Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

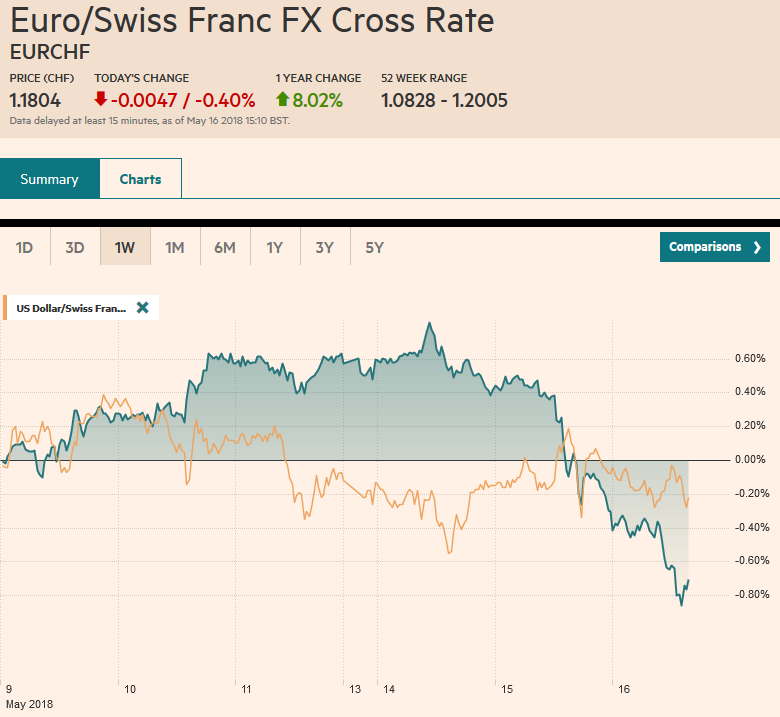

Swiss FrancThe Euro has fallen by 0.40% to 1.1804 CHF. |

EUR/CHF and USD/CHF, May 16(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe US dollar is mixed today after the Dollar Index rose to new 2018 highs yesterday. It is being driven by rising US rates, which also punishes short dollar positions. The US 10-year yield rose seven basis points yesterday to nearly 3.10%. It is consolidating near 3.06% now. Many see the yield rising toward 3.20%, which would match the mid-2011 high. The two-year yield continues to march higher as well. It rose three basis points yesterday to 2.57% and is flat today. Part of the rise at the short-end reflects expectations about the trajectory of Fed policy. For example, if the Fed were to hike rates three more times this year, it would put the average effective rate for Fed funds near 2.45% (allowing the Fed funds rate to trade as it is now at the firm end of the target range). The implied yield on the January contract is 2.3055%. This implies about a 42% chance of a fourth hike this year. That is nearly double the odds before the April jobs data that kicked off this months reports. The implied yield has risen six basis points this month. The two-year note yield has risen by nine basis points during the same time. |

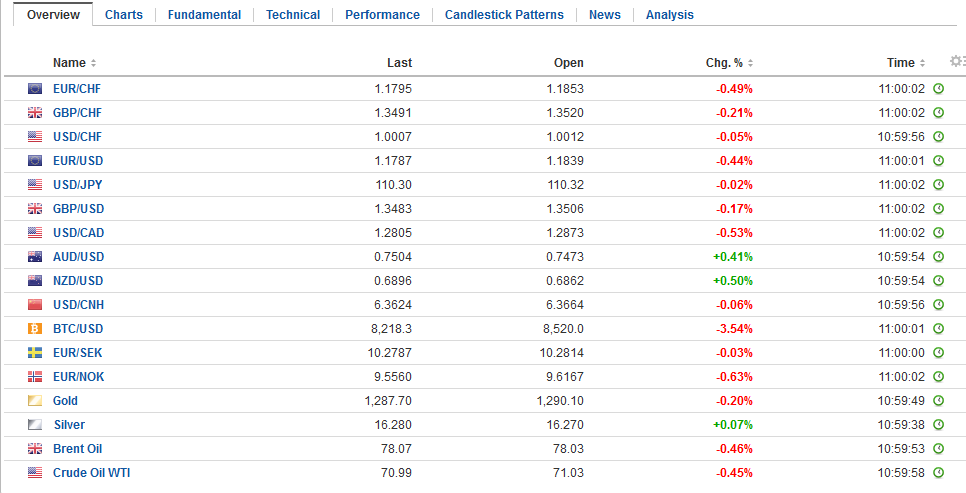

FX Daily Rates, May 16 - Click to enlarge |

| This is to say a good part of the backing up of short-term rates is a function of rising confidence of the Fed’s course. At the start of the week, we suggested that the rise in the US-German interest rate differential could be explained by the diverging inflation performances in recent months. There was nothing particularly worrisome in the yesterday’s April retail sales report, but the components used for GDP purposes was firm at 0.4% following the upward revision in the March series to 0.5%. The Empire Manufacturing Index also was reported at the same time and was stronger than expected. We argue that the Federal Reserve more than other major central banks can look through practically any soft high-frequency data and be confident that its mandates can be achieved. They are within spitting distance now, and there is the large fiscal stimulus in the pipeline.

