Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

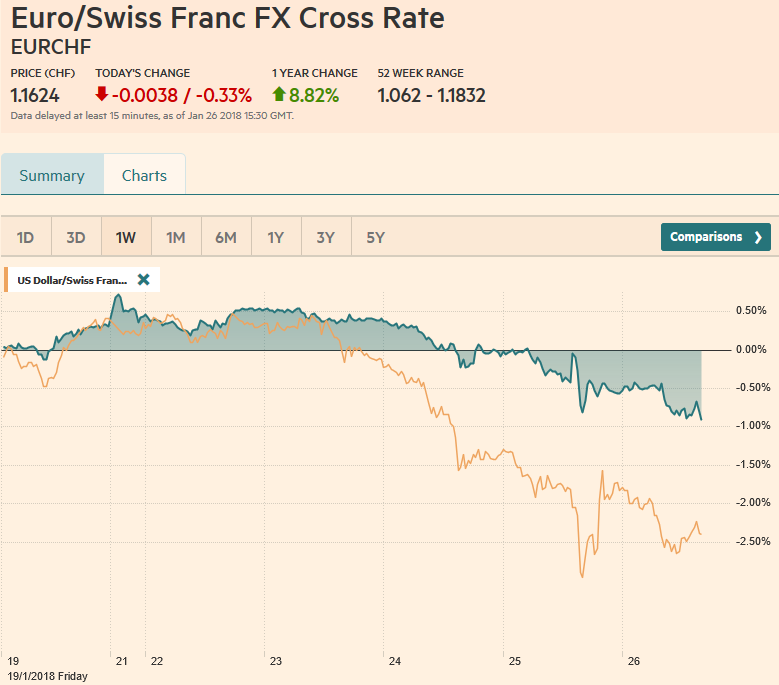

Swiss FrancThe Euro has fallen by 0.33% to 1.1624 CHF. |

EUR/CHF and USD/CHF, January 26(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

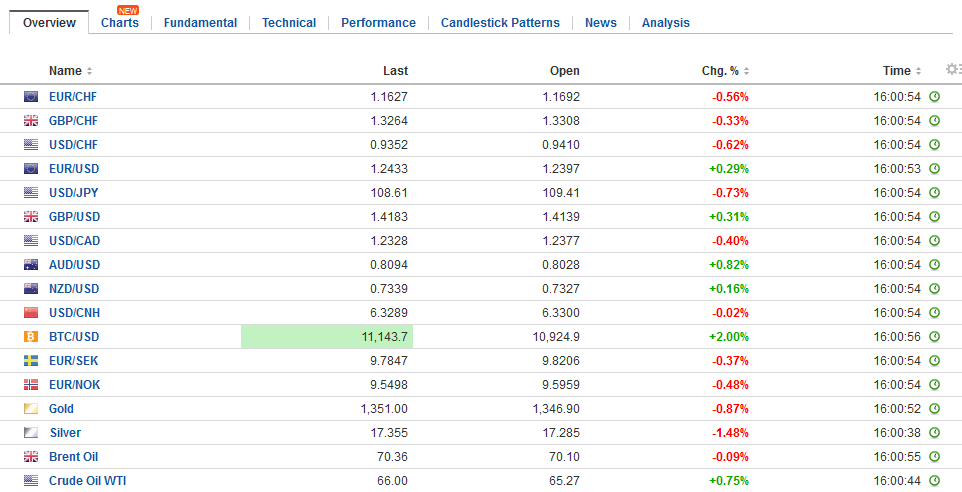

FX RatesIt was dramatic. Following the BOJ and ECB’s rather mild rebuke of dollar’s depreciation, US President Trump cautioned that his Treasury Secretary comments were taken out of context, and in ant event, he, the President ultimately favored a strong dollar. The dollar, which had continued fall after Draghi’s post-ECB meeting comments, shot higher in the US afternoon in response to Trump’s comments. The market took advantage of the dollar’s recovery to sell it at better levels. The dollar has surrendered more than 61.8% of yesterday’s recovery. Ultimately, market participants realize that policymakers wishes are hardly the stuff that makes for the durable trends that are often apparent in the foreign exchange market. Whether or not US officials want or like a weak dollar in the short-term that is what they have. That said, we look for a consolidative tone to emerge as the market digest the combination of the explosive news stream and the extended positioning. |

