Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

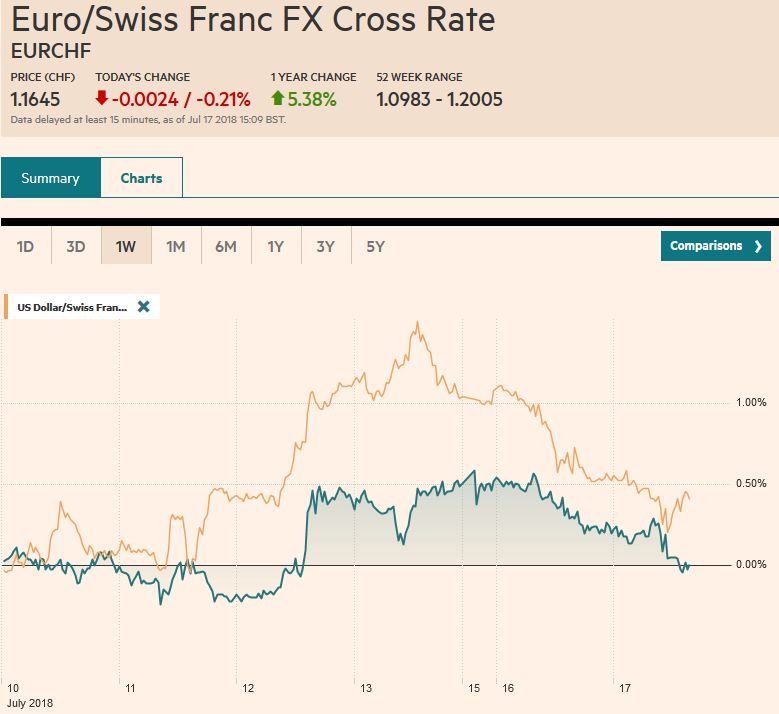

Swiss FrancThe Euro has fallen by 0.21% to 1.1645 CHF. |

EUR/CHF and USD/CHF, July 17(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

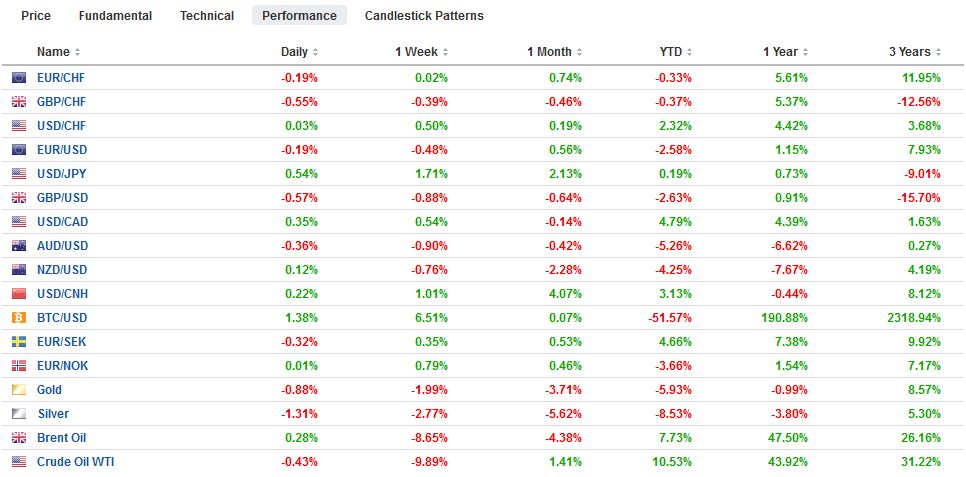

FX RatesThe US dollar eased in Asia session and the European morning. The greenback had appeared technically vulnerable, and the economic news stream is light. Sterling, unlike most of the other major currencies, remains within yesterday’s range. Yesterday’s high, a little above $1.3290, maybe reinforced a little today by the GBP245 mln $1.33 option that is expiring. Brexit concerns may also be acting as a drag. At first, it looked like Prime Minister May was going to block the amendments to the Trade Bill. Even the sponsor did not expect them to pass. However, May instead chose to accept them. The dollar has been confined to a 20 tick range on either side of JPY112.40. After breaking higher last week, a consolidative phase has unfolded. Support is seen a little below JPY112.00. It has not been below JPY111.90 since initially pushing through the JPY112 level last Wednesday. There is a $590 mln option at JPY112.50 that will be cut today. |

