Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

There are a number of events and economic reports in the week ahead that will help shape the investment climate in the weeks and months ahead. In recognition of the importance of initial conditions, let’s briefly summarize the performance of the dollar and main asset markets.

After recovering from a five-month decline in September and October, the dollar has lost ground against all the major currencies here in November, save the Australian dollar. Benchmark 10-year bond yields are at the lower end of the ranges since over the last several months. The US two-year yield has risen, and the curve has flattened. In Europe, the 10-year yields have fallen more than 2-year yields, which has also resulted in curve flattening. US, Asia, and Emerging Market equities are near record or multi-year highs. European shares have underperformed in November after rallying in September and October.

United StatesTaxes: The Senate bill is currently expected to be brought to the floor on November 30. We expect it to come down to the wire but suspect the risk is that there are at least three Republican Senators of the 52 that will vote against the bill. It would not end the effort, any more than a similar defeat meant the Affordable Care Act is safe. Although the disappointment could spur a knee-jerk reaction, the medium-term implications may be constructive. If it does pass, we suspect it would provide fodder for the equity market and could spur a steepening of the yield curve. Powell Confirmation Hearings: The hearings will begin November 28. Investors think they have Powell’s measure. Mild-mannered, clear speaking, gradualist who has never registered an official dissent on the FOMC. With extensive turnover at the Federal Reserve, there will be many proposals for a “new beginning,” but look for Powell to represent a strong element of continuity. Changes in communication, and perhaps a press conference after every meeting, as the ECB and BOJ already do, would not be surprising. Little market reaction to his testimony means that Powell did a good job. Federal Reserve: There is at least seven Fed officials scheduled to speak in the coming days, including Yellen’s mid-week testimony before the Joint Economic Committee of Congress. The market remains confident of a rate hike next month. The January Fed funds contract implies a 1.39% effective average Fed funds rate. Recognizing that the first three days of the new year will be the year-end rate, which we assume to be 10 bp below the prevailing rate, generates an average effective rate for the month at 1.40%. By our reckoning, the market has one, and a half hikes discounted for next year. The Fed is signaling three, and at least one investment house says four. Will the next iteration of dot plots that comes at the conclusion of next month’s FOMC meeting show the same thing? The Beige Book will be released on Wednesday in preparation for that meeting. The report may show a strengthening of the expansion, with some areas reporting tightening of the labor market. Economic Data: Two reports stand out: The revision of Q3 GDP and the measure of inflation the Fed targets, the core PCE deflator. The initial estimate of Q3 GDP is expected to be revised to 3.2% from 3.0%, with stronger consumption a key factor, though perhaps goosed by quick rebuilding related demand after the horrific storms. The PCE core deflator reached 1.91% last October and fell to 1.290% in August. This is the mystery of which Yellen speaks, and one in which her working hypothesis is that is it due to short-term one-off factors. The core deflator is expected to rise to 1.4% in October. The bond market will be sensitive to any surprise, and through it, the dollar. |

Economic Events: United States, Week November 27 - Click to enlarge |

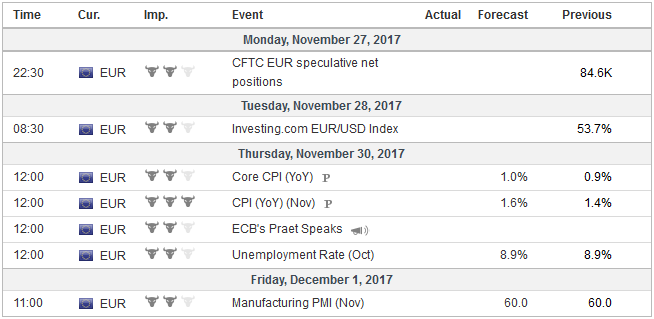

EurozoneEconomic Data: A synchronized upswing appears to be gathering steam. Laggards like France and Italy are fully participating. Spain also appears to be re-strengthening, like Germany. Despite political challenges in several countries, including Ireland, where the minority government faces a trying few days, the economic momentum continues unabated. The preliminary read of November CPI reported. The headline is expected to rise to 1.6% from 1.4%. Part of this reflects energy prices, but part is also due to core price. The core measure is expected to tick up to 1.0% from 0.9%. |

