Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss FrancThe Euro has risen by 0.11% at 1.1429 |

EUR/CHF and USD/CHF, October 05(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe US dollar is firmer against most of the major and emerging market currencies. The yen and sterling are resisting the pressure, while the South African rand and Russian rouble are paring some of this week’s declines. US equity losses yesterday weighed on Asian and European trading today. The MSCI Asia Pacific Index fell every day this week to post its worst week in seven months, losing more than 3.5%, which warns the risk of a steep sell-off in China when its markets re-open on October 8. The index of H-shares that trade in Hong Kong fell 3.75% this week. The technology sector has been hit particularly hard, and the MSCI Asia Pacific technology index at the lowest level since July. European stocks are also under pressure today, but the smaller technology representation has helped it hold upper better than Asian markets. The 0.6% decline of the Dow Jones Stoxx 600 in the European morning brings this week’s loss to about 1.5%. Core benchmark yields are up two-three basis points, and most of the European peripheral bond yields are up a little less. Italian bonds are an exception, and the yield is up about five basis points, bringing the increase on the week to eight basis points, and keeps the pressure on Italian bank shares, where the index is off about 4% this week following last week’s 8.3% plunge. The US 10-year yield is at 3.20% ahead of the US jobs data. Japan: The dollar is higher against the yen for the fourth consecutive week but this week’s gains are marginal after finishing last week around JPY113.70. And even these upticks are vulnerable to the volatility after the US employment data. There is a nearly $550 mln option at JPY114 that expires today and $1.2 bln at JPY113.50, which is just below the week’s low. Contrary to some expectations, the BOJ did not reduce the amount of super-long bonds was buying, but judging from its inaction, it is hesitant about resisting the upward pull on yields coming from the US. Although August cash earnings were disappointing (0.9% year-over-year after 1.5% in July, household spending jumped 2.8% (from 0.1% in July). It is the strongest in three years. Australia: The poor construction PMI (49.3 vs. 51.8) and an uninspiring 0.3% rise in retail sales (after a flat reading in July failed to arrest the Australian dollar’s decline, which did not rise in a single session this week. Near $0.7065, it is off about 2.2% on the week, the biggest decline in nearly eight months, leaving it at fresh two-year lows today. Its perceived sensitivity to Chinese developments may discourage bottom pickers ahead of the weekend and the re-opening of Chinese markets on Monday. Our medium-term objective remains near $0.6900. |

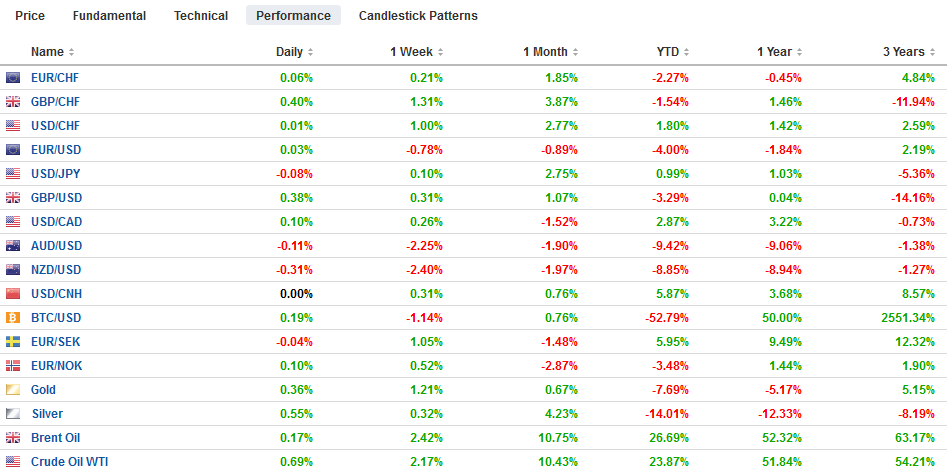

FX Performance, October 05 - Click to enlarge |

UK: Prime Minister May survived the Tory Party Conference, and the reports suggest that EC officials are suggesting that a deal is “very close,” As we noted earlier this week, there is talk that May will offer a fresh compromise to the EC on the Irish border and future trade deals. Ireland is supportive of the direction May is moving on its border. What we see as a trilemma, however, remains in place. It is still not clear that a Brexit plan can appease three stakeholders, the EC, May’s cabinet, and the UK Parliament. Sterling nearly posted a potential key reversal yesterday, making a new low for the move and proceeding to close 2/100 of a cent below the previous day’s high. Still, it was sufficient, and there has been some light follow-through buying today. There is are nearly GBP500 mln in options struck between $1.30 and $1.3025 today that are expiring. Trendline resistance comes near $1.3110, which is high for the week and the 100-day moving average.