FX Daily Rates, January 26 - Click to enlarge |

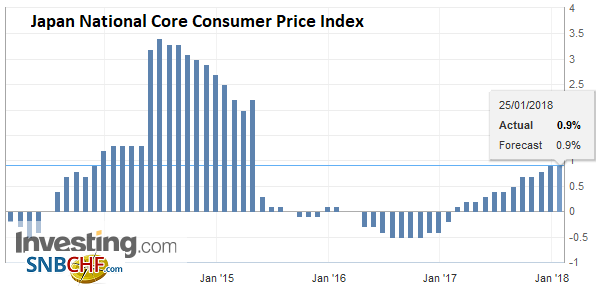

| Fresh developments have been light. The main economic data was Japan’s December CPI. The headline rose from 0.6% to 1.0%. However, this was a function of fresh food and energy. When these items, which may not be sensitive to monetary policy, are excluded the pace was unchanged. The core, which the BOJ targets at 2% remained at 0.9%. Excluding fresh food and energy, more like the US core rate, was unchanged at 0.3%. |

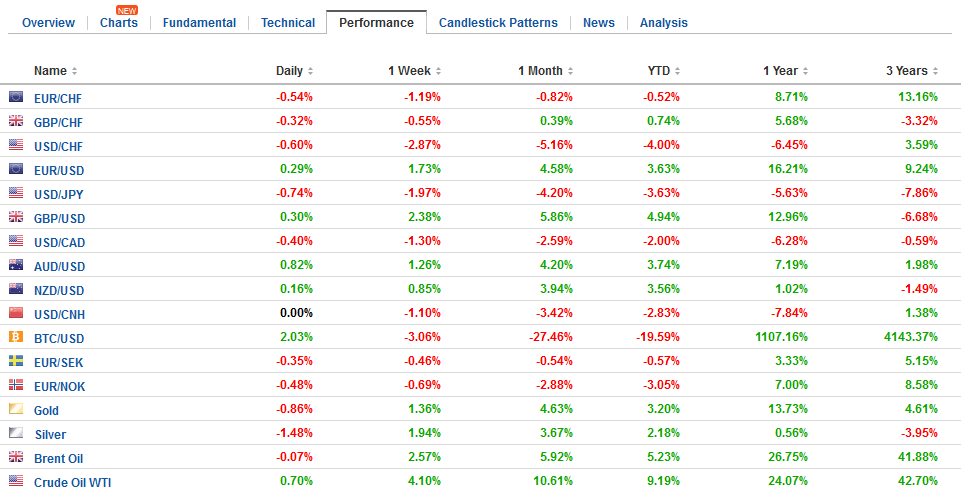

FX Performance, January 26 - Click to enlarge |

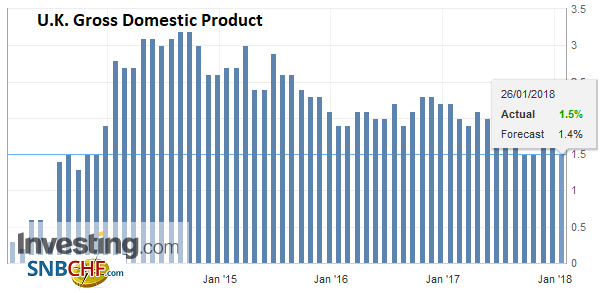

United KingdomThe UK reported its first look at Q4 GDP. It rose slightly more than expected at 0.5%. The year-over-year rate slipped to 1.5% from 1.7%. The last time the year-over-year print was this low was in Q1 13. Details are not provided with the initial estimate, but it does appear that a pick up in services may have been the key to the upside surprise. Sterling, which like the other major currencies, was already moving higher extended its gains. |

U.K. Gross Domestic Product (GDP) YoY, Q4 2017(see more posts on U.K. Gross Domestic Product, ) Source: Investing.com - Click to enlarge |

