Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

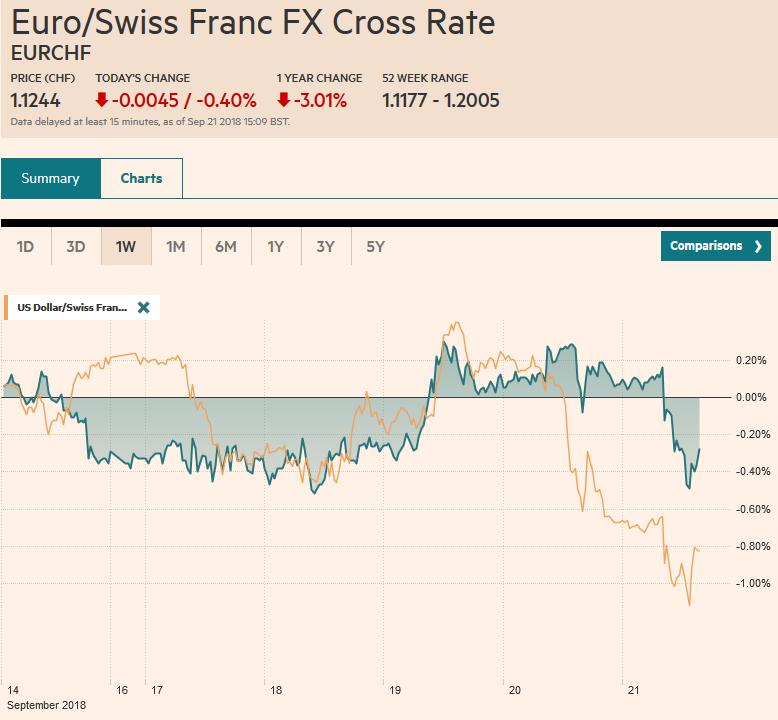

Swiss FrancThe Euro has fallen by 0.40% at 1.1244 |

EUR/CHF and USD/CHF, September 20(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe euro poked through $1.18 for the first time since the June ECB meeting. There is an option for about 740 mln euros that expires there today and another at $1.1775 for 890 mln euros. That June high was near $1.1850, which was a five-high. If today’s gains hold, it would be the eighth gain in the past 10. Not only does there appear to be an equity rotation taking place but the Italian premium over Germany (10-year) has narrowed about 60 bp this month we see several large banks taking a more optimistic look at Italian debt, encourage by official suggestions that next year’s deficit will be in the 1.6%-1.8% range. Talk of a parallel currency an existential confrontation with the EU has all but evaporated. Meanwhile, the dollar rose to nearly JPY112.90 today, its best level since mid-July. There is an option for almost $600 mln at JPY112.50. The Nikkei began the week near the 23,000 area that has capped it over the past several months and is finishing the week within striking distance of 24,000. The year’s high a little above thee was set in January. However, note that foreign investors have been liquidating Japanese equity holdings for eight consecutive weeks through last week. |