The bounce in the euro met a wall of selling in front of $1.20. We had thought there was a bit more potential. Now the euro is threatening the $1.1800 level. The next important area is a cent lower. The $1.1700 area corresponds to a 38.2% retracement of the euro’s gains since early last year. |

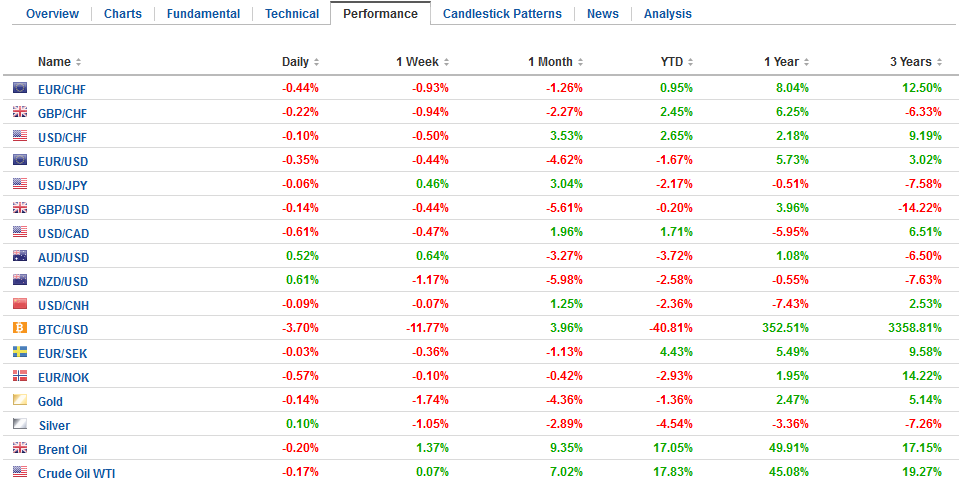

FX Performance, May 16 - Click to enlarge |

Japan

Compare that with the simply awful Japanese GDP figures. We flagged the risk of a negative report and the end to the two-year expansion. The world’s third-largest economy contracted by 0.2% in Q1 18, and adding to the disappointment, growth in Q4 17 was slashed to 0.1% from 0.4%. That means net-net the Japanese economy has contracted over the past six months. The downward revision was driven by private consumption, which was cuts to 0.2% from 0.5%, and business spending, which rose 0.6% rather than 1.0%. The one bright spot, the rise in the GDP deflator to 0.5% from a revised flat reading in Q4 17. While the BOJ may desire higher inflation, the immediate impact is to translate into a 0.4% contract in nominal growth.

Meanwhile, the government is putting together some fiscal measures, like cutting taxes on autos and homes to help support the economy through the retail sales tax hike in October 2019 (from 8% to 10%). There is also some talk of a new tax based on the fuel efficiency of vehicles.

The yen hardly responded to the news. It seems to be taking its cues from US yields. That said, note that the March TIC data showed that Japanese investors continue to reduce their Treasury holdings. Outside of January, they have been divesting Treasury holdings since last July. In the first seven months of 2017, Japanese investors were net buyers for five months. Their Treasury holdings have fallen by about $70 bln since last July, with $16 bln drawdowns reported in March. There is a $590 mln JPY110.50 option that expires today. The move above JPY110 negates the potential double top pattern.

Italy

A report that played up the more confrontational approach by the Five Star Movement (M5S) and the (Northern) League spurred investor anxiety, which is weighing on Italian assets today. The yield on the 10-year bond is up seven basis points and is above 2% for the first time in a couple of months. Other peripheral yields on edging higher, but the core is pulling back one to two basis points in line with US Treasuries. The Italian stock market is off 1.4%. Most markets are lower but not nearly as much. The Dow Jones Stoxx 600 is- off less than 0.1%. Italian shares are snapping a three-day advance. The technical tone is poor and a close below the 20-day moving average, for the first time since early April may signal a more sustained 3%-5% pullback, which would dent this year’s still-impressive 9.6% gain.

Emerging market hotspots remain in focus. The Malaysian ringgit is off for a sixth session. Since April 11, it has appreciated in only two sessions. The Turkish lira is lower for a fourth session and is plumbing new record lows. The Argentine peso’s performance after yesterday’s Lebac sales (38%-40%) will be monitored. There is some thought that an extreme may be near. A couple of large US-based funds reportedly were large buyers at yesterday’s debt sales. The central bank appears to have sold around $1.2 bln so far this week to absorb the peso sales. It may have also intervened in the futures market, according to some reports.

United States

The US reports April housing starts and industrial production figures. Housing starts and permit may pare March’s gain, and the headline industrial output is at risk of a drop in utilities. The signal comes from manufacturing. It averaged 0.4% in Q1, and the median forecast in the Bloomberg survey was for a 0.5% gain in April. The Fed’s Bostic speaks before the US equities open, while Bullard speaks after the close. Canada reports March manufacturing sales.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$EUR,$JPY,$TLT,Emerging Markets,EUR/CHF,FX Daily,Italy,newslettersent,USD/CHF