Economic Events: Eurozone, Week November 27 - Click to enlarge |

GermanyGerman Politics: The initial attempt to forge a coalition in Germany failed. The SPD, which has been the CDU/CSU coalition partner in two of the past three governments Merkel led, is reluctant to return to government. However, elections at this juncture could be disastrous as nothing has changed in the two months since it drew the least support in modern times. And to enter into government would make the AfD the largest opposition party. Investors seem to know two things. First, Merkel and the head of the SPD will meet Thursday to explore the possibilities of either a new Grand Coalition or a minority government. Second, the PMI and IFO survey data point to a reacceleration of the German economy here in Q4. |

Economic Events: Germany, Week November 27 - Click to enlarge |

United Kingdom

|

Economic Events: United Kingdom, Week November 27 - Click to enlarge |

JapanBOJ: Following the MOF’s decision to cut the initial target issuance of 40-year bonds, after having previously cut the amount 30-year bonds it planned to issues, the BOJ announced the reduction of the number of long bonds (25 year-plus) by JPY10 bln to JPY90 bln. The curve at the long-end steepened, as a result. Data: Japan’s economic expansion remains intact. October industrial production is expected to bounce back from September’s softer report. However, capex and exports remain key. Consumption remains poor, despite a strong labor market, where unemployment is expected to remain unchanged at 2.8%. Overall household consumption is expected to have contracted in the 12-months through October, the same as in September. This broad measure of Japanese consumption has not risen in a calendar year since 2013. At the end of the week, Japan report October CPI figures. The headline is expected to slow to 0.2% from 0.7% year-over-year. This is largely an issue of the base effect. The BOJ targeted measure, which excludes fresh food prices, may tick up to 0.8% from 0.7%. But this increase is a function of the gains in energy prices. Excluding fresh food and energy, CPI may have remained steady at 0.2%. |

Economic Events: Japan, Week November 27 - Click to enlarge |

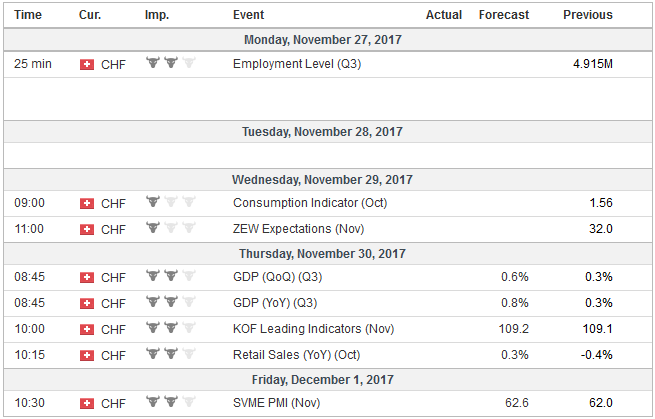

Switzerland |

Economic Events: Switzerland, Week November 27 - Click to enlarge |

Extend Output Cuts: Official comments have led investors to expect that OPEC and non-OPEC countries will agree to extend the output restraint through the end of next year. Currently, the output cuts have been agreed through March 2018. Compliance has been robust, according to various account.

Higher Prices and Inflation: A combination of the OPEC and non-OPEC restraint, some political issues, such as in Libya, and “normal” pipeline problems have helped lift prices. Brent may be up 8% this year, but it is up nearly 45% since the late June lows. The front-month futures contract has closed above a barrel for five consecutive weeks. Light sweet crude has risen 20% this year and is up 40% since the low near midyear. This can be expected to feed through into headline CPI measures.

Full story here Are you the author?

Tags: EMU,Federal Reserve,Japan,newslettersent,OPEC,U.K.,US