Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

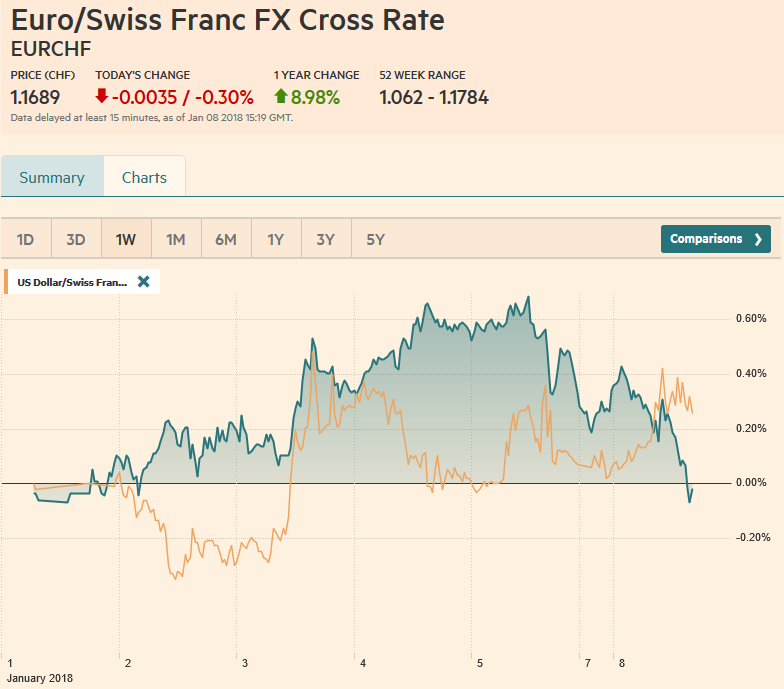

Swiss FrancThe Euro has fallen by 0.30% to 1.1689 CHF. |

EUR/CHF and USD/CHF, January 08(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

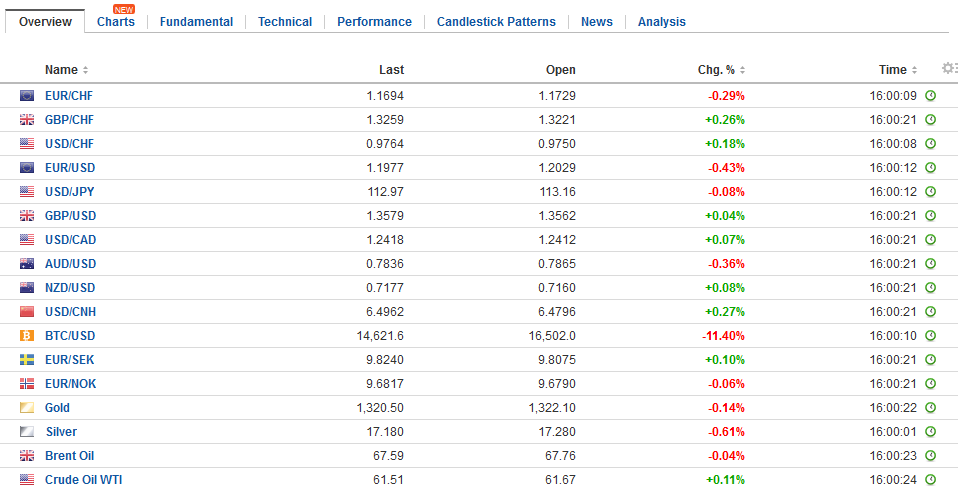

FX RatesThe US dollar is enjoying modest but broad-based gains after trading firmly at the end of last week despite the slightly disappointing jobs report. The dollar’s upticks are understood to be corrective in nature. The Canadian dollar appears to be protected by the increased prospects of a rate hike next week after its stellar employment report. The euro is lower for the second consecutive session. It has not fallen two days in a row since the middle of last month. It is the first session in five that the euro has traded below $1.20. Recall that last week, it had stalled in front of last year’s high. It has tested initial support near $1.1980. The next target is in the $1.1920-$1.1950 area. There is a large option (2.3 bln euros) struck at $1.1985 that expires tomorrow. |

FX Daily Rates, January 08 - Click to enlarge |

| Japan’s markets were on holiday earlier today. The greenback traded to almost JPY113.40 after flirting with JPY112.00 early last week. The dollar has approached the JPY113.65-JPY113.75 area that capped upticks last month. The US 10-year yield, which the exchange rate still seems sensitive to, is near 2.47%. That is the upper end of the recent range, but there is no momentum to speak of and the yield appears to be consolidating in a 2.40%-2.50% range. In the futures market, speculators are net short10-year Treasuries (for the third consecutive week) for the first time since last April.