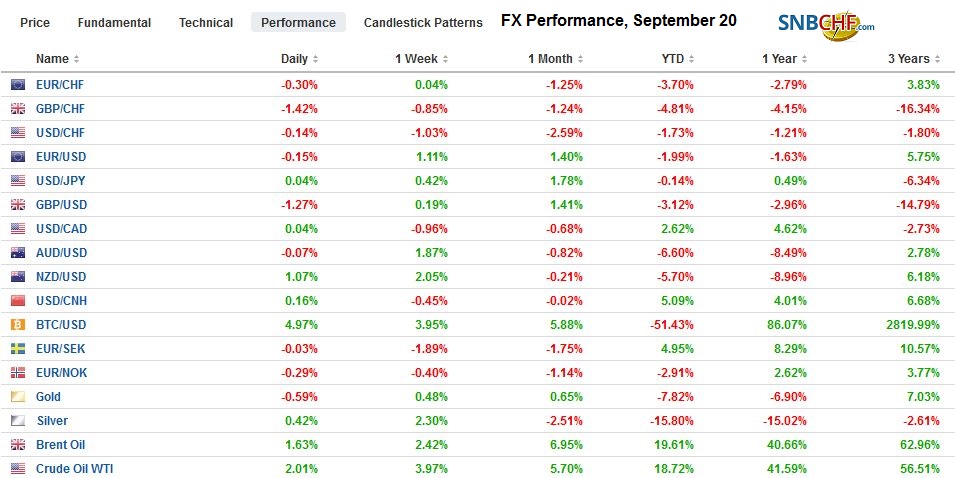

FX Performance, September 20 - Click to enlarge |

Sometimes the dollar is the key mover, but sometimes, like today, it seems to be the fulcrum, reflecting disparate moves among other currencies. While the euro is at two-month highs, the yen is near two-month lows. The euro is bouncing off two-month lows and the 100-day moving average against sterling. Most emerging market currencies are advancing against the dollar today. Of note, the Hong Kong dollar’s 0.4% rally is the largest in 15-year.

There are several developments today, and not all of them are reflected in the prices. For example, the flash PMI for the eurozone was softer than expected. The composite reading for September slipped to 54.2 from 54.5. Note that it averaged 54.3 for Q3 after 54.7 in Q2 and 57.0 in Q1. German and French manufacturing softened to 53.7 and 52.5 from 55.9 and 53.5 respectively. It may be a bit simplistic, but this is one of the places one would look for the impact of the trade tensions. Services, on the other hand, are more reflective of domestic demand. German services PMI rose to 56.5 from 55.0, while French services eased to 54.3 from 55.4.

The US-China trade conflict escalated this week, but this may work to the advantage of other countries. Japan, Taiwan, and South Korea’s latest export figures have been strong. Korea reported today that exports in the first 20 days of September jumped 21.5% year-over-year (imports rose 14%). Taiwan reported export orders rose 7.1% in August rather than 6.2% as the median forecast in the Bloomberg survey had it. Earlier this week, Japan reported a 6.6% increase in exports from a year ago, which was also above expectations.

The BOJ surprised investors today by trimming the amount of longest maturities it buys of JGBs by JPY10 bln. Many participants see this as a stealth tapering, though the BOJ denies it. Separately, Japan reported a small uptick to 0.9% from 0.8%, and the headline pace quickened to 1.3% from 0.9%.

The Hong Kong dollar’s surge today is being attributed to three drivers. First, there is the unwind of a carry trade that uses the HKD as the financing currency to buy US Treasuries. The sell-off in US Treasuries is forcing some to unwind the trade Second, China indicated it will be boosting T-bill issuance, and many see this as a potential threat to liquidity in Hong Kong. Third, given the peg, the Hong Kong Monetary Authority follows the Fed. The Fed is widely expected to hike next week. With upcoming holidays and quarter-end, there is a short-squeeze.

Meanwhile, global equities are powering ahead. The MSCI Asia Pacific Index rose 1% today. It is the fourth consecutive advance, and the two-week gain of 3.7% is the most in seven months. Chinese shares participated. The CSI 300 rose 5.2% this week, the most in three years. The Dow Jones Stoxx 600 is extending its rally for a sixth session today. It was up about 1.6% this week on top of 1% last week.

European bonds are mostly firmer, while the US 10-year yield is establishing a foothold above 3%. In May, the US yield popped briefly through the 3.12% level, which is the next technical target. The only data on tap today is the flash Markit PMI.

Canada reportsJuly retail sales and August CPI. Headline retail sales were likely held back by auto sales, but are still expected to have rebounded from a soft June report. Excluding autos, Canada’s retail sales are expected to have risen by 0.6%. Headline consumer inflation may have ticked down in August after a heady 0.5% increase in July. The year-over-year rate may pullback from July’s 3% pace. Core rates are expected to have been steady. The market appears to have discounted a little more than a 75% chance of a hike next month. The US dollar is straddling the CAD1.29 area.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CAD,$EUR,$JPY,EUR/CHF,newsletter,USD/CHF