Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

You Don’t Have To Take My Word For It About Eliminating QE

You Don’t Have To Take My Word For It About Eliminating QE24 Oct 2021

August Avoids Zero In JGB’s28 Sep 2021

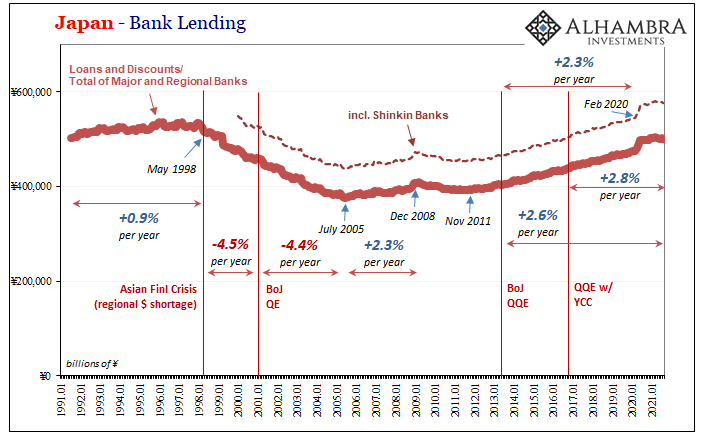

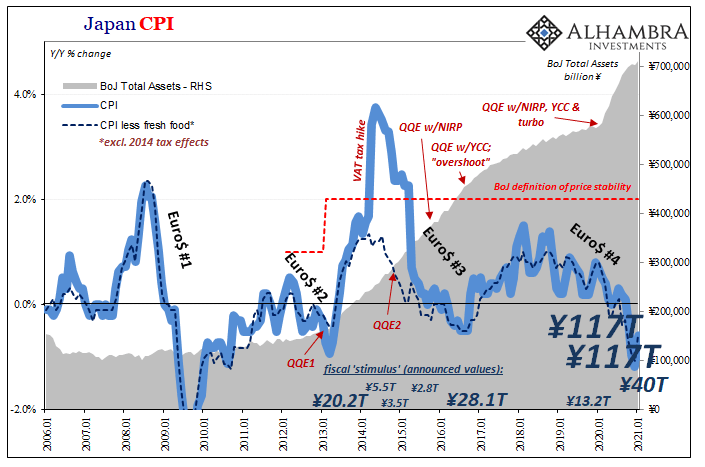

Nine Percent of GDP Fiscal, Ha! Try Forty25 Feb 2021

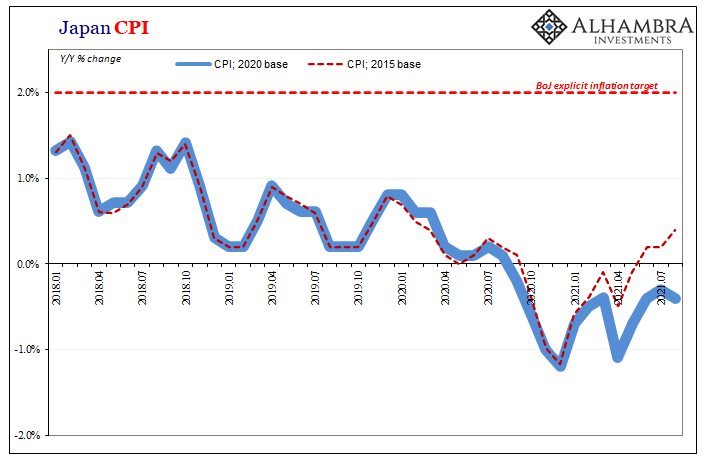

Deflation Returns To Japan, Part 223 Nov 2020

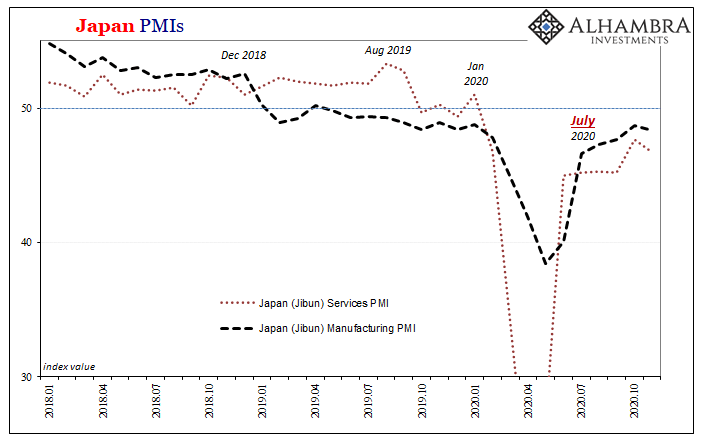

Looking Ahead Through Japan30 Jun 2020

From QE to Eternity: The Backdoor Yield Caps4 Jun 2020

There Was Never A Need To Translate ‘Weimar’ Into Japanese

There Was Never A Need To Translate ‘Weimar’ Into Japanese17 May 2020

What Happens When Central Banks Buy Stocks (ETFs)? Well, We Already Know13 Mar 2020

ISM Spoils The Bond Rout!!!3 Oct 2019

Effective Recession First In Japan?16 May 2019

What Tokyo Eurodollar Redistribution Really Means For ‘Green Shoots’2 May 2019

Something Different About This One22 Feb 2019

Lost In Translation8 Feb 2019

Economics Is Easy When You Don’t Have To Try11 Dec 2018

And Now For Something Completely Different20 May 2018

Transitory’s Japanese Cousin1 May 2018

The Best ‘Reflation’ Indicator May Be Japanese4 Apr 2018

The Global Burden12 Apr 2017

Systemic Depression Is A Clear Choice5 Apr 2017

True Cognitive Dissonance4 Mar 2017