Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

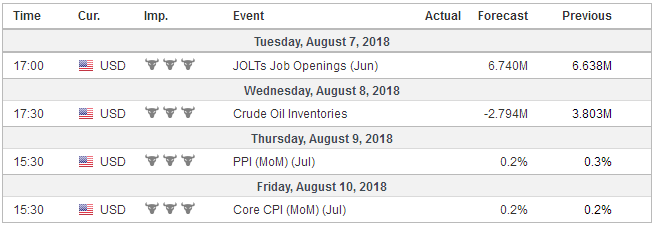

United StatesWith most of the major central bank meetings and important economic data out of the way, the dog days of August are upon us. In terms of drivers, it means that players will have to look elsewhere for inspiration and it means that market liquidy is likely not at its best. That said, there are a few economic reports that will grab investors’ attention, even if briefly. Among them will be the US July CPI. The headline is likely to have been lifted by gasoline prices, and a new cyclical high of 3% may be recorded. The core rate is expected to be flat at 2.3%. It will translate into a decline in real earnings. Yet this measure is not comprehensive and does not track consumption very well. We already know that auto dealers cut their incentives and sales fell, but excluding autos, retail sales (August 14) likely rose. Personal consumption rose at a 4% annualized pace in Q2, partly rebounding after a soft Q1 (0.9%). There have only been a few quarters during the US expansion that this was exceeded. A return to the longer-term trend (average) of around 2.6% points to firm growth. If the part of the economy that contributes 70% grows by 2.6%, it translates into gives 1.8% GDP before government components, investment, not to mention trade. |

Economic Events: United States, Week August 02 - Click to enlarge |

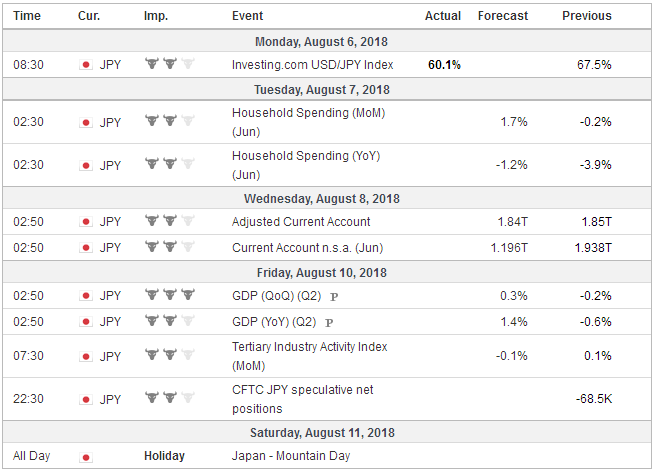

JapanJapan reports Q2 GDP at the end of the week ahead. After contracting by 0.2% in Q1, the economy recovered and appears to have expanded by as much, if not a little bit more, in Q2. Consumption and business investment improved. Still, the world’s third-largest economy essentially stagnated in H1 and Q3 is not off to a strong start (soft manufacturing PMI) and the GDP deflator may have fallen back into negative territory, for the first time in a year. Some economists regard the GDP deflator as a superior inflation metric, and the whiff of deflation may help the BOJ stabilize the JGB market after widening the band for the 10-year yield and intervening before the upper band was reached. |

Economic Events: Japan, Week August 02 - Click to enlarge |

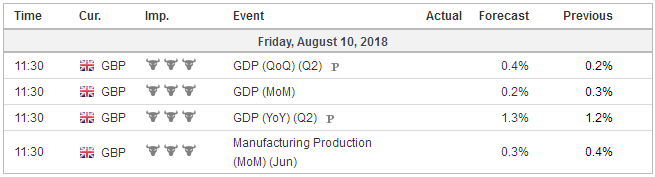

United KingdomThe UK’s reports June trade and industrial production data and the market will react twice to it. First when the data is released and then again at the end of the week when the first estimate of Q2 GDP will be published. The newly introduced monthly GDP series is likely points around 0.2% growth in June. Growth in the second quarter picked up after the 0.2% pace reported in Q1. Most expectations for Q2 GDP are at 0.4% and kept the year-over-year pace at a soft 1.3% (1.2% in Q1 was the weakest in six years). With monetary policy no doubt on hold for some time, attention is squarely on Brexit and the dollar’s tone in terms of sterling’s drivers. Canada followed up a stronger than expected May GDP report with a smaller than expected trade deficit. On July 10, Canada reports July jobs data. Strong data may boost confidence that the Bank of Canada is the only major central bank that can keep up with the Federal Reserve in the coming quarters. The two-year yield has risen by 32 bp since the end of June, and the implied yield of the December BA futures reflects in its entirety. The US premium over Canada for two-year borrowing has narrowed by 15 bp since the middle of July. In contrast, the Reserve Bank of Australia and the Reserve Bank of New Zealand hold policy-making meetings in the week ahead. A move on rates by either is highly unlikely. Both currencies remained penned in ranges. The official discouragement of selling yuan by the PBOC before the weekend helped reinforce the lower end of the ranges. |

