDAQ is setting the tone for today. The US stock market advance had been led by a narrow group of equities, and those have come under strong pressure amid slower consumer demand and stricter export control. Asian equities were a sea of red today. Chinese markets led the sell-off with more than a 2% drop. In Europe, the Dow Jones Stoxx 600 is for a fifth session. It is off nearly 4.7% since November 8, when this leg down began. It has only gained in one session since then. Of note, Italian bank shares are off for a fifth session. They have risen in two of the past 12 sessions, and over this run, the Italian bank share index has lost about a quarter of its value. Current indications warn that the S&P 500 is poised to gap lower. Peripheral European bond yields are higher, as they trade with risk assets, while core bond yields and the US 10-year Treasury yield is slightly softer. The US dollar is mostly firmer, though the Swiss franc and Japanese yen are finding support amid the equity slump. |

FX Performance, November 20 - Click to enlarge |

Asia Pacific

Bank of Japan Governor Kuroda stuck to his stance. Negative interest rates are still needed. He dismissed as an academic paper claiming that ending negative interest rates could help lift inflation as not being representative of BOJ thinking. Although he recognized that there was little chance of reaching the inflation target in FY19 or FY20, he continued to sound optimistic. The BOJ forecasts average core CPI (excluding fresh food) of 1.4% in FY 19. Many investors are less sanguine. The decline in oil prices and mobile phones and free nursery school warns of less rather than more price pressures.

The minutes from the Reserve Bank of Australia’s recent meeting did not shed much fresh light on the policy outlook. Essentially, the RBA said that the next move in rates is more likely to be higher than lower, but there is no strong case for a near-term move. RBA Governor Lowe indicated he was watching slumping housing prices closely in Sydney and Melbourne. The IMF’s outlook was more concerning. It said the balance of risks were on the downside due to slowing world growth and rising trade tensions.

The dollar slipped to new lows for the month against the yen (~JPY112.30). The 100-day moving average is found just above JPY112.00, though the rally began in late October near JPY111.30 and with support near JPY112.50 fraying a return to that low cannot be ruled out. The Australian dollar peaked near $0.7340 at the end of last week. It is now slipping through the 100-day moving average (~$0.7255). A trendline connecting the late October and the last week’s low is found near $0.7225. A break could signal a return to the $0.7160 area. After strengthening last week, except on Monday, the Chinese yuan eased slightly for the second consecutive session today. The ranges have been exceptional narrow. Chinese one and two-year yields are slipping below US yields, and this is seen negative for the yuan over time.

Europe

The UK-EU negotiated deal has few friends, but there is no agreement on an alternative or even an alternative leader. It appears more Tory members of parliament said they would send a letter of no confidence than actually sent the letter. Prime Minister May appears to have survived to fight another day. Making a virtue out of necessity, May’s critics are now talking about a challenge next month after Parliament votes. However, another problem has emerged over the past 24 hours: Gibraltar. Although everyone has known of the issue, there was no attempt to address it, and Spain has indicated it will not support the agreement until the wording on Gibraltar is changed.

After the ill-fated election last year that saw the Tories lose their majority, the unionist party (DUP) from Northern Ireland provided the votes needed to govern. However, piqued by the agreement, the DUP abstained or voted against the government’s Finance Bill yesterday. This is a shot across the bow and warns of the pressure that remains on the UK government.

Euribor for next December is trading firmer and the implied yield as at its lowest level in two years. The market has largely unwound the expectations of a rate hike at the end of next summer. The implied yield has fallen nearly 15 bp over the past month. Some observers are attributing this trade tensions or Italy. We are less sanguine. Recall that it was Germany, the region’s largest economy that contracted in Q3, not only Italy. Also, the flash PMI due at the end of the week is not expected to signal much of a recovery after 0.2% growth was reported in Q3. Moreover, given this and the drop in oil prices, the ECB staff forecasts may shave inflation and growth forecasts.

The euro initially extended its gains toward $1.1470 in late Asia before being sold to nearly $1.1420 where bids were found in early Europe. The $1.1400 area offers support, and there is a $1.15 option that is rolling off today for nearly 615 mln euros. Sterling is trading just inside yesterday’s range (~$1.2795-$1.2885). Chart resistance is seen in the $1.2900-40 area.

North America

The US reports housing starts and permits today. Housing starts peaked earlier this year around 1.334 mln (seasonally adjusted annual rate). They slumped to 1.177 mln in June and have been chopping around since then. Housing starts stood at 1.201 mln in September. The median forecast from the Bloomberg survey is for pick up to 1.225 mln. The risk appears on the downside, though permits, which initially fell in September were revised higher. Nearly every measure of the housing market has weakened as costs have risen. Yesterday the homebuilder index fell to four-year lows. One mitigating factor is that the housing market accounts for a considerably smaller part of GDP than before the Great Financial Crisis. Press reports indicate that banks and non-bank financial institutions are scaling back or closing related departments.

A new troika is emerging at the Federal Reserve: Powell, Clarida, and Williams. We understand all three to have signaled intentions to continue to raise interest rates gradually. The Chair, Vice-Chair, and New York Fed President recognized potential headwinds from aboard, but the contraction in Germany and Japan seems over even before the Q3 contractions were announced. The purpose of it was likely the desire to explain the balanced assessment. At the same time, with some repo rates rising above the upper end of the Fed funds target range, the FOMC may opt to hike the interest on reserves a little less than the target range, as they did in September.

Mexico’s ambassador to the US suggested that the US will lift or begun to lift the tariffs on steel and aluminum that were levied against Canada and Mexico on national security grounds before the NAFTA 2.0 bill is signed. All three presidents are expected to sign the bill at the G20 meeting on Nov. 30- Dec 1. The US dollar continued to be within striking distance of MXN20.50, the recent high. The US dollar looks content in a CAD1.3150-CAD1.3200 near-term trading range.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,EUR/CHF,newsletter,SPX,USD/CHF,yuan