There is clearly a common denominator in the kind of “solutions” that the State comes up with to deal with the problems that it caused (and that’s most problems). Not only are these remedies worse than the disease, but they are always extremely simplistic, reductionist and they never, ever, take into account anything else apart from the political “optics” and the populistic value of each new measure or piece of legislation. There is no...

Read More »

Tag Archive: QE

Weekly Market Pulse: First, Kill All The Speculators

Read More »

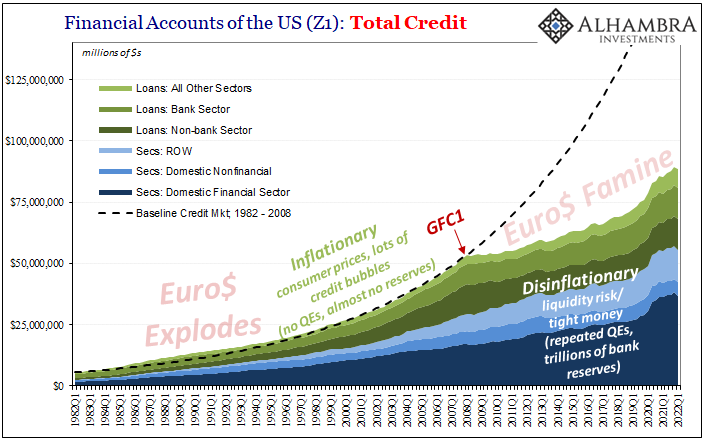

The Everything Data’s (Z1) Verdict: Not Inflation, Only More Of The Same

Read More »

Collateral Shortage…From *A* Fed Perspective

Read More »

I Told You It *Wasn’t* Money Printing; How The Fed Helped Cause, But Can’t Solve, Our Current ‘Inflation’

Read More »

Goldilocks And The Three Central Banks

Read More »

The Hawks Circle Here, The Doves Win There

Read More »

Start Long With The (long ago) End of Inflation

Read More »

Weekly Market Pulse: Has Inflation Peaked?

Read More »

Weekly Market Pulse: Discounting The Future

Read More »

What Does Taper Look Like From The Inside? Not At All What You’d Think

Read More »

The Real Tantrum Should Be Over The Disturbing Lack of Celebration (higher yields)

Read More »

Bill Issuance Has Absolutely Surged, So Why *Haven’t* Yields, Reflation, And Other Good Things?

Read More »

The Curve Is Missing Something Big

Read More »

The Great Eurodollar Famine: The Pendulum of Money Creation Combined With Intermediation

Read More »

Tapering Or Calibrating, The Lady’s Not Inflating

Read More »

August Avoids Zero In JGB’s

Read More »

Taper *Without* Tantrum

Read More »

Rechecking On Bill And His Newfound Followers

Read More »

The Endangered Inflationary Species: Gazelles

Read More »

On Swiss National Bank

On Swiss National Bank

-

SNB Sight Deposits: decreased by 2.2 billion francs compared to the previous week

-

Household wealth in 2025

-

Heads up for NZD and CHF traders, RBNZ Gov Breman and SNB Chair Schlegel to speak

-

Swiss franc appreciation has led to tighter monetary conditions – SNB minutes

-

SNB’s Chairman Schlegel: A few months of negative inflation wouldn’t be a problem

Main SNB Background Info

Featured and recent

-

SNB Sight Deposits: decreased by 2.2 billion francs compared to the previous week

SNB Sight Deposits: decreased by 2.2 billion francs compared to the previous week -

Corrections vs. Bear Markets: Why 20% Declines Are Obsolete

Corrections vs. Bear Markets: Why 20% Declines Are Obsolete -

-40 Kilo! Ricarda Lang feiert Abnehmerfolg! Das Internet feiert!

-40 Kilo! Ricarda Lang feiert Abnehmerfolg! Das Internet feiert! -

Steuerrecht digitalisieren mit KI – eine gute Idee?

Steuerrecht digitalisieren mit KI – eine gute Idee? -

Why Switzerland is launching a charm offensive in Southeast Asia

Why Switzerland is launching a charm offensive in Southeast Asia -

Ex-Raiffeisen bank CEO fined for tax evasion

Ex-Raiffeisen bank CEO fined for tax evasion -

The price of gold matters, but availability matters more.

The price of gold matters, but availability matters more. -

FATAL: EU Chefdiplomatin blamiert ganz Europa! China außer sich!

FATAL: EU Chefdiplomatin blamiert ganz Europa! China außer sich! -

India’s situation shows why physical gold is different from paper exposure.

India’s situation shows why physical gold is different from paper exposure. -

ZUGRIFF auf dein Vermögen: So schützen sich INSIDER

ZUGRIFF auf dein Vermögen: So schützen sich INSIDER

More from this category

- Debt cancellation: the new panacea?

9 Jun 2023

Weekly Market Pulse: First, Kill All The Speculators

Weekly Market Pulse: First, Kill All The Speculators31 Jan 2023

- The Everything Data’s (Z1) Verdict: Not Inflation, Only More Of The Same

26 Jun 2022

- Collateral Shortage…From *A* Fed Perspective

7 May 2022

- I Told You It *Wasn’t* Money Printing; How The Fed Helped Cause, But Can’t Solve, Our Current ‘Inflation’

21 Apr 2022

- Goldilocks And The Three Central Banks

7 Apr 2022

- The Hawks Circle Here, The Doves Win There

26 Jan 2022

- Start Long With The (long ago) End of Inflation

24 Dec 2021

Weekly Market Pulse: Has Inflation Peaked?

Weekly Market Pulse: Has Inflation Peaked?13 Dec 2021

- Weekly Market Pulse: Discounting The Future

7 Dec 2021

- What Does Taper Look Like From The Inside? Not At All What You’d Think

5 Nov 2021

- The Real Tantrum Should Be Over The Disturbing Lack of Celebration (higher yields)

3 Nov 2021

- Bill Issuance Has Absolutely Surged, So Why *Haven’t* Yields, Reflation, And Other Good Things?

2 Nov 2021

- The Curve Is Missing Something Big

21 Oct 2021

- The Great Eurodollar Famine: The Pendulum of Money Creation Combined With Intermediation

13 Oct 2021

- Tapering Or Calibrating, The Lady’s Not Inflating

7 Oct 2021

- August Avoids Zero In JGB’s

28 Sep 2021

- Taper *Without* Tantrum

17 Aug 2021

- Rechecking On Bill And His Newfound Followers

9 Apr 2021

- The Endangered Inflationary Species: Gazelles

11 Feb 2021