Over the weekend, Abe urged the BOJ to continue its efforts to reflate the economy, but stopped short of endorsing BOJ’s Kuroda for a second term. Abe noted that job availability is near a 43-year high. Core inflation of 0.9% is the same as in the eurozone, though measured differently. Abe encouraged companies to boost wages by 3% of more, but there is no compelling reason to expect businesses to do so. |

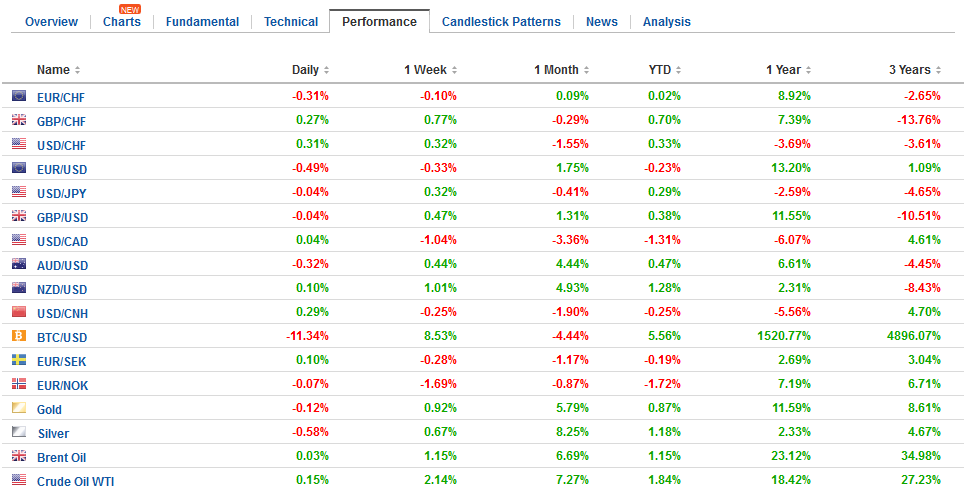

FX Performance, January 08 - Click to enlarge |

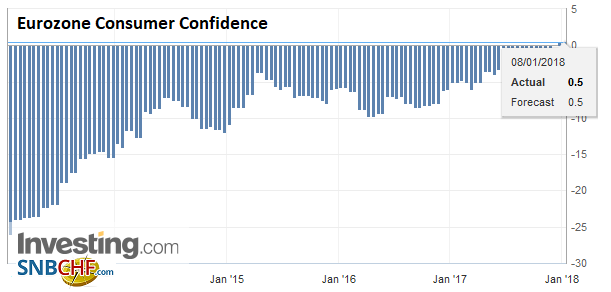

EurozoneThe eurozone reported stronger than expected survey and real sector data today. Sentix investor confidence rose more than expected (32.9 from 31.1), and other confidence surveys were firmer. |

Eurozone Consumer Confidence, Jan 2018(see more posts on Eurozone Consumer Confidence, ) Source: Investing.com - Click to enlarge |

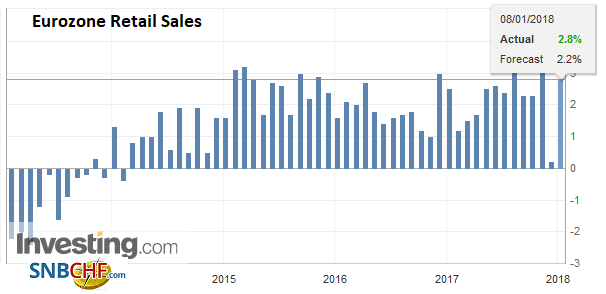

| November retail sales rose 1.5% after October’s 1.1% decline. The median forecast from the Bloomberg survey was for a 1.3% increase. |

