Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

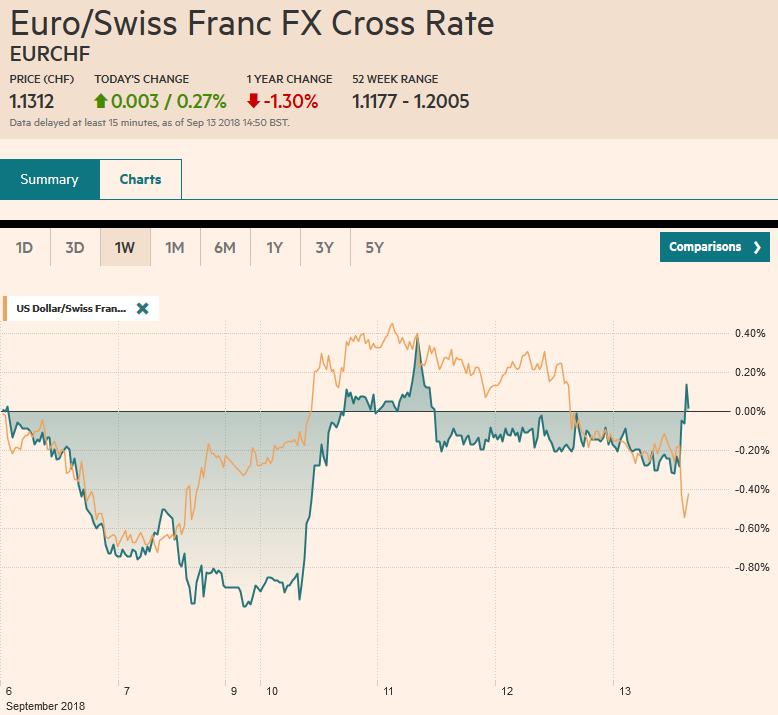

Swiss FrancThe Euro has risen by 0.27% at 1.1312 |

EUR/CHF and USD/CHF, September 13(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe euro has fallen on ECB meeting days this year and the last two meetings in 2017. The euro is trading in the upper end of the $1.1525-$1.1650 trading range. The intraday technicals suggest that the $1.1600 area may hold until at least the Draghi’s press conference. There are three large options that are expiring that could impact trading: $1.1550 (1.3 bln euros), $1.1600 (1.8 bln euros), and $11625 (991 mln euros). The euro has not finished the North American session above $1.1630 here in September. The dollar remains within yesterday’s range against the yen. It has been in a JPY110.85-JPY11.65 range so far this week. There are two sets of expiring option to note. The first is stuck between JPY111.50 and JPY111.60 and are for $1.76 bln. The other set is JPY111.65-JPY111.75 for about $840 mln. The yen is sidelined with the focus on the European central banks. Sterling has been confined to a little more than a quarter cent range around yesterday’s settlement. So far, it is the first session since August 2, that it is not traded below $1.30. It is also posting gains for the fourth consecutive session. A close today below $1.2980 would weaken the technical tone. |

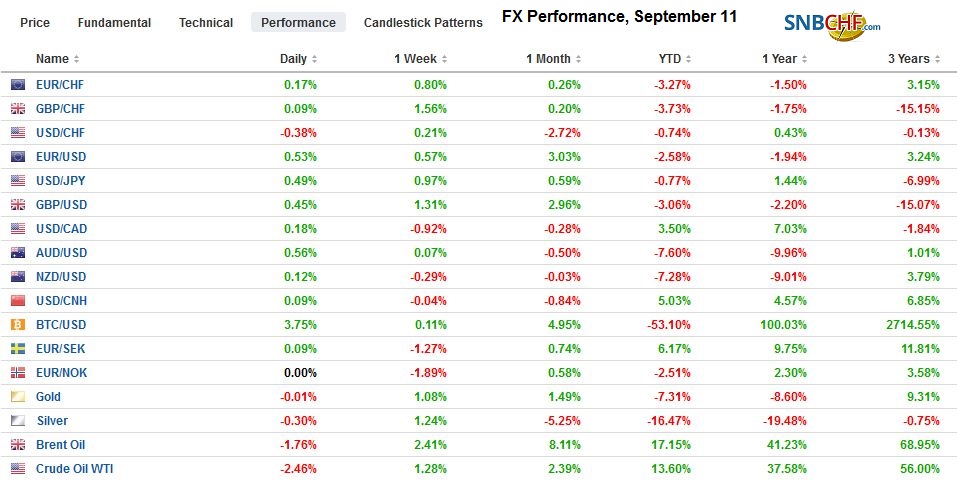

FX Performance, September 13 - Click to enlarge |

There is an eerie calm in the markets ahead of the highlight for the day and week. The central banks of the eurozone, UK, and Turkey hold policy meetings, and the US reports August CPI.

The greenback is a mostly firmer, with the Australian dollar as the notable exception. On the one hand, we would note that is it higher for the fourth consecutive sessions, after finding some support near $0.7100 earlier in the week. A stronger than expected jobs report help lift the Aussie to $0.7200 today, and there is an A$ 753 mln option expiring at $0.7220 today.

Australia report growing 44k jobs in August, nearly three times more than expected and mostly accounted for by a nearly 34k increase in full-time positions. The participation rate ticked up to 65.7% from a revised 65.6%, but the unemployment rate was steady at 5.3%. While the data is constructive, there is not much impact on the outlook for monetary policy. Offsetting the jobs growth is soft wage pressures, subdued inflation, and weaker house prices.