FX Performance, July 17 - Click to enlarge |

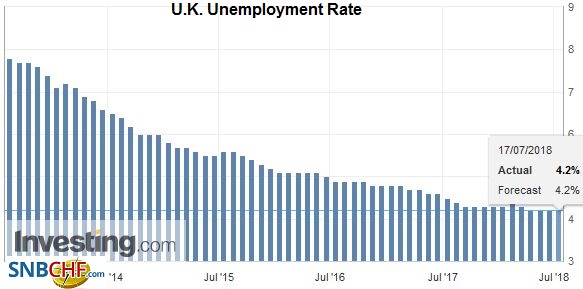

United KingdomThe UK employment data were in line with expectations. The unemployment rate was steady at 4.2% in May, and the average weekly earnings rose 2.5%. The three-month employment change of 137k was only slightly lower than the April pace of 146k and better than the 115k economists expected. There is nothing in the report, or in BOE Governor Carney’s testimony today, that gives any reason for investors to have second thoughts about the likelihood of a rate hike at the next MPC meeting on August 2. |

U.K. Unemployment Rate, Aug 2013 - Jul 2018(see more posts on U.K. Unemployment Rate, ) Source: investing.com - Click to enlarge |

The situation seems rather chaotic, at least from afar, and it is not clear how things will shake out. The decisive battle within the Tory Party has yet to be fought. It continues to appear that the signatures of Tory members needed to trigger a leadership challenge, and even if one is triggered, it is not obvious that May would be defeated. The underlying point is that while there may be dislike for the status quo, there is no agreement on the alternative or the way forward.

The New Zealand dollar is leading the charge today against the greenback, with only the yen not participating. The Kiwi was lifted by strong underlying inflation. The sectoral report showed inflation at a seven-year high near 1.7% in Q2, after the year-over-year increase in the headline rate accelerated to 1.5% from 1.1%. The low from last week was recorded ahead of the weekend near $0.6725. It traded up to $0.6840 today. The $0.6860 area capped it earlier this month. A move above there would open the door to a return to the $0.6950 area seen in late June.

The Australian dollar is lagging behind. Even though the Reserve Bank of Australia reinserted a line that had been dropped last month that indicated that the next move in rates is likely higher, the Aussie is little changed. Tomorrow Australia reports its employment data. A break of NZD1.0835 could confirm a double top in place, and signal a move into the NZD1.0650 area, where the Aussie had bottomed in mid-June.

Many markets in Asia fell today, led by Hong Kong’s 1.25% decline. China, Taiwan, Korean, Thai, and Indonesian shares fell. Japan, returning from a long holiday weekend, saw the Nikkei raise almost 0.5% and the Topix nearly 0.9%. Utilities, consumer staples, and financials led the advance. The energy sector traded heavily after oil fell sharply. Excluding Japan, the MSCI Asia Pacific Index was off 0.35%, the second day of losses. With Japanese shares, the MSCI Asia Pacific index eked out less than a 0.1% gain.

European stocks are faring the same. The Dow Jones Stoxx 600 is up less than 0.1% near midday on the Continent. Materials are leading the way, as the sector gains more than 1%. Industrials and financials are also pulling higher. Telecoms are off 1.2%, and utilities and real estate sectors are softer. The euro is trading quietly higher and is approaching a five day high. So far, today is the first session since last Monday that the euro has not traded below $1.17.

Oil prices dropped more than 4% yesterday and are struggling to stabilize today. News that Saudi Arabia increased the oil offered to a couple Asian buyers for August was part of a larger story that can be summed up by saying that concerns about supply disruptions eased, including the re-opening of Libyan parts and an expected to soon return of some Canadian oil. There is also talk that the US may tap its strategic reserves, though a decision does not look imminent. The $68 a barrel level may offer a technical base for August WTI. It is a 61.8% retracement of the rally from mid-June (~$63.60) to the recent high (July 3, ~$75.25). That said, the technical indicators warn of the risk of a deeper correction.

The focus in the US session turns to Powell’s testimony before a Senate Committee. His prepared remarks have already been released. The interest then is on the questions and answers. The issues that may interest investors most related to the number of hikes (median dot in June was for four hikes this year after one member changed their forecast) and the shape of the curve. The flatness of the curve and the risk of inversion is giving the doves on the Fed new reasons to temper the pace. However, within the context of negative interest rates abroad, the issuance of the debt management office, and the fiscal stimulus, several Fed officials have played down the recessionary implications. There is also bound to be a discussion of the impact of the tariffs on the US economy. Powell’s views are clear. There is already some impact on business sentiment, and it could impact CapEx plans.

The US will report industrial output, which is expected to bounce back from a 0.1% decline in May. Manufacturing should recover the 0.7% decline. Capacity utilization rates may reach a new three-year peak above 78%. After the markets close, the May TIC data and API oil inventory estimate will be released. Through April, the US imported an average of $67.38 bln a month according to the TIC data. In the same period last year, the average was $54.35 bln and in 2016, the average in the Jan-April period was $34.5 bln.

Full story here Are you the author?

Tags: #GBP,#USD,$AUD,$EUR,$JPY,EUR/CHF,newslettersent,NZD,U.K. Unemployment Rate,USD/CHF