Euro: European economic developments are light. There are two talking points today. The first is appears to be a recycling of an older story that the ECB could extend maturities as it asset-buying program becomes limited to simply re-investing maturing proceeds starting next year. The second is Italy. ECB President Draghi met with the Italian President Matterella apparently cautioning on the budget. Although the government revised down its deficit projections, the growth estimates, revealed and too optimistic. It forecasts 1.5% GDP next year, 1.6% in 2020 and 1.4% in 2021. Private sector economists do not see growth over 1.2% over the next three years.

Moreover, and most troubling for the EC is the government’s projection of structural deficit, which adjusts for cyclical and one-off measures, is projected at 1.7%, or nearly double the 0.9% anticipated for this year. The euro continues to struggle. It has risen one session last week and one session this week. It is in less than a third of a cent range today ahead of the North American session. It briefly traded above $1.18 on September 24, and the low this week was about $1.1465. Two large options are expiring today: The $1.1450 strike is for 2.3 bln euros, and the $1.15 strike is for 1.9 bln euros.

Emerging Market Highlights: India’s central bank surprised the market by not hiking rates today. Although it changed its self-described stance to “calibrated tightening” from “neutral,” it was insufficient to prevent the rupee from dropping further in disappointment. The dollar was trading near INR73.60, and after the 5-1 decision, the greenback climbed above INR74.1. Indian equities responded positively. To be sure, Indian rates have not peaked.

South Korea reported its September CPI jumped to 1.9%, the highest in a year, from 1.4% in August. This boosts speculation that the central bank will hike rates. It meets next on October 17-18.

The Brazilian real takes a four-day advance into today’s session. Regardless of the election results, Monday is likely to be volatile. Investors seem to prefer Bolsonaro and the latest (Datafolha) poll puts him in the lead over the Workers’ Party candidate Haddad. However, without a majority, Bolsonaro would likely face Haddad in a run-off (October 28), and here the polls are within the margin of error.

US Data: The ISM surveys, the weekly jobless claims, and the ADP private sector estimate give investors little reason not to expect a strong report. Yet economists have forecast a 180k rise in non-farm payrolls down from 201k in August. Job growth this year is averaging 207k a month, which is ahead of last year’s average of 182k and the 2016 average of 195k. This is no magic. It is at least partly a function of a large dollop of fiscal stimulus and purchased in part by the nearly trillion dollar budget deficit.

There may still be room for an upside surprise, but given the dollar’s advance over the past two weeks, it may take more than a marginal beat to push the greenback significantly higher. This may be especially true if earnings growth does not accelerate but slows, which is a reasonable forecast given last September’s heady 0.5% increase that drops out of the year-over-year comparison. Even though wage growth when adjusted for inflation is not posting strong gains, the 1.6 mln net new jobs created so far this year is underpinning consumption. Credit is also helping. Consumer credit for August will be reported later in the day. It has risen by an average of $12.4 bln a month this year, slowing from 2017 (monthly average was $15.60 bln), and 2016 (averaged $19.2 bln).

There is a nagging concern that the US trade practices and the retaliation that has followed may squeeze exporters and jobs in manufacturing. Manufacturing lost 3k jobs in August, the first decline this year. If a back-to-back loss is unexpectedly reported, it will draw much attention. The August trade figures are expected to show a widening of the shortfall to around $53.5 bln from a little more than $50 bln. The monthly deficit has averaged $48.2 bln this year compared with $45.1 bln. Some of the aggregate demand fueled by the fiscal stimulus is being met by imports.

Canadian Data: Canada also reports trade and jobs data. It may very well announce the third consecutive month of less than a C$1 bln shortfall, the longest such streak since 2014. Although NAFTA 2.0 does not address the steel and aluminum tariffs on Canada, Canadian trade figures have held up better than many feared. Canadian employment growth has been exceptionally volatile this year. The monthly report has been in a -88k to 54k this year. Last year the range was 12.6k to 81.2k, and in 2016 the range was -10.1k to 66.6k. The median forecast from the Bloomberg survey is 25k. The US dollar’s broad performance may be the key to the Canadian dollar ahead of the weekend. Against the Canadian dollar, the greenback entered today’s session nearly flat on the week after depreciating from roughly CAD1.32 in early September to a little below CAD1.28 on the NAFTA 2.0 news. The US dollar has bounced since Monday’s gap lower opening. The gap was filled on Thursday as it retraced the last leg down. The CAD1.2935-CAD1.2970 band offers the next chart resistance.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$EUR,brl,EUR/CHF,jobs,newsletter,Trade,USD/CHF