Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

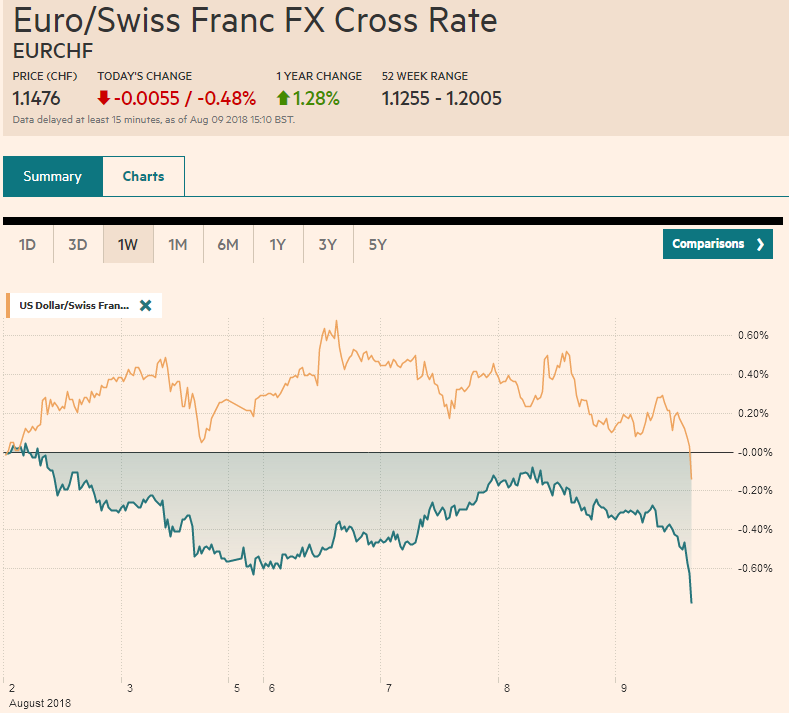

Swiss FrancThe Euro has fallen by 0.48% to 1.1476 CHF. |

EUR/CHF and USD/CHF, August 09(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe global capital markets are mostly quiet. US sanctions on Turkey and Russia are pressuring their respective currencies, and the New Zealand dollar has slumped nearly 1.5% on the back of a dovish hold by the central bank. The Kiwi is at 2.5-year lows near $0.6650. Sterling is lower for the sixth consecutive session amid no-exit Brexit fears and made fresh lows since last October before recovering to little-changed levels in late morning turnover in London. The euro is consolidating within yesterday’s range. The euro has mostly been in a 20 tick range on either side of $1.16, where an 823 mln euro option expires today. There is a billion euro option at $1.1550 that will also be cut. European bonds are firmer and Italian bonds are outperforming. Although there have been some intraday moves, Italy’s 10-year yield is off about six basis points this week, and four are being recorded now. European shares are heavy, with only the consumer discretionary sector showing some mild gains. Energy is the worst performing sector. Oil prices are stabilizing after sliding 3.2% yesterday, where trade tensions and Chinese action on US refined products took the entire complex down. US oil stocks did not fall as much as had been expected. The dollar was sold to JPY110.70 near midday in the Asian session, a two-week low, before recovering toward JPY111.20. There are some options expiring that will influence activity. There are around $1.8 bln in options struck at JPY111.00-JPY111.05. There is another $1.06 bln in JPY111.25-JPY111.30 options and another ($1.9 bln) JPY111.50-JPY111.55 that expire today Japan’s 30-year bond auction (JPY700 bln or ~$6.3 bln) was well received, which helped to ease the long-term Japanese yields, while yields in the belly of the curve edged higher, while the short-end eased. |

