Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

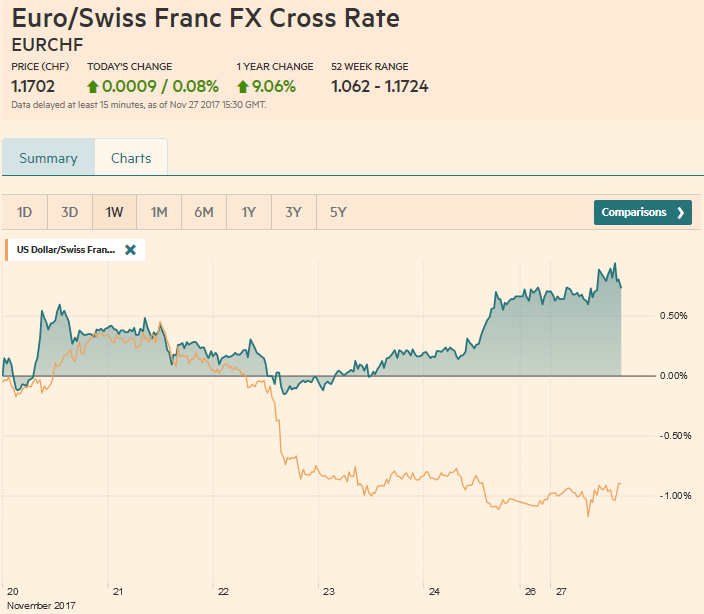

Swiss FrancThe Euro has risen by 0.08% to 1.1702 CHF. |

EUR/CHF and USD/CHF, November 27(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe US dollar is narrowly mixed and is largely consolidating last week’s losses as the market waits for this week’s numerous events that may impact the investment climate. These include the likelihood of the US Senate vote on tax reform, preliminary eurozone November CPI, a vote of confidence (or lack thereof) in the deputy PM in Ireland, Powell’s confirmation hearing as Yellen’s successor, the BOE financial stability report, and stress test, and the latest read on Japanese inflation. The euro extended last week’s gains (to nearly $1.1960) but is struggling to sustain the gains. It is slipping below the upper Bollinger Band (~$1.935) near midday in Europe. Last week’s low was set last Tuesday near $1.1715 when the US 2-year premium over Germany peaked just shy of 2.50%. It eased for a couple of days, bottoming near 2.42%. It is back to 2.45% now. The 10-year differential poked through 2.00% early last week, fell to about 1.95%, and is firmer today. The drama in German politics failed to weigh much on the euro, but many see the possibility of a new Grand Coalition as constructive for the single currency. The head of the SPD Schulz will meet with Merkel on Thursday. It is not clear the price Schulz will demand. The SPD has a party conference December 7-9. Schulz, who is supported by the left-wing of the party, was under pressure following the poor campaign and results in the September election. The FDP, which had imploded during the European crisis, has returned to parliament, but only time will tell whether it made a good strategic decision to abandon the coalition talks. |

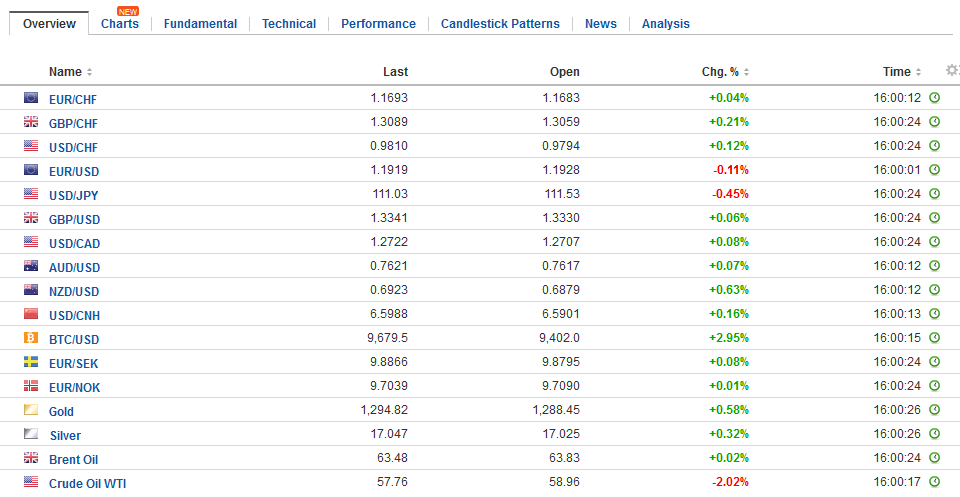

FX Daily Rates, November 27 - Click to enlarge |

| Meanwhile, it looks like a political crisis can be avoided in Ireland. The ongoing police scandal had threatened to topple the government. However, news reports suggest that Prime Minister Varadkar is close to a deal with the head of the opposition to avoid new elections. This comes as the UK was given until December 4 to make progress on the Irish border post-Brexit or risk continued divorce negotiations rather than moving to trade talks. There appears to be a strong consensus among most of Ireland’s political parties that a hard border between Northern Ireland and Ireland is not acceptable. Moreover, it also seems understood that Ireland’s negotiating position is strongest now and may weaken as the negotiations proceed.