Another notable feature of the Asian session was the rally in equities. All markets in the region participated, except Australia, where the ASX 200 fell 0.75%. The MSCI Asia Pacific Index gained almost 1.0% to snap ten-day slide. It gapped higher and follow-through buying tomorrow will be key to the near-term outlook. The MSCI Emerging Markets Index is also up around 1% before the Latam session, and it is the second day of gains.

There are two areas in which the market may be getting ahead of itself. The first is on the trade. Reports yesterday that the US Treasury has invited Chinese officials for talks in Washington helped spur a risk-on rally. We are skeptical. In May, the US Treasury appeared to have struck a deal with China that would lead to it buying much more US products. However, President Trump backed off and by doing so, sent a signal to China that the trade issue will not be resolved by the Treasury Department. The reports of an intended meeting follow press reports covering the warnings by several larger banks that across the board tariffs on China that the US was threatening would likely trigger a sharp drop in US stocks, perhaps wiping out next year’s anticipated earnings growth.

If the Treasury does host talks, and there is no reason to think China would turn down the invitation, we do not expect a deal to be reached. However, if China simply renews its offer to buy more US goods, which incidentally would likely come at the expense of other exporters to China, that may be sufficient to set the stage for a Trump-Xi meeting in late November, after the US elections, on the sidelines of the G20 meeting.

The second issue that the market may be getting ahead of itself is on Brexit. The changing tone of the EC has helped sterling recover against both the dollar and the euro. The problem, the way we see it, is that Prime Minister May cannot make all the key stakeholders happy. The Chequers Plan, which is servicing as the basis for agreement with Europe is not secure at home.

The next few weeks will likely feature May trying to win over her party and the eurosceptics. One area that she may make a concession is on offering a more restrictive immigration policy, and this could come as early as the September 24 special cabinet meeting. This is ahead of May’s October 3 speech at the party conference. It is shortly after that that May could be subject to a leadership challenge.

After deciding unanimously to lift rates last month, there is practically no chance of another rate hike today. Indeed, the BOE meeting may be as close to a non-event as possible. It will be overshadowed by the central bank of Turkey which is under strong pressure to raise interest rates. The dollar is nearly 3% higher against the lira, following comments by Erdogan that he prefers lower rates. It is the strongest gain in two weeks. Until today, the lira was building on last week’s 2% recovery.

The main feature of the ECB meeting may be the staff’s forecasts. We had anticipated a downward revision in the growth forecast, and recent press reports give it is some validation. However, to be clear, the tapering (to 15 bln euros from 30 bln euros) starting next month, and stopping at the end of the year is on automatic pilot, by which we mean the bar to changing it is very high. The softer real data and the heightened trade tensions, however, are not yet a significant obstacle because growth is still seen above trend, which means, from the view of policymakers, that excess capacity is being absorbed. This underpins expectations that prices will gradually rise. It is not so much that the region’s economy is experiencing a soft patch, but rather it is returning toward trend growth.

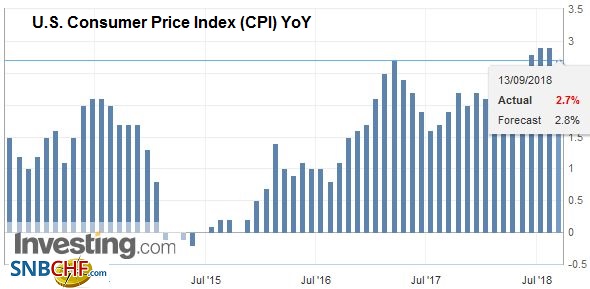

United StatesThe US CPI may not get much attention as the ECB press conference commands more attention. Yesterday’s PPI was softer than expected but the linkages with the CPI is limited. The market expects the headline rate to possibly soften a touch (2.8% vs. 2.9%) |

U.S. Consumer Price Index (CPI) YoY, Sep 2013 - Sep 2018(see more posts on U.S. Consumer Price Index, ) Source: investing.com - Click to enlarge |

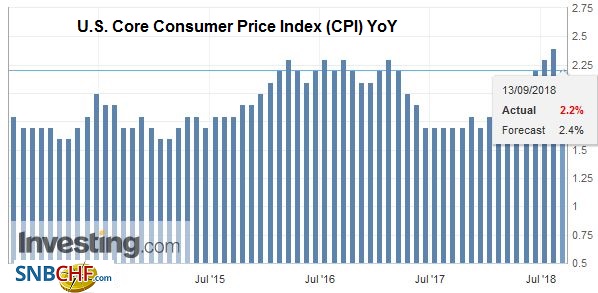

| and for the core rate to be steady (2.4%). There is no implication for policy and little doubt that the Fed will hike rates on September 26. The market is also feeling more confident (80%+) of a follow-up hike in December. Yesterday Governor Brainard suggested that the neutral rate (~2.9%) is not a cap on rates is the latest signal that monetary policy may actually become restrictive. We understand the neutral rate to be a mile marker rather than some kind of barrier for policy. |

U.S. Core Consumer Price Index (CPI) YoY, Sep 2013 - Sep 2018(see more posts on U.S. Core Consumer Price Index, ) Source: investing.com - Click to enlarge |

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$EUR,$JPY,EUR/CHF,newsletter,U.S. Consumer Price Index,U.S. Core Consumer Price Index,USD/CHF