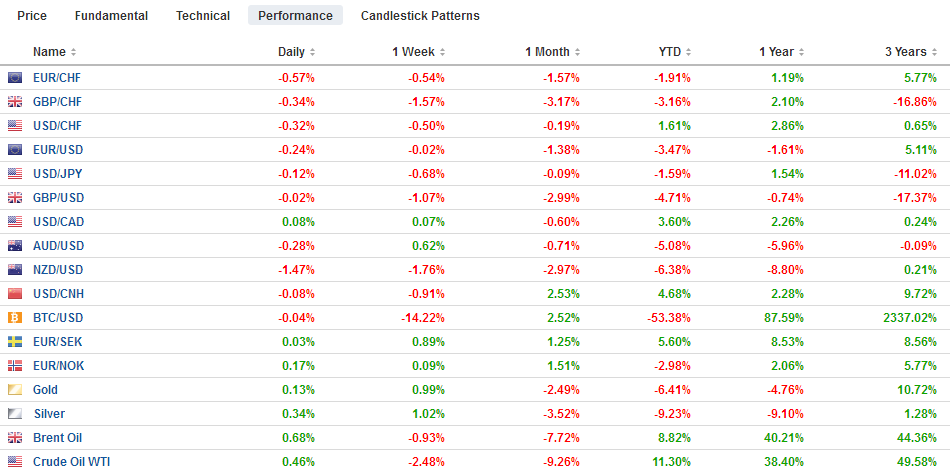

FX Performance, August 09 - Click to enlarge |

Japanese stocks eased but most bourses in the region edged higher, and the MSCI Asia Pacific firmed a minor 0.1%, but it is the third consecutive advance. Chinese shares continued to recover with the Shanghai Composite up 1.8%. The Chinese yuan firmed slightly and is now a little higher for the week. China reported July inflation figures. CPI rose 2.1% after a 1.9% rate in June. It is the second gain in a row. Producer prices slipped to 4.6% from 4.7%. The market had expected slightly lower readings of both reports, but they were understood as benign.

Meanwhile, short-term Chinese rates continue to ease. The 7-day repo rate has fallen non-stop since pushing above 3.0% in late July. Today’s five basis point decline follows a 28 bp fall Tuesday and Wednesday and puts the benchmark rate at 2.085%. Similarly, three-month SHIBOR last rose on June 15 when it reached 4.352%. Today’s decline puts it at 2.816%. This seems to run counter to efforts to arrest the yuan’s slide.

The Reserve Bank of New Zealand pushed out by a year to Q3 2020 when it expects a rate hike may be appropriate. This is a year later than it signaled three months ago. Moreover, the risk that rates will have to be cut first are broadly balanced. Officials are happy with the New Zealand dollar’s weakness and used the statement and public comments to lean against the building expectations evident in the money market for tightening.

The Canadian dollar staged an impressive recovery yesterday from a sell-off spurred by an escalation of the diplomatic dispute with Saudi Arabia. Saudi Arabia has announced divestment from Canada and a trade embargo. The bark is worse than the bite. This year Canada has exported about C$1.4 bln of goods to Saudi Arabia and imported about C$2.0 bln. Saudi direct investment in Canada is estimated to be about C$1.3 bln, and Canadian direct investment in Saudi Arabia is estimated at less than C$30 mln. Saudi Arabia may have some Canadian dollars in reserves, and if you make some conservative assumptions, it could be C$10 bln.$20 bln.

The figures here are not large relative to their universe, but compared with the average daily turnover, it could have a short-term impact. When everything is said and done, the net impact is minor, it is virtually unchanged since last Thursday.

The economic calendar in North America picks up today with the US reports weekly initial jobless claims, PPI, and wholesale trade and inventories. The data may have headline risk, but these data points do not typically move the market. The wraps up the quarterly refunding with a 30-year bond sale. The Fed’s Evan’s speaks to reporters near midday in Chicago. He is seen on the dovish side of the Fed’s spectrum. Yesterday’s 10-year note auction was well-received and better than the lukewarm reception to the three-year note sale the day before. Canada reports housing starts and new home prices.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$CAD,$CNY,$EUR,$JPY,EUR/CHF,newslettersent,NZD,USD/CHF