The US dollar traded higher against the in early Asia. It tested the lower end of the band of resistance that was once supported (JPY111.65-JPY111.80) but has subsequently sold off to push through the pre-weekend low near JPY111.20. Last week’s low was set just above JPY111.05. A break of JPY111.00 would target the JPY110.15 area, a retracement objective of the rally from early September (~JPY107.30) to the high earlier this month (~JPY114.75). The dollar fell through the 200-day moving average last Wednesday and has not been able to resurface above it (~JPY111.70). We note that although the US 10-year yield is steady, Japan’s 10-year yield rose 1.4 bp. Sterling is trading firmly at the upper end of the pre-weekend range. It posted an outside up day before the weekend. A close above $1.3345 targets the $1.3430 area. Tomorrow’ the BOE issues its financial stability report and the results of this year’s stress tests on the top seven banks. There is also some talk that the BOE may raise the capital requirement. |

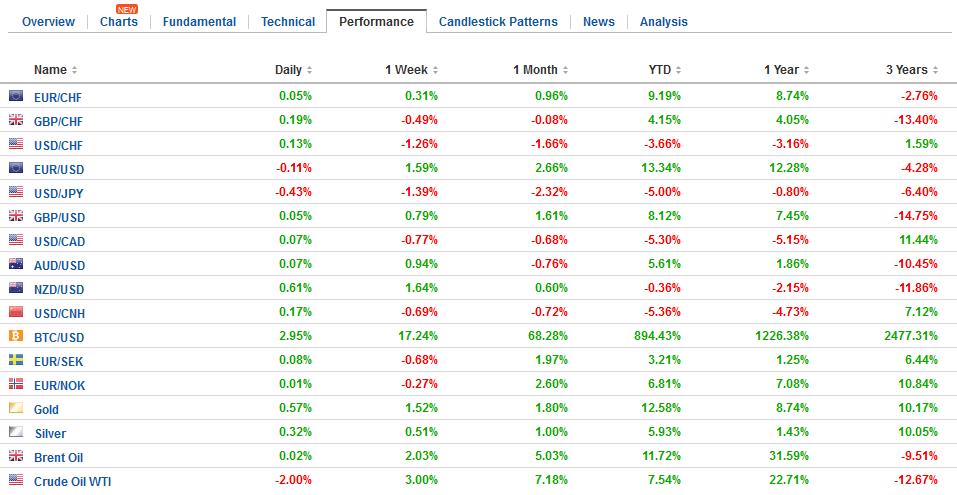

FX Performance, November 27 - Click to enlarge |

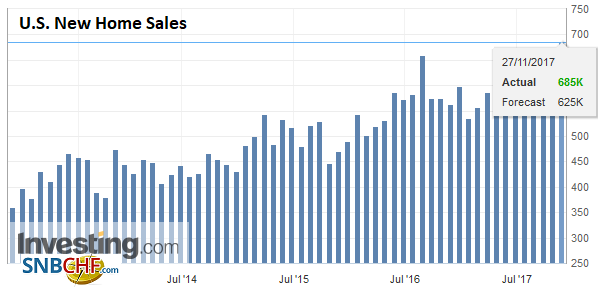

United StatesThe US session features October new home sales. After a nearly a 19% surge in September (storm related) a setback is widely expected. Several Fed officials speak this week. Today, the Minnesota Fed President Kashkari, a noted dove, who would likely dissent from a decision to hike rates next month speaks, as NY Fed’s Dudley, late in the session. Dudley has indicated he will step down in the middle of next year. Simon Potter, who heads up the NY Fed’s Markets group is seen as a likely successor. |

U.S. New Home Sales, Oct 2017(see more posts on U.S. New Home Sales, ) Source: Investing.com - Click to enlarge |

Asian shares traded lower, even though the US S&P 500 and NASDAQ set new record highs before the weekend. The MSCI Asia Pacific Index snapped a four-day advance and lost about 0.4%. Australia, India, and Malaysia bucked the regional trend. Chinese shares resumed their slide after posting small gains ahead of the weekend after last Thursday’s large fall. The CSI 300 (large cap) fell 1.3%, essentially halving this month’s gain. It follows a nearly 7% decline in the last three sessions last week. Shenzhen’s 1.5% drop brings its loss for the year to almost 4.0%. With stretched valuations, market sentiment has been vulnerable to signs that the government is still committed to deleveraging, while the official media targeted an individual company that was a stellar performer.

There is also a tightening of liquidity in China. China’s 12-month interest rate swaps climbed for the first time in three sessions. The yield on the 10-year government bond rose two basis points to near 4.0%. The year-end pressure was also seen in Hong Kong, where the one-month interbank rate rose to 0.92225%, the highest since 2008.

European shares and bond are mostly trading with a firmer bias. The Dow Jones Stoxx 600 is recouping its pre-weekend dip, led by utilities and real estate. Materials and information technology are nursing modest losses. Among the bourses, the DAX is the laggard today. Most core and peripheral yields are lower in Europe. Italy and Portugal’s 10-year yields are off three basis points, while Spain’s yield is down less than two. Core yields are off by around a single basis point.

In emerging markets, the key talking point today is the recovery of the South African rand after S&P’s downgrade to below investment grade status took 2% of the currency before the weekend. It is up 3% today and at its best level in a month. Meanwhile, in Mexico, Deputy Governor of the central bank, Diaz de Leon has been tipped to replace Carstens at the head of the central bank. And, Finance Minister Meade is expected to step down today and formally accept to lead the PRI into next year’s elections.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$EUR,$JPY,$TLT,EUR/CHF,MXN,newslettersent,U.S. New Home Sales,USD/CHF