Eurozone Retail Sales YoY, Nov 2017(see more posts on Eurozone Retail Sales, ) Source: Investing.com - Click to enlarge |

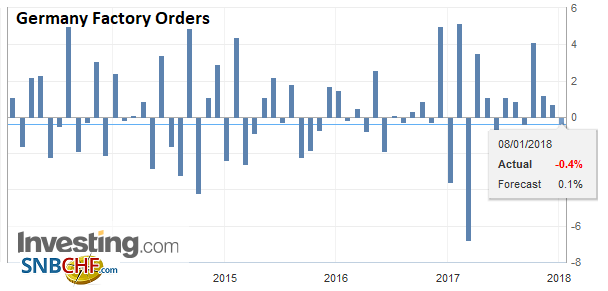

GermanyOn the other hand, Germany’s November factory orders disappointed by falling 0.4% after a revised 0.7% gain in October (initially 0.5%). The year-over-year rose an impressive 8.7%. The market had expected 7.8%. Domestic orders slipped 0.4%, while foreign orders fell 1.2%, though orders from EMU rose 0.7%. |

Germany Factory Orders, Nov 2017(see more posts on Germany Factory Orders, ) Source: Investing.com - Click to enlarge |

The UK’s Halifax reported disappointing December house prices. The 0.6% decline contrasts with expectations for a slight increase, and adding insult to injury the 0.5% gain in December was revised to 0.3%. The three-months, year-over-year rate eased to 2.7% (from 3.9%), to return to levels not seen since last August. The slowest pace in 2017 was seen in July at 2.1%.

There is much talk about a cabinet reshuffle in the UK, but nothing has been announced yet. While many senior posts are not expected to change, there are reports suggesting that a minister will be appointed for a “no-deal Brexit.” Sterling’s losses today appear more a function of the dollar’s bounce than specific UK concerns. Sterling has traded a couple of ticks on both sides of the pre-weekend range. Unlike the euro, it has not slipped through last week’s lows (~$1.3495).

The Australian dollar is the weakest of the majors, losing about 0.33% at about $0.7840. We note that large speculators in the futures market are carrying a net short Aussie position. A break of last week’s lows (~$0.7795) is needed to signal a proper correction. Separately, note that a government department warned that iron ore prices fall on average by 20% this year.

The corrective pressures in the foreign exchange market have not spilled over to equities. The MSCI Asia Pacific Index, excluding Japan, rose (~0.4%) for the fifth consecutive session Nearly all markets in the region rose. European bourses are mostly higher, as well. The Dow Jones Stoxx 600 is adding 0.2% to last week’s gains. It is the fourth consecutive advancing session. Today’s gains are led by real estate, financials and materials. Consumer staples and information technology are drags. US equities are flat to slightly higher. This week’s earnings include JP Morgan Chase, Well Fargo and Blackrock.

Bond markets in Asia may have been dragged higher by US Treasuries action after the jobs data. European benchmark 10-year yields are slightly softer. Peripheral bonds are doing best (off 1-3 bp), but Italian bonds are lagging.

The US reports consumer credit late in the session. It is expected to have risen around $18 bln in November. Consumer credit has slowed in the US, and without a stronger pick-up in November and December, it could be the weakest year since 2014. Three regional Fed presidents speak today. Bostic provides an economic overview, while Williams and Rosengren speak at a conference on inflation targeting. The market appears to be discounting around a 75% chance of a March hike.

The Bank of Canada releases the results of its senior loan officer survey. It is the last important economic data point ahead of next week’s rate decision. There are quantitative and qualitative aspects to the report. Another negative reading (-0.5 in Q3) would be disappointing. After the impressive jobs report at the end of last week, the odds of a rate hike next week increased to a little more than 80%. The odds were closer to 50% a week ago.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$EUR,$JPY,$TLT,EUR/CHF,Eurozone Consumer Confidence,Eurozone Retail Sales,Germany Factory Orders,newslettersent,USD/CHF