Jeffrey P. Snider

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

Thomas Hoenig was President of the Federal Reserve’s Kansas City branch for two decades. He left that post in 2011 to become Vice Chairman of the FDIC. Before that, Mr. Hoenig as a voting member of the FOMC in 2010 cast the lone dissenting vote in each of the eight policy meetings that year (meaning he was against QE2, too). This makes him, apparently, the hawk of all hawks.

In January 2011, in his capacity as still President in the Kansas City branch, Hoenig told an audience in Kansas City that though he was no longer a voting member of the Committee (he had starting in 2011 rotated off as regional branch presidents do) his same concerns remained.

As we begin 2011, recent economic data indicate a firmer tone in the outlook, and I am increasingly confident that the recovery is both sustainable and likely to gain strength over the next several quarters.

The primary danger to his outlook as he saw it then was the fiscal deficit. As to the other, he said, “A second concern I have is the consequences that will follow when we combine our current fiscal projections with a highly accommodative monetary policy.” The issue for him was, as in 2010, lags. According to his view, the FOMC was in danger of not thinking far enough ahead. They were being too cautious and risked letting inflation run wild given how much stimulus, so called, had been invented and introduced.

am pleased to be able to say that in my view the economy is in recovery, although at a moderate pace. Over time, barring unexpected surprises, the recovery should gain momentum, which will encourage hiring and slowly bring down the unemployment rate. About that, “unexpected surprises” were just around the corner. Merely a few months forward, the BEA would show that the US economy had already entered a downturn (as Hoenig was speaking) and ultimately the global eurodollar system would experience another major crisis that summer. And during that near-panic, the FOMC would carry on deliberations stunned, truly bewildered not just that it was happening but that something so serious ever could given so much presumed liquidity and “money printing.”

We all know in economics that policy actions or anything for that matter has lagged effects. A shock doesn’t cause immediate collapse, nor does an actual rather than imagined injection of money. The 2008 panic wasn’t just those two weeks in early October, it had really started the prior August and wouldn’t end until the following March.

But the idea of lags has become like so many other terms bastardized to fit the current circumstances; or, more accurately, to excuse contemporary conditions for how they don’t conform wrapped into the idea that they will tomorrow given enough time. Like the word “transitory”, this is taking “lag” way too far. From yesterday in Japan: Fears over the future of Abenomics are mounting at a time when the BOJ is finally beginning to see the results of five years of its ultra-loose policy stance.

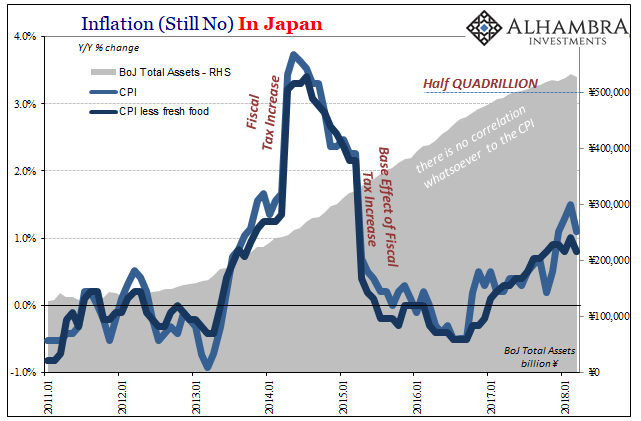

For those keeping score, the Bank of Japan has engaged in constant and massive LSAP’s for more years than anyone could have ever imagined. They began to take on the most absurd proportions in 2013, five years ago, with the intrusion of QQE. The idea was positively Krugman-esque, the mythical S-curve jump to be created by this doctrine of credibly promise to be irresponsible. As of the end of Marcy 2018, BoJ has obtained total assets of ¥528.5 trillion. Half a quadrillion.

Inflation in Japan, Jan 2011 - Apr 2018

(see more posts on Japan Consumer Price Index / Inflation, )- Click to enlarge

Can five years still be considered under any lagged effect? And not yet to actual success, but, as the quote above points out, the possibility that it is “finally beginning.” So much time has passed, half a decade, are we not way, way beyond cause and effect? The article was also written a day too early. The setbacks it described was not the CPI, but the yen’s recent strength and Abe’s mounting political scandals which might imperil the current monetary policy.

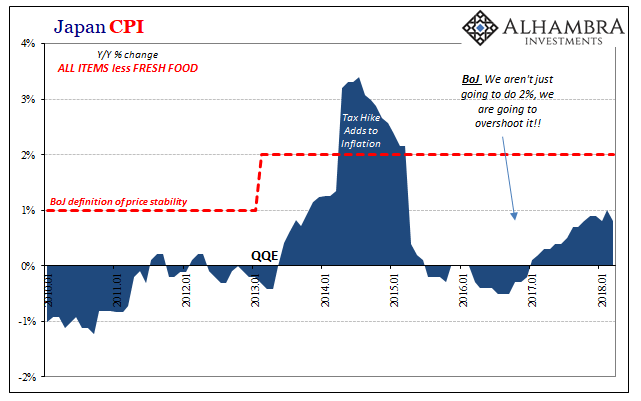

Today, the Ministry of Internal Affairs reports Japanese consumer prices fell -0.4% month-over-month, bringing the CPI back down to just 1.1% year-over-year, leaving it still only about halfway to its target. Excluding fresh food prices, the Japanese “core” rate was less than 1% yet again.