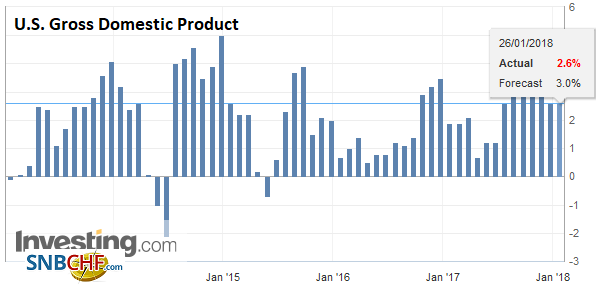

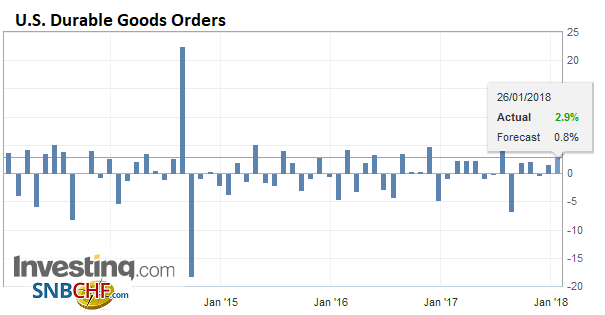

United StatesThe US reports Q4 GDP, and in doing so, renders the other reports today, including the advance merchandise trade balance and durable goods orders less interesting. The Bloomberg survey found a median expectation of 3.0%, but the median has been under-estimating the strength of the US economy–that is what the data surprise models show. |

U.S. Gross Domestic Product (GDP) QoQ, Q4 2017 Source: Investing.com - Click to enlarge |

| The Atlanta Fed’s GDP Now sees 3.4% growth and the NY Fed’s tracker puts it at 3.9%. Consumption is expected recovered smartly in Q4 after a disappointing 2.2% annualized pace was recorded in Q3. Also, quarterly deflator used for consumption is GDP is expected to rise to 1.9%, which would be the strongest pace in 2017. |

U.S. Durable Goods Orders, Dec 2017(see more posts on U.S. Durable Goods Orders, ) Source: Investing.com - Click to enlarge |

Japan |

Japan National Consumer Price Index (CPI) YoY, Dec 2017(see more posts on Japan National Consumer Price Index, ) . |

Japan National Core Consumer Price Index (CPI) YoY, Dec 2017(see more posts on Japan National Core Consumer Price Index, ) Source: Investing.com - Click to enlarge |

|

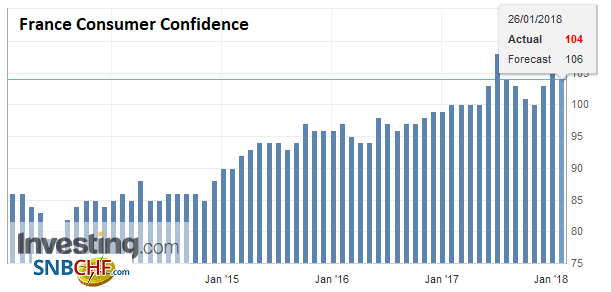

France Consumer Confidence, Jan 2018(see more posts on France Consumer Confidence, ) Source: Investing.com - Click to enlarge |

The North American session features Canada’s CPI and Q4 US GDP. Canada’s CPI is expected to have softened in December. A 0.3% decline would offset a rise of a similar magnitude in November and pull the year-over-year rate back below 2%. Bank of Canada Governor Poloz did not seem particularly hawkish in comments from Davos. Poloz noted that while the exchange rate it is important for exporters, the key is the strength of its main export market, the United States.

The MSCI Asia Pacific Index gave back early gains to finish a hair lower for the second consecutive session. Nevertheless, it extended its advancing streak for a seventh week. Foreigners returned to the Korean market after having been spooked by the MSCI warning against the new capital gains levy that is under consideration. Korea’s KOSDAQ, which has an aggressive agenda of IPOs, gained 1.6% today and to cap a 3.75% gain this week. Led by mainland banks and insurance companies, Hong Kong’s Enterprise Index also remains hot. Today’s 2.5% rally brings the weekly advance a little above 4%. Japanese and Taiwanese shares are the only equity markets in Asia to fall this week.

European shares are higher in the early going. The Dow Jones Stoxx 600 is up about 0.45%, led by health care and consumer discretionary sectors. It needs to rise by a bit more to extend its advancing streak for a fourth week. If not, it will be the first losing week of the year.

Bond yields are narrowly mixed. Peripheral European bonds are still very much in play. Spain has emerged as the clear favorite. Not that it will go there again, but before the crisis, Spain’s 10-year yield had traded briefly through Germany’s 10-year yield. Italian bonds will likely offer a better opportunity later after elections and the challenge it may have in putting a new government in place.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$EUR,$JPY,EUR/CHF,France Consumer Confidence,Japan National Consumer Price Index,Japan National Core Consumer Price Index,newslettersent,U.K. Gross Domestic Product,U.S. Durable Goods Orders,U.S. Gross Domestic Product,USD/CHF