Economic Events: United Kingdom, Week August 02 - Click to enlarge |

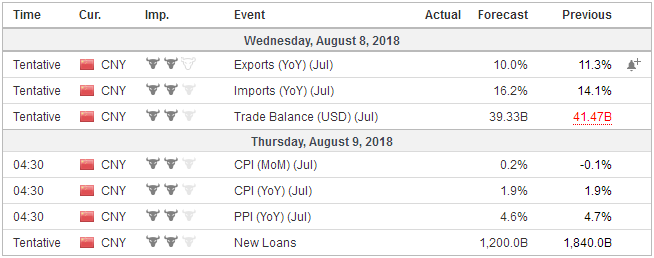

ChinaThe PBOC decision after the local markets closed to reimposed a reserve requirement on yuan forwards is an important signal of its displeasure with yuan weakness. To blunt the strength of the yuan in 2015, Chinese officials had dropped the reserve requirement, by reimposing it they are hoping to deter yuan sales. Moreover, using such tools, which change the incentive structure, are seen as preferable and an evolution of earlier practices that relied on command. The US is threatening to ratchet the pressure higher by 1) raising the tariffs to 25% on the $200 bln of imports from China, which could be implemented in a few weeks, and 2) putting a tariff on nearly all of the imports from China or around $500 bln. China has taken several important steps to offset the economic hit that is expected by the escalating trade conflict with the US. Fiscal and monetary levers have been used, and there is scope for more, if necessary. The required reserve ratio is still high, and there is scope for broad and targeted reductions, for example. Given what China has done to Japan and South Korea in previous disputes, its response to the US provocations has thus far has been quite measured. It is if officials may be having difficulty reading the US Administration. Like King Priam of Troy, who was told that bringing the Horse into the city walls would lead the fall of Troy, Trump has been warned by nearly everyone apparently, but his inner circle, that the tariffs will not get China to capitulate to US demands. And more. It will be disruptive to the US economy. Controversially, the White House committed $12 bln to help some farmers hit by the counter-tariffs. While Chinese officials gird up for a protracted struggle, they have potential inflict considerably more harm and frustrate US aims, such participating in the coming embargo against Iranian oil or pressure on North Korea. However, the recent action seems to lend credence to the declaratory policy of not weaponizing the yuan’s exchange rate. |

Economic Events: China, Week August 02 - Click to enlarge |

Switzerland |

Economic Events: Switzerland, Week August 02 - Click to enlarge |

China has an active economic schedule in the coming days. The weakness in Chinese shares (Shanghai Composite off 8% in July) and the (nearly 3%) depreciation of the yuan suggests China likely experienced capital outflows. This suggests a decline in reserves is likely. China also reports July trade figures. The contrast with America is stark. The US trade deficit rose by $19.6 bln in the first half or 7.2% year-over-year. China’s trade surplus fell by about 25% in dollar terms (nearly 27% in yuan terms) to $138.6 bln in H1 18 from almost $185 bln in H1 17. American policymakers and the economists that drink from the same cup may complain about Chinese trade practices like they complained about Japanese trade practices 30-40 years ago (and not without merit), but a smaller Chinese surplus, like a smaller Japanese surplus, does not necessarily translate into improvement in the US trade balance.

China will publish its latest inflation figures. The stability of China’s CPI (like GDP) stretches its credibility. For the last 12, 24, and 36 months, China’s CPI has averaged 1.8%. It has also averaged 1.8% over the past three months. It is poised to firm. The June increase of 1.9% is expected to be followed by a 2.0% pace in July. Producer price inflation peaked early last year at 7.8% and have trended lower since. The year-over-year pace is expected to slow to 4.5% in July from 4.7% in June. The takeaway from China’s inflation report is not so much about price pressures but that officials have scope to provide more stimulus is needed.

In a similar vein, the lending data may show that the shadow banking challenge has been addressed, at least for the time being, which allows policymakers to focus on other priorities. The difference between aggregate financing and yuan loans is a proxy for shadow banking. In May and June yuan loans were greater than aggregate financing. It was the first back-to-back occurrence since 2008. July may be the third consecutive month.

Capital struck against Italy in late May when the new government initially wanted to give a eurosceptic the finance portfolio. Interest rates shot up. Market pressure and the bold action by Italy’s president succeeded in forcing the government to retreat. At the end of last week, as the budget initiatives came back to the fore, capital again struck. The 10-year yield briefly traded back above 3.0%. Although the yield eased back to a little below 2.93%, it still finished up 18 bp on the week after increasing 15 bp the week before. Salvini is pressing hard for an income tax cut, which of course helps those with legitimate income and a job. Di Maio is pushing hard for a new transfer scheme seeks to help those without jobs and who may not be in the labor market proper.

The confrontation with the EC looks to shaping up in September. The top four rating agencies assign the equivalent to BBB to Italy. Moody’s indicated in late May that it was reviewing Italy’s credit rating due to significant risk to its fiscal position. A decision is expected in September, and a downgrade seems likely. Fitch will update its assessment at the end of the month and S&P review in October. Given that S&P unexpected upgraded Italy’s credit rating in last October and negative review, let alone a rate cut, seems unlikely.

Full story here Are you the author?Tags: #USD,$CNY,$EUR,Italy,Japan,newslettersent,U.K.