Japan Consumer Price Index, Jan 2010 - Apr 2018

(see more posts on Japan Consumer Price Index / Inflation, )- Click to enlarge

Obviously, this is a problem not unique to Japan. It’s as if the island chain’s “deflationary mindset” has been its chief export since 2008. None of the central banks around the world seem able to answer for the persistent undershoot (if they ever do, then they might then be able to tackle the more important and related issue of global Japanification). Comically enlarged lags, obliterating the word “transitory”, persistent questions about inflation despite trillions and maybe even quadrillions, these are all signs and evidence of the same thing. Ben Bernanke at Thomas Hoenig’s Jackson Hole Symposium in 1999:

The principal conclusion of this paper has been stated several times. In brief, it is that flexible inflation-targeting provides an effective, unified framework for achieving both general macroeconomic stability and financial stability. Given a strong commitment to stabilizing expected inflation, it is neither necessary nor desirable for monetary policy to respond to changes in asset prices, except to the extent that they help forecast inflationary or deflationary pressures.

Japan Consumer Price Index, Jan 2010 - Apr 2018

(see more posts on Japan Consumer Price Index / Inflation, )- Click to enlarge

Think about what he said except in the contrary where the first part of that quote is wrong. What if it didn’t matter what or how much any central bank did as what it calls “stimulus” because what followed over a period of years, half or even a full decade, was macroeconomic and financial instability? It would rewrite not just what’s going on today, but what’s gone on for decades (from bubbles to conundrums).

With so many tested varieties in so many different geographical locations, the wide range of QE’s and LSAP’s have shown, proved actually, central bankers have no idea how to influence inflation. And given that inflation is always and everywhere a monetary phenomenon, monetary policy has no connection with money.

Or, maybe it really is just one enormous lag, and Thomas Hoenig’s concerns were just a little early. Seven years early.

Full story here Are you the author?Previous post See more for Next postJeffrey P. Snider is the head of Global Investment Research of Alhambra Investment Partners (AIP). Jeffrey was 12 years at Atlantic Capital Management where he anticipated the financial crisis with critical research. His company is a global investment adviser, hence potential Swiss clients should not hesitate to contact AIP

Tags: Abenomics,Bank of Japan,CPI,currencies,economy,Federal Reserve/Monetary Policy,inflation,Japan,Japan Consumer Price Index / Inflation,lsap,Markets,Monetary Policy,money,newslettersent,QE,QQE

Permanent link to this article: https://snbchf.com/2018/05/snider-transitorys-japanese-cousin/

On Swiss National Bank

SNB Sight Deposits: decreased by 2.2 billion francs compared to the previous week

Household wealth in 2025

Heads up for NZD and CHF traders, RBNZ Gov Breman and SNB Chair Schlegel to speak

Swiss franc appreciation has led to tighter monetary conditions – SNB minutes

SNB’s Chairman Schlegel: A few months of negative inflation wouldn’t be a problem

Featured and recent

SNB Sight Deposits: decreased by 2.2 billion francs compared to the previous week

SNB Sight Deposits: decreased by 2.2 billion francs compared to the previous week Corrections vs. Bear Markets: Why 20% Declines Are Obsolete

Corrections vs. Bear Markets: Why 20% Declines Are Obsolete -40 Kilo! Ricarda Lang feiert Abnehmerfolg! Das Internet feiert!

-40 Kilo! Ricarda Lang feiert Abnehmerfolg! Das Internet feiert! Steuerrecht digitalisieren mit KI – eine gute Idee?

Steuerrecht digitalisieren mit KI – eine gute Idee? Why Switzerland is launching a charm offensive in Southeast Asia

Why Switzerland is launching a charm offensive in Southeast Asia Ex-Raiffeisen bank CEO fined for tax evasion

Ex-Raiffeisen bank CEO fined for tax evasion The price of gold matters, but availability matters more.

The price of gold matters, but availability matters more. FATAL: EU Chefdiplomatin blamiert ganz Europa! China außer sich!

FATAL: EU Chefdiplomatin blamiert ganz Europa! China außer sich! India’s situation shows why physical gold is different from paper exposure.

India’s situation shows why physical gold is different from paper exposure. ZUGRIFF auf dein Vermögen: So schützen sich INSIDER

ZUGRIFF auf dein Vermögen: So schützen sich INSIDERMore from this category

Monthly Macro Monitor: A Lot Of Noise, Little Effect

27 Apr 2026

Weekly Market Pulse: The Only Free Lunch In Investing

13 Apr 2026

- Market Volatility Strategies For Investors

1 Jan 2026

- Inflation as a moral hazard

19 Dec 2025

- Gold’s flashing warning: The end is nigh for fiat

4 Nov 2025

Investor Dilemma: Pavlov Rings The Bell – Draft

3 Nov 2025

- A conversation with Catherine Austin Fitts

10 Oct 2025

Weekly Market Pulse: An Energetic Market

18 Sep 2025

Invest Or Index – Exploring 5-Different Strategies

15 Sep 2025

Weekly Market Pulse: Big Rate Cuts? Not Right Now

18 Aug 2025

- Geopolitical theater and implications for investors (or lack thereof)

11 Jul 2025

Annuities Are Not Your Enemy.

3 Jul 2025

Weekly Market Pulse: The Turkey Leg

23 Jun 2025

Weekly Market Pulse: No Free Lunches

19 May 2025

Weekly Market Pulse: On The Road Again

12 May 2025

Allow Chinese Companies to Build Locally and Sell Locally or Face Dire Consequences

7 May 2025

Speculator Or Investor? 10-Rules From Legendary Investors

25 Apr 2025

Weekly Market Pulse: Peak America?

21 Apr 2025

- Silver: A rare buying opportunity

7 Apr 2025

Weekly Market Pulse: Tune Out The Noise

